That was the story of the digital age — hence our series of articles on the future of media in this digital age.

The next disruption will be more profound.

From platforms to intelligence

Artificial intelligence (AI) will not just reshape media — it will redefine its interface.

See also: A recurring pattern in the history of information

Social media disrupted distribution. AI will disrupt the need to visit publishers at all.

Historically:

Pre-internet: Reader → Newspaper → Content → Ads

Social media era: Reader → Platform → Publisher

AI era: Reader → AI Assistant → Answer

The destination disappears.

AI assistants will aggregate, interpret and deliver information directly — bypassing both publishers and platforms. The shift is not incremental. It is structural.

This is not just another distribution layer. It is the intelligence layer — and whoever owns it owns the user relationship (the customers who pay).

The ‘Spotify Moment’ for journalism

Even the strongest players are not immune. The success of institutions such as The New York Times, Financial Times and The Economist was built on a simple but powerful model: Own the audience, build trust and monetise through subscriptions and advertisements.

For more stories about where money flows, click here for Capital Section

They survived social media by pulling readers back into a direct relationship.

AI threatens to break that relationship. If Spotify intermediated artists and listeners, AI will intermediate journalists with readers. The interface captures the user. The producer becomes invisible.

Journalism risks becoming infrastructure, not destination. We have seen this before: Amazon captured retail, booking platforms captured hotels and Uber captured taxis.

And AI assistants will capture information.

What can media companies do?

There are only a few strategic paths — and none is without risk.

1 Become a data supplier to AI: License content into the AI ecosystem. A new revenue stream, but at the cost of commoditisation. You become a cog in someone else’s machine.

2 Build your own AI layer: Integrate AI into your product — summaries, personalisation, research tools. Done well, AI enhances subscription value. Done poorly, it accelerates disintermediation.

3 Double down on original journalism: AI summarises. It does not investigate. It does not uncover. It does not take risks. Original reporting remains the last defensible moat.

4 Turn brand into identity: In a world of infinite information, people will not just pay for facts — they will pay for judgement. Trust becomes a signal. Editorial voice becomes an asset.

But all four strategies face the same unanswered question: Can any media company truly own the audience when the interface itself is intelligent?

When readers consume your content without ever visiting you, do you still exist?

A winner-takes-most world

For most media companies, the outlook is harsher.

AI collapses differentiation. Readers want the best answer — not 10 versions of the same story. This creates winner-takes-most dynamics, where only a few brands survive at scale. The rest becomes invisible.

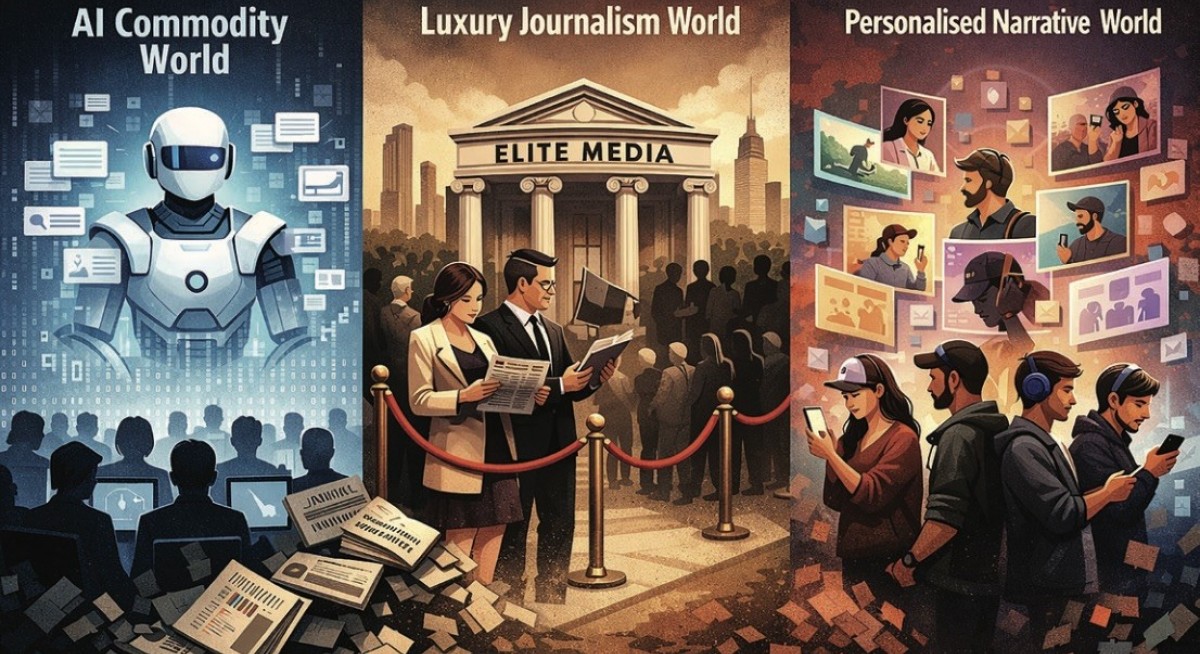

Three possible futures

1 The AI Commodity World: Information becomes abundant, instant and free. AI summarises everything — news, analysis and context. Distribution is controlled by AI assistants and platforms.

For users: frictionless, interchangeable and commoditised. For publishers: economic collapse.

Journalism becomes invisible infrastructure

The deeper risk: If original reporting is no longer funded, AI will eventually summarise less truth, not more.

[If you produce information, AI replaces you]

2 The Luxury Journalism World: A small group of elite institutions survives.

They are not content producers — they are trust providers.

Readers pay for verification, judgement, access and credibility. Journalism becomes a premium product.

But this creates a divide: a well-informed paying minority — and a mass audience reliant on free AI summaries.

[If you produce trust, AI amplifies you]

3 The Personalised Narrative World: Media fragments. AI enables personalised feeds, niche communities and individual creators to scale. People follow voices, not institutions.

The result: Thousands of micro-brands. Highly engaged but narrow audiences. Competing realities.

The risk is not misinformation — but parallel truths.

[If you produce narrative, AI fragments you]

Why this matters

This is not just an industry problem.

The erosion of independent media has consequences for democracy, accountability and the quality of public discourse.

If truth becomes unprofitable, it becomes scarce. And when truth becomes scarce, power fills the vacuum.

What comes next?

Media still has one remaining advantage. One last moat. Next week, we explore what it is — and whether it is enough.

Portfolio commentary

The Malaysian Portfolio fell 0.7% for the week ended July 1, faring better than the benchmark FBM KLCI, which dropped 1.5%. The only winner for the week was Kim Loong Resources (+0.4%), while the biggest losers were Public Bank (-2.5%), United Plantations (-1.9%) and Maybank (-1.5%). Total portfolio returns now stand at 220.8% since inception. This portfolio is outperforming the benchmark FBM KLCI, which is down 9.4% over the same period, by a long, long way.

The Absolute Returns Portfolio, meanwhile, was down 1.0% for the week. The loss pared total portfolio returns to 24.8% since inception. The top gainers were Microsoft Corp (+5.1%), Alphabet Inc - CL C (+3.7%) and Berkshire Hathaway (+1.0%), while the notable losers were Talen Energy Corp (-11.1%), Alibaba Group Holding (-6.6%) and Sun Hung Kai Properties (-1.3%).

The AI Portfolio continued to see volatility, which is not unexpected. It gained 4.4% last week, lifting total portfolio returns to 29.5% since inception. The top gainers were Naura Technology (+21.8%), Unusual Machines (+19.0%) and Datadog (+18.8%). Hewlett Packard Enterprise (-9.8%), Alibaba (-6.6%) and Roundhill Memory ETF (-5.8%) were the biggest losers for the week.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks, including the particular stocks mentioned herein. It does not take into account an individual investor’s particular financial situation, investment objectives, investment horizon, risk profile and/or risk preference. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.