The Edge Singapore’s REITs Investment Forum took place over two evenings, on Aug 19 and Aug 26, at the SGX auditorium to a full house. Both sessions saw lively debate and strong audience engagement. On Aug 19, the theme and title were Home Advantage: Singapore REITs anchored for stability, while the theme for Aug 26 was Beyond Borders: 2025 outlook for global REITs.

Adrian Chui, CEO of ESR-REIT’s manager, kicked off the first evening with a presentation on his REIT and a conversation on the benefits of a Singapore-focused portfolio, robust capital management, asset enhancement initiatives and interest rates. He pointed to a turnaround in distributions per unit (DPU) for ESR-REIT.

Interest rates are an important driving force for REITs’ cost of debt, the capital values of their portfolios and their unit price. “Interest rates are coming down, which we have been guiding the market on since last year. In June 2024, the peak for our interest cost was 4.06%. In December 2024, it was 3.8%. As of June 30, it is down to 3.4% primarily because we have been actively managing our interest rate exposures through the various stages as they expire, even though our fixed interest cost is at 80%,” says Chui.

Falling rates and active asset and property management underpinned ESR-REIT’s net property income (NPI), which rose by 30.1% y-o-y to $166.3 million in 1HFY2025. DPU rose by 0.2% y-o-y to 11.239 cents, reversing an 18% decline a year ago. Core DPU, which accounts for approximately 96% of total DPU, rose 8.1% y-o-y, reflecting the full-period contribution from the newly acquired assets, completed asset enhancement initiatives (AEIs), organic growth and partially offset by the additional funding drawn to support the acquisitions.

“Close to 84% of our rental income comes from Singapore. Our portfolio comprises new economy assets, primarily logistics and high-spec space, which are now more in demand,” Chui says.

Han Khim Siew, CEO of OUE REIT’s manager, the next speaker, also highlighted the impact of lower interest rates on OUE REIT’s finance costs. ”Finance cost has declined significantly. That has helped with our overall performance for the DPU,” he says.

See also: OUE REIT’s growth playbook — Singapore-centric assets with interest rate tailwinds

Following the sale of Lippo Plaza, Shanghai, which was completed in December 2024, OUE REIT boasts an all-Singapore portfolio, one of only three REITs. “50% of our income is from Singapore office. Rental reversion was 9.1% for [2Q2025]. If you include this quarter, we’ve had 12 consecutive quarters of positive rent reversion. For those 12 quarters, all three of our office buildings recorded an increase in rent,” Han says.

He cites the trend as being a beneficiary of OUE REIT’s prime assets in the heart of the CBD. “Most office employees like to be downtown. Hence, employers, including MNCs, prefer to be headquartered in the CBD.”

“Our rents will remain strong because our average expiring rent for this year is $10.86 psf, and for next year, it is $10.29 psf. The market rent for Grade A office buildings is $12.10 psf. Our rents are still trading below the market,” adds Han.

See also: ‘It’s time to start growing’ as Elite UK REIT acquires, repositions assets

ESG boosts rents

Attendees at The Edge Singapore’s REITs Investment Forum were canvassed on what they view as important when investing in REITs. DPU scored the highest, and ESG (environment, social, governance) the lowest. Increasingly, investors view sustainability as a cost with limited benefits.

Guy Cawthra, CEO of Lendlease Global Commercial REIT’s (LREIT) manager, says that its buildings in Singapore are graded as Green Mark Platinum by the Building and Construction Authority.

“Why do we care about sustainability, and why do we care about the environment? And the short answer is, because it’s the right thing to do,” adds Cawthra. According to him, Lendlease was founded by a Dutch Australian, Dick Dusseldorf, who believed that companies owe a responsibility to society.

“When we look at developing our projects, we always look to push the envelope and create the most sustainable real estate that we can. We do that to future-proof the property; secondly, it’s what our tenants and our customers also want. If you look at tenants across the globe, particularly in office space, many tenants won’t occupy a building which is not green,” Cawthra says.

Many MNCs have their own sustainability targets. Cawthra adds that environmentally friendly, sustainable buildings are also more efficient. “I think we would all agree that reducing our water consumption, reducing our electricity consumption, reduces our costs, and that’s got to be a big financial decision as well.”

Han of OUE REIT’s manager has an additional reason to have his buildings green marked. He says: “We need to access the green financing. Accessibility to financing means we can get cheaper financing. Secondly, if we’re not green marked, then you are dealing with a small pool of tenants, which means your rents are coming down as well. And lastly, on a more practical basis, is really, if we don’t ensure that our buildings are green marked, if the chillers aren’t changed and the lighting isn’t updated, what happens when it’s time to sell?”

To stay ahead of Singapore and the region’s corporate and economic trends, click here for Latest Section

The reality is, when it is time to sell, the buyer may offer a lower price for a non-Green Mark platinum building. Hence, the practical and financial reasons for focusing on sustainability include access to cheaper financing, green financing, higher rents, higher occupancy, and eventually, to sell at the full market value.

For Chui of ESR-REIT’s manager, Green Mark buildings are attractive to MNCs because they have a green procurement and sustainability requirement. “Generally, when we sell assets, we tend to sell to institutional investors, and increasingly, institutional investors will look at whether you have ESG features or not. If not, they will just deduct the money. Our approach, from the leasing point of view, is that the bulk of our tenants who want us to focus on making ESG more important in their leasing decisions is not as weighted heavily as compared to office,” he adds.

According to CBRE, grade A office rents average around $11-$12 psf. Industrial property rents are in the low to mid-single digits. The amount spent on ESG has to be commensurate with the rewards. Two factors that are likely to affect ESG spend are the impact on distributions and the longer-term value of the asset, market watchers say.

Interest rates are important

In her presentation on Aug 26, Nupur Joshi, CEO, REITAS, focused on the importance of the interest rate cycle and interest rates on REITs. Interest cost is the largest expense of the S-REITs. According to Joshi, the average aggregate leverage for the S-REITs is around 39% with the average interest coverage ratio at around 3.2 times. While aggregate leverage is below the regulatory ceiling of 50%, and ICR is above the regulatory floor of 1.5 times, these ratios are less robust than those for US REITs. According to NAREIT’s REITs industry factsheet, the average aggregate leverage of US REITs was 32.5% in 1Q2025, and the average ICR was 4.2 times.

Interest rates are important for REITs for three main reasons. They impact distributions as interest expense is the most important expense item for S-REITs. Capitalisation rates and discount rates are affected by interest rates, and these, in turn, affect capital values. Outlook for rents and cash flow also impact capital values, and lower policy rates are likely to boost both rents and cash flows. Third, to maintain the yield spread between risk-free rates, distribution per unit yields are likely to compress. With DPU as relatively stable as the numerator within the ratio, unit prices are likely to rise.

“As interest rates decline, REITs become more attractive for those investors who are looking for yield. You’re getting a much lower rate on your six-month T-bills than previously,” Joshi points out. REITs, which are yielding an average of 6% look a lot more attractive than six-month T-bills, which are yielding 1.44% based on the latest auction on Aug 28.

Because of the influx of liquidity into Singapore as a result of the Singapore dollar’s haven status, Sora is at the lowest rate in more than three years. “There are more capital inflows because of a reallocation of capital flows from investors,” Joshi says.

Lower rates are likely to lower REITs’ cost of debt, which have already started to decline despite most REITs hedging around 70% to 75% of their debt on fixed rates.

“Gradually, over time, as those hedges fall off and they have to refinance, REITs will have the benefit of refinancing at lower rates. For the June-end results announcements by the Singapore-focused REITs, there was a noticeable decline in their interest cost,” Joshi indicates. She believes this is just the beginning of the decline in interest expense.

At a recent meeting of central bankers at Jackson Hole, Federal Reserve Chairman Jerome Powell indicated that more rate declines are possible. Up to the start of this year, US and Singapore rates moved in tandem, with the pass-through from US rates at around 70% to 80%. However, since the start of this year, US and local rates have diverged, with Sora and local risk-free rates falling. Singapore’s risk-free rates are at around 1.84% compared to the 10-year US Treasury yield of 4.23%.

Declining US rates will probably provide a floor to the declining valuations of the assets of US-focused S-REITs, and S-REITs with US assets such as Mapletree Industrial Trust, CapitaLand Ascendas REIT, and CapitaLand Ascott Trust.

With the cost of debt falling, property valuations are likely to stabilise. “Concern over property valuations may recede. There could be potential upside which could lift the net asset values. In a DBS report, the analysts are expecting 10% total return,” Joshi says. Total return includes DPU and price appreciation.

Retail and the JS-SEZ

By December next year, the Johor-Singapore Rapid Transit System Link (RTS) will be up and running. Whether Johor takes business away from Singapore remains to be seen. Chui says that Medina, which was part of Iskandar, already exists.

“It’s not as if competition is not there. The key important question is, who and what is going to be filling up the space, and how will Singapore’s economic fabric change over time?” adds Chui. In his view, Singapore’s focus is likely to be different from the Johor-Singapore Special Economic Zone (JS-SEZ) that the new linkages, such as the RTS, are meant to help. At any rate, Chui believes that the JS-SEZ will take many years. “My immediate concern is around the trade dynamics with the tariffs. This is the focus for us in the next 12 to 24 months,” he adds.

Cawthra offers a more ground-level perspective. He recounts a weekend trip to Johor: “It took me an hour to get there, and an hour and a half to get back. I was worried that my taxi that took me there may or may not have been legal,” he jokes. Aside from transport woes, he thinks the RTS is a fantastic idea. “It’s going to ease the transport [bottlenecks] between the two countries, and hopefully bring greater collaboration. The two governments have big aspirations for the SEZ if we can get better synergies between the two countries.”

As for retail, Cawthra says it remains an unknown. Johor is usually a destination where Singaporeans go for food and services such as beauty care and medical. “If you look at the price of regular items in our stores, it might be similar. So visitors from Singapore are probably not going for that purpose. We don’t know the impact yet, but I’m confident of our offering in the malls we have. It’s indirect competition, and it forces all of us to raise our game,” adds Cawthra. LREIT owns 313@somerset and Jem. As such, Cawthra doesn’t think that Johor provides direct competition.

Han of OUE REIT says Mandarin Gallery, which is the retail portion of Hilton Singapore Orchard, has a completely different retail proposition from suburban malls in Singapore. “We can offer retailers from overseas who come in and want to open one, maybe two stores in Singapore, a great location with a curated offering,” Han says.

Mandarin Gallery isn’t a mass market mall with chain stores. The retail stores are almost bespoke. Han points to the Rimowa store in Mandarin Gallery as one of two in Singapore, the other one being at Marina Bay Sands. The Korean theme is popular, and the Mandarin Gallery has Korean restaurants. Mandarin Gallery also hosted K-pop girl group Blackpink’s Rose streetwear pop-up store during August.

Should REITs still head overseas?

Among Singapore’s selling points that Joshi highlights is that it is a global REIT listing venue. “We have 17 REITs out of our 38 traded REITs that have all their properties, or substantially all their properties outside of Singapore, or their sponsors are from outside of Singapore. This is what makes the Singapore REIT market unique. You can invest in SGX and get access to the properties in all these different markets,” Joshi says.

However, investing in REITs with overseas assets comes with risks. This was amply articulated in the circular of Frasers Hospitality Trust (FHT). Among the reasons for the privatisation was the depreciation of currencies in FHT’s foreign markets against the Singapore dollar. Other REITs with overseas assets have been similarly impacted, including CDL Hospitality Trusts. As an example, CapitaLand Integrated Commercial Trust’s Australian properties declined by 15.2% as at December 31, 2024, partly because of the depreciation of the Australian dollar against the Singapore dollar. But CICT’s Singapore properties outperformed, causing valuation and net asset value to rise in FY2024.

REITs with US assets have performed particularly poorly because of the interest rate cycle, the slow return-to-office of US workers, and the lack of liquidity in the system. Singapore retail investors would have been impacted by the depreciation of the US dollar against the Singapore dollar this year. In general, local investors have not had a good experience investing in REITs with mainly overseas assets. In addition, local investors experienced governance and financial issues with the sponsors of a Chinese S-REIT and property trust.

On Aug 26, Professor Joseph Ooi, co-director, NUS, IREUS, in his presentation, acknowledged that REIT managers have a more challenging time understanding foreign markets. It isn’t just currency risk. Governance, understanding the legal and regulatory framework, the property cycle and demand and supply of the overseas market are some of the factors that affect execution. Costs are likely to be higher through additional fees paid to property, legal and financial consultants for overseas acquisitions and management.

“When does geographical diversification fail? When you go blindly for the sake of expansion and growth, and everybody is doing it. That results in a lack of local expertise, poor risk management, overpayment and cash overruns. My key takeaway is, one, overseas expansion can boost growth, but it comes with a risk. Ultimately, it is management quality, asset selection, discipline and execution,” says Ooi.

One of the top performing REITs this year based on total return this year is Elite UK REIT, which owns only UK commercial assets, and its unit price is traded in UK pounds. On Aug 26, Joshua Liaw, CEO of Elite REIT’s manager, says he focused on two areas, asset performance and rental reversions.

In 1H2025, Elite UK REIT’s revenue increased 0.5% y-o-y to GBP18.7 million ($32.4 million), arising from positive rental reversion and new rental income from the acquisition of three government-leased properties in June. With interest savings arising from capital management and interest rate optimisation, tax planning and tax benefits from sustainability-related capital expenditure, distributable income increased 5.8% y-o-y to GBP9.7 million, while DPU rose 10% y-o-y to GBP0.0154 in 1H2025.

“The assets we bought are accretive with a long WALE of 7.4 years. They are very important from a risk perspective, mission-critical, government, and national infrastructure. We’ve done some refinancing last year, and we had our lowest gearing ever of 40.7%. Along the way, we’ve also gotten a bit clever with our debt structure,” Liaw says.

He says that the REIT takes three-month advanced rentals from the UK government. Instead of putting the money in fixed deposits, the REIT used it to reduce debt whenever possible. In addition, valuations fell in prior years, and the portfolio has been de-risked. Year-to-date, Elite UK REIT’s unit price is up 20.7%, excluding DPU.

What’s next?

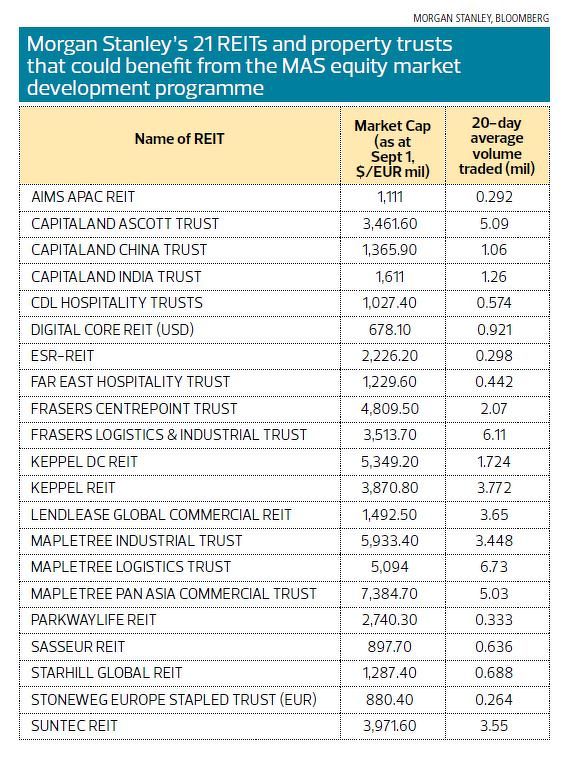

On the evening of Aug 26, in his keynote speech, Ronald Tan, senior vice-president, global sales and origination, SGX, highlights that the local REIT sector has been instrumental in capturing new asset classes such as New Economy (logistics and life science), the living sector and data centres. He points out that Morgan Stanley’s Singapore at 60 report forecasts that Singapore will be Apac’s largest REIT market by 2035, overtaking Japan and Australia. This could be boosted by data centre listings, follow-ons and secondary equity fund raisings.

“I also want to give prominence to the MAS Task Force announcements of various measures, including the Equity Development Fund, which is directed at the small and mid-cap stocks. In the [Morgan Stanley] report, they’ve identified 24 REITs and trusts that could be beneficiaries and see uplifts in liquidity and valuation.”

Which are these 24 REITs and business trusts? According to Singapore at 60, the 24 REITs and business trusts have an average market cap of US$2.1 billion ($2.6 billion), and a daily value traded of US$4.6 million. They offer high and stable dividends (dividend yield: 7%). The report says: “their propensity to raise equity through secondary market placements positions them well to grow market cap over time, potentially scaling up enough to be upgraded to the MSCI Singapore Index, per our assessment. This happened with Suntec REIT in 2014 and Mapletree Logistics Trust in 2020.”

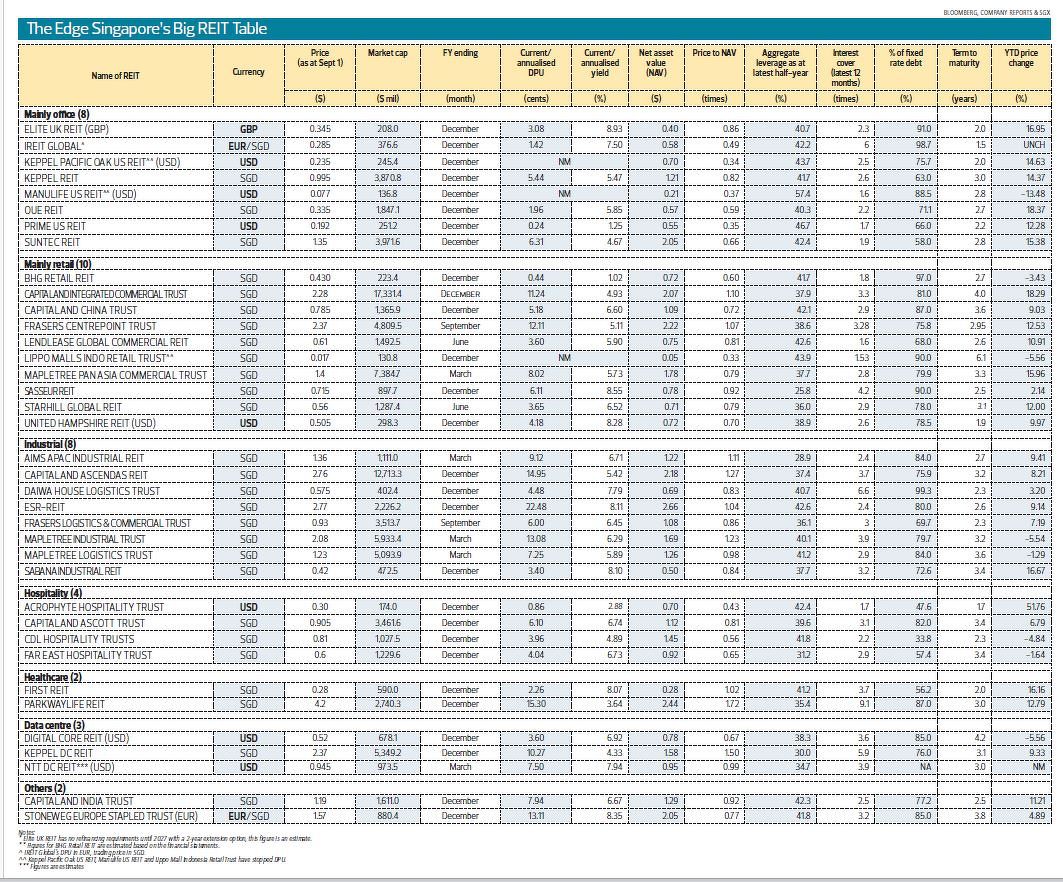

The 24 REITs and business trust list comprises four business trusts, including CapitaLand India Trust and 20 REITs, including overseas REITs such as CapitaLand China Trust. The TES Big REIT table can be viewed here and Morgan Stanley's 21 REITs and property trusts are here.

{kind=link}

{kind=link}