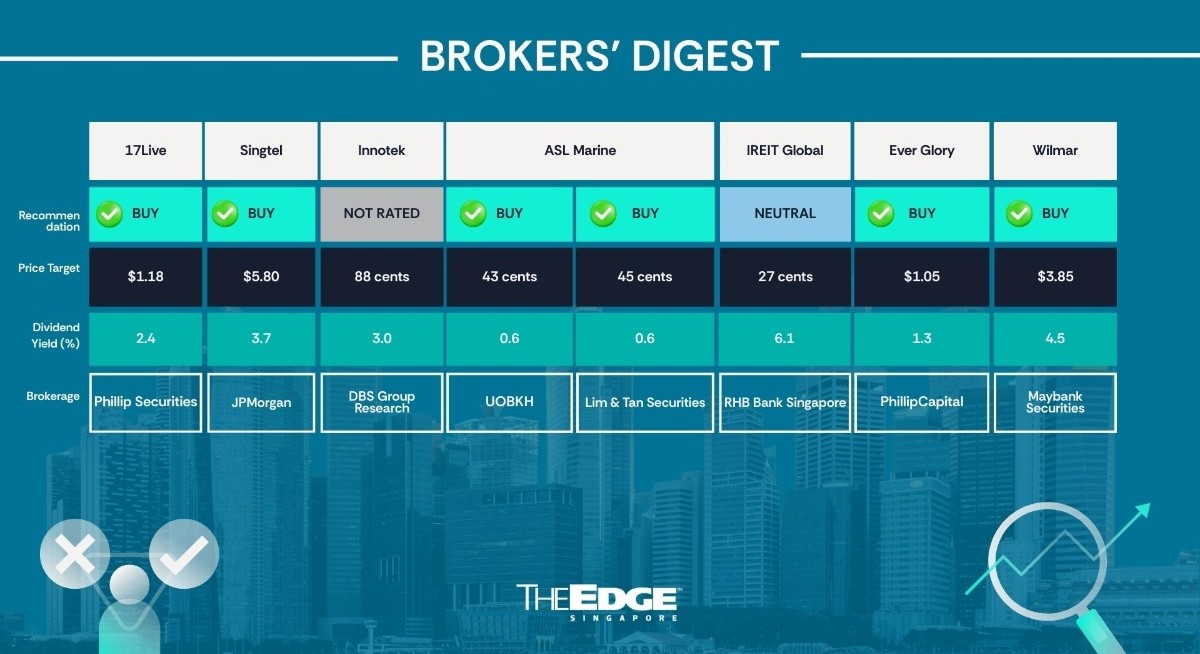

PhillipCapital is reiterating its “buy” call on Singapore’s first and only successfully Spac-listed company, 17Live (SGX:LVR![]() ) , but has dropped the target price to $1.18 from $1.45 previously.

) , but has dropped the target price to $1.18 from $1.45 previously.

This comes on the back of the live-streaming platform operator’s recent FY2025 ended Dec 31, 2025 results announcement, which showed the group turned profitable for the 2HFY2025 period. It reported earnings of US$3.68 million ($4.68 million) compared to a loss of US$5.21 million a year ago. On a full-year basis, the group is still in the red, but losses narrowed to US$924,000 from US$3.27 million in FY2024.

The group posted operating revenue of US$158.8 million in FY2025, a 16.8% y-o-y decrease, primarily due to Liver livestreaming. The group’s revenue from V-Liver live streaming increased slightly from US$11.0 million in FY2024 to US$11.1 million in FY2025.

Revenue for 2HFY2025 came in at US$77.6 million, a decline from US$89.7 million a year ago.

See also: Info-Tech to benefit from 'structural shift' in government's AI-related push: RHB

17Live declared a final dividend of 0.5 cent per share. Including its interim dividend of 1.5 cents per share, the total dividend payout for FY2025 is 2.0 cents.

Looking ahead, besides beefing up its streamer ecosystem, the company plans to diversify its revenue base. This includes moving into short-form drama in Japan and the continued development of live commerce in other Asian markets.

“Leveraging its creator base, technology infrastructure, and strong balance sheet, the group remains confident in its ability to deliver sustainable revenue growth and profitability improvement,” says 17Live.

See also: Mittal of DBS maintains 'buy' on Singtel on sale of Gulf Development stake

Analysts Serena Lim and Paul Chew note that while the group had turned a profit in 2HFY2025, earnings were below expectations.

“We reduced our FY2026 revenue and patmi forecasts by 25% and 37.5%, respectively, reflecting softer growth assumptions for the livestreaming market, slower monetisation trends, and a longer ramp-up period for new initiatives to contribute meaningfully to earnings. We continue to expect a consistent dividend policy and management’s ongoing share buyback programme,” say Lim and Chew.

In addition, 17Live continues to execute the share buyback programme launched in 2024, with authority to repurchase up to 10% of issued share capital. As of 2HFY2025, 9 million shares, valued at US$6.8 million, have been bought back, representing about 53% of the authorised limit under the current mandate.

However, Lim and Chew are cautious about the negative growth from core segments at the moment. “We expect the negative growth in the core segment (2HFY2024: –34%) to gradually narrow as the removal of exclusive contracts and ongoing events attract top-active streamers from competitors. This should boost monthly active users, particularly in Japan, and support higher conversion to paying clients, with revenue impact likely to materialise in FY2026,” they say. — Samantha Chiew

Singapore Telecommunications

Price target:

JPMorgan ‘overweight’ $5.80

Early commencement of share buybacks

JPMorgan is maintaining its “overweight” rating on Singapore Telecommunications (Singtel) (SGX:Z74![]() ) and raising its target price to $5.80 from $5.20 previously.

) and raising its target price to $5.80 from $5.20 previously.

For more stories about where money flows, click here for Capital Section

The move comes as Singtel has executed its share buyback programme earlier than expected, as part of its broader capital recycling strategy to boost shareholder returns, according to analysts Ranjan Sharma, Sigrid Qiu and Ankur Rudra.

Singtel has set a goal of monetising $9 billion in assets, with the proceeds earmarked for $5 billion in dividends, a $2 billion share buyback and $2 billion in growth initiatives. It has already begun the buyback, repurchasing roughly $50 million worth of shares since Feb 27, ahead of JPMorgan’s earlier-than-anticipated estimate.

The analysts see room for the monetisation target to increase as the value of several portfolio companies has risen. “If the asset monetisation target is increased, Singtel could increase its planned dividends and buybacks and/or support shareholder distributions over a longer period, in our view,” they write in a March 6 note.

Even after a 122% total shareholder return since January 2024, JPMorgan believes Singtel’s underlying non-listed assets “remain deeply discounted” at a forward EV/Ebitda of three times. Buybacks and asset recycling could help narrow that discount.

Growth in the infrastructure businesses is also expected to support earnings. The launch of 58 megawatts of additional data centre capacity in Singapore last month should drive stronger contributions from the segment.

In Australia, Optus added about 27,000 wireless customers q-o-q, while average revenue per user (ARPU) remained stable in 3QFY2026 despite the disruption caused by the Triple Zero outage. The analysts believe Optus can gradually improve ARPUs if its customer base remains resilient, and the stronger Australian dollar — up about 6% since September 2025 — could provide a FX tailwind to earnings.

JPMorgan analysts increased the target price to $5.80, mainly due to the roll forward to March 2027 and a higher P/E multiple of 20 times, up from 19 times previously. “We apply a higher target multiple due to the capital recycling programme and earnings growth potential of the non-listed assets supporting the stock’s rerating,” write the analysts.

However, they “moderately lowered” their earnings per share (EPS) forecasts for FY2027 and FY2028 by 1% to 3%, reflecting lower earnings forecasts for Bharti Airtel, in which Singtel has a stake. Their projections also do not yet incorporate Singtel’s recent acquisition of STT GDC. — Nurdianah Md Nur

InnoTek

Price target:

DBS Group Research ‘unrated’

Scaling into the AI hardware value chain

DBS Group Research analysts Amanda Tan and Ling Lee Keng believe that Innotek’s (SGX:M14![]() ) exposure to AI will help support a structural re-rating of the counter beyond traditional precision engineering.

) exposure to AI will help support a structural re-rating of the counter beyond traditional precision engineering.

In their Mar 9 un-rated report, the DBS analysts observe that Innotek’s revenue remains predominantly exposed to the automotive (39% of FY2025 revenue) and office automation (22% of FY2025 revenue) segments. However, they see the strategic pivot toward server components (21% of FY2025 revenue) as a meaningful shift in earnings quality.

“The recent endorsement by Nvidia and IEIT Systems validates InnoTek’s technical capability in high-precision machining and metal fabrication, raises InnoTek’s profile amongst industry players, and embeds it within the fast-growing AI infrastructure value chain,” state Tan and Ling.

They note that InnoTek has been delivering prototypes to Nvidia to support future server models alongside active discussions with other customers for similar server-related projects, pointing to a pipeline of growth.

As server demand scales alongside artificial intelligence and cloud deployments, they expect the server segment, which already contributes 21% of sales, to grow 35% y-o-y in FY2026 and FY2027, outpacing legacy verticals and driving overall group growth.

However, the DBS team sees near-term volatility persist across automotive, office automation, and TV/display due to uneven end-demand, soft consumer spending and tariff uncertainty.

“Automotive markets continue their adjustment to weaker petrol vehicle demand in China, mitigated by growing EV demand. In the office automation segment, China remains weak, albeit more than offset by growth in Asia due to China+1. In contrast, the AI segment remains buoyed by secular tailwinds and strong hyperscalers’ capex spending, in addition to a ramp from new server customers,” the DBS team explains.

As Innotek expands from graphics processing unit (GPU) server chassis components to liquid-cooling systems, orders are expected to scale up starting in FY2026. “We have currently baked in server mix to grow from 21% in FY2025 to 30% in FY2027, in line with management’s expectations that in the next three years or so, the server segment will be similar to the automotive segment in terms of revenue mix,” they add.

Based on their estimates, given that Innotek supplies machine components to certain server customers, which typically carry margins of 20%–30%, they view the server segment as margin accretive relative to the group’s historically normalised gross margin of around 15%.

Meanwhile, to mitigate geopolitical risk and capture China+1 relocation demand, Innotek has established a new Malaysian plant, with operations targeted for 2QFY2026, and is more than quadrupling the build-in area in Thailand, reducing concentration risk to China while strengthening its ability to support multinational customers relocating production.

“In our view, its high-precision manufacturing capabilities, combined with an established Asean footprint, position the group to benefit from ongoing supply chain diversification structurally,” the DBS team predicts. As such, both Tan and Ling have assigned a fair value to InnoTek of 88 cents, based on 21 times FY2027 earnings. — The Edge Singapore

ASL Marine

Price targets:

Lim & Tan ‘buy’ 45 cents

UOB Kay Hian ‘buy’ 43 cents

Analysts from Lim & Tan and UOB Kay Hian (UOBKH) are more upbeat about ASL Marine (SGX:A04![]() ) after the shipyard’s 1HFY2026 earnings jumped eightfold to $17.1 million, exceeding bullish expectations. For the half year ended Dec 31, 2025, revenue was up 5.5% y-o-y to $181.6 million. Notably, the decrease in finance costs was nearly 73% to $4.0 million.

) after the shipyard’s 1HFY2026 earnings jumped eightfold to $17.1 million, exceeding bullish expectations. For the half year ended Dec 31, 2025, revenue was up 5.5% y-o-y to $181.6 million. Notably, the decrease in finance costs was nearly 73% to $4.0 million.

In his March 3 report, Nicholas Yon from Lim & Tan highlighted that the company, which is also in the ship chartering business, delivered an “earnings beat” for 1HFY2026.

“Overall, the results reflect both operating leverage and the early benefits of balance-sheet normalisation, supporting the sustainability of earnings momentum,” says Yon, who has kept his “buy” call and raised his target price from 33 cents to 45 cents. Similarly, Heidi Mo of UOBKH has raised her target price to 43 cents from 35 cents.

With a global ageing fleet driving demand for maintenance and repairs, this business is set to enjoy “structurally higher” margins than chartering or shipbuilding. Yon expects the repairs segment to remain ASL’s core earnings “engine” while Mo sees it as an earnings “anchor”.

Meanwhile, ASL’s chartering business is set to enjoy higher margins as older, less profitable ones are refreshed. Mo notes the 30% q-o-q increase in the chartering order book and 40% q-o-q decline in shipbuilding orders, signalling a continued pivot towards infrastructure-linked chartering. She alludes to ASL benefiting from Singapore’s coastal protection projects, which could cost up to $100 billion.

Yon says ASL’s interim dividend of 0.13 cents is a signal of its confidence to sustain earnings. Yon cheers the faster-than-expected reduction in the debt level, to the point that he expects a net cash position by the end of FY2027.

Based on ASL’s business outlook and strengthening balance sheet, Mo raises the forecast for earnings by 4% to 9% for FY2026 to FY2028 and values the stock at 43 cents, or 12 times FY2027 forecast earnings, representing a slight discount to peers.

Yon has raised ASL’s FY2026 and FY2027 profit forecasts to $33.1 million and $38.3 million, respectively. He values the company’s shares at 45 cents, with a P/E of 12 times estimated FY2027 earnings per share, a slight discount to peers. — Lin Daoyi

IREIT Global

Price target:

RHB Bank Singapore ‘neutral’ 27 cents

Missed projections on higher costs

Vijay Natarajan of RHB Bank Singapore has downgraded his call on IREIT Global (SGX:UD1U![]() ) to “neutral” from “buy” after the Europe-based REIT’s distributions per unit (DPU) in 2HFY2025 ended Dec 31, 2025 missed his expectations. From his previous target price of 35 cents, Natarajan now figures this counter is only worth 27 cents.

) to “neutral” from “buy” after the Europe-based REIT’s distributions per unit (DPU) in 2HFY2025 ended Dec 31, 2025 missed his expectations. From his previous target price of 35 cents, Natarajan now figures this counter is only worth 27 cents.

The REIT, citing higher financing costs and lower net property income margins, has reported a 2HFY2025 DPU of EUR0.0038, a 59.6% y-o-y plunge, bringing full-year DPU to EUR0.0109, down 42.6%.

Also, the REIT’s net asset value (NAV) has been lowered “unexpectedly” too by 13% in euro terms. A new valuer, citing significantly higher discount rates, lowered the valuation of the REIT’s key assets, the Berlin campus by 18% y-o-y, and the Concor Park by 38% y-o-y.

In 4QFY2025, IREIT’s portfolio occupancy rate rose 0.4 percentage points q-o-q to 89.4% and is likely to inch up higher, with a few active leasing discussions underway. The REIT also achieved a 4% portfolio rent escalation in FY2025.

He notes that the REIT remains in talks with two potential “high quality” AAA-rated office tenants to secure sizeable leasing commitments and that the leases are likely to be signed by 2H2026, a “slight delay” from its earlier guidance of 1Q2026.

Natarajan notes that both tenants are seeking to sign very long leases of over 10 years, while the hospitality portion of the Berlin Campus has already been leased to Stayery and Premier Inn under very long master leases.

IREIT is also in active discussions with its key tenant, Decathlon, which contributes 21% of total income, to remove the lease break options due in 2027, and expects a positive outcome, with the majority of these options being extended. It also does not expect any negative impact from ongoing potential litigation based on its legal counsel’s advice.

Factoring in additional interest costs, adjusting for net property income margins, and increasing the cost of equity by 10 basis points to account for development and market risks, Natarajan has cut his FY2026 and FY2027 DPU by 21% and 17%, respectively.

“While valuations are cheap, with the units trading at 0.5 times P/BV, we await greater clarity and certainty on the Berlin campus lease signing,” says Natarajan. — The Edge Singapore

Ever Glory United

Price target:

PhillipCapital ‘buy’ $1.05

Market-leading M&E player

PhillipCapital’s Chong Yik Ban has upgraded his call on Ever Glory United Holdings (SGX:ZKX![]() ) to “buy” after the group’s revenue and adjusted patmi exceeded expectations in 2HFY2025 ended Dec 31, 2025.

) to “buy” after the group’s revenue and adjusted patmi exceeded expectations in 2HFY2025 ended Dec 31, 2025.

In 2HFY2025, Ever Glory United’s revenue was up by 83.7% y-o-y to $78.2 million, while adjusted patmi rose by 98.2% y-o-y to $6.4 million. Including the $5.5 million bargain purchase of Guthrie Engineering, patmi surged by 269.1% y-o-y to $11.9 million. Chong previously had an “accumulate” call on the counter.

FY2025 revenue and adjusted patmi, which stood at $106.7 million and $11.1 million, respectively, were 128% and 122% of Chong’s forecasts.

“We believe Ever Glory is one of the largest M&E (mechanical and electrical) players in Singapore following its acquisition of Guthrie,” says Chong in his March 9 report.

Guthrie, which has a strong track record of landmark projects in Singapore, such as runway lighting at Changi Airport, will lead Ever Glory in securing more high-value contracts moving forward, including the construction of Changi Airport’s Terminal 5 and airport electrical contracts, Chong notes. Other contracts may also include MRT tunnel lighting by the Land Transport Authority and hospital contracts.

In addition to his upgrade, Chong has increased his target price to $1.05 from 81 cents. This is based on an FY2027 P/E of 18 times, as per his previous calculations, which used a blended P/E for FY2026–FY2027. The new P/E multiple represents a 10% discount to Ever Glory’s peers’ two-year forward P/E of 20 times.

Looking ahead, Chong expects Ever Glory’s revenue to grow at a CAGR of 25% for the next two years, while adjusted patmi is tipped to grow at a CAGR of 36% over the same period. Both figures are supported by the group’s record order book of $733 million, which is expected to last four to five years, with significant recognition towards the latter part of the period. — Felicia Tan

Wilmar International

Price target:

Maybank Securities ‘buy’ $3.85

Regulatory overhang ‘largely behind’

Hussaini Saifee of Maybank Securities has upgraded his call for Wilmar International (SGX:F34![]() ) from “hold” to “buy”, along with a higher target price of $3.85, up from $3.12 previously.

) from “hold” to “buy”, along with a higher target price of $3.85, up from $3.12 previously.

As observed by Saifee in his March 10 note, the agri-food giant delivered what are deemed “resilient” numbers for FY2025 ended Dec 31, with core earnings up 10% y-o-y and revenue up 5%, thanks to growing volumes, stable pricing and improved product mix.

Saifee notes that Wilmar has flagged geopolitical and operating headwinds. Nonetheless, he sees a “constructive” outlook, with Wilmar guiding food products to mid-single-digit volume growth and newer categories such as flour, rice and noodles to double-digit growth. “Global supply-demand dynamics support stable pricing and positive refining margins in Indonesia and Malaysia,” he adds.

Also, while soybean crushing margins are expected to soften, plantation output was weak in early 2026, although Saifee expects a recovery.

In addition, Wilmar, saddled with regulatory issues in its major markets of Indonesia and China, should see these overhangs “largely behind” and with “adequate” provisions in place.

Specifically, Wilmar has booked US$782 million ($996 million) for Indonesia-related matters, US$104 million for its legal cases in China, and US$150 million linked to irregularities at its Pakistan associate, notes Saifee.

The war between the US, Israel and Iran has roiled the oil market but is seen to have a mixed impact on Wilmar.

“While elevated crude could support biofuels & integrated spreads offer some buffer, higher freight and insurance costs, plus potential demand softness if conflict escalates, may be the offsetting factors,” reasons Saifee.

Meanwhile, a weaker US dollar also provides an incremental earnings tailwind, estimates Saifee, who has raised his earnings forecasts by 6% for the current FY2026 and 7% for the coming FY2027, which has led to the higher target price.

Last but not least, with earnings on an upward trajectory, lower leverage and a more flexible balance sheet, there is scope for Wilmar to pay more dividends, says Saifee, who is projecting a payout of between 16 and 17 cents. In contrast, Wilmar is paying a total of 14 cents for FY2025. — The Edge Singapore