Yet in healthcare, education and media, we continue to accept this trade-off as inevitable. It is not.

There is a third model — misunderstood, less discussed but increasingly relevant: private enterprises that generate profit, but do not extract the profit. It is often referred to as private not-for-profit enterprise.

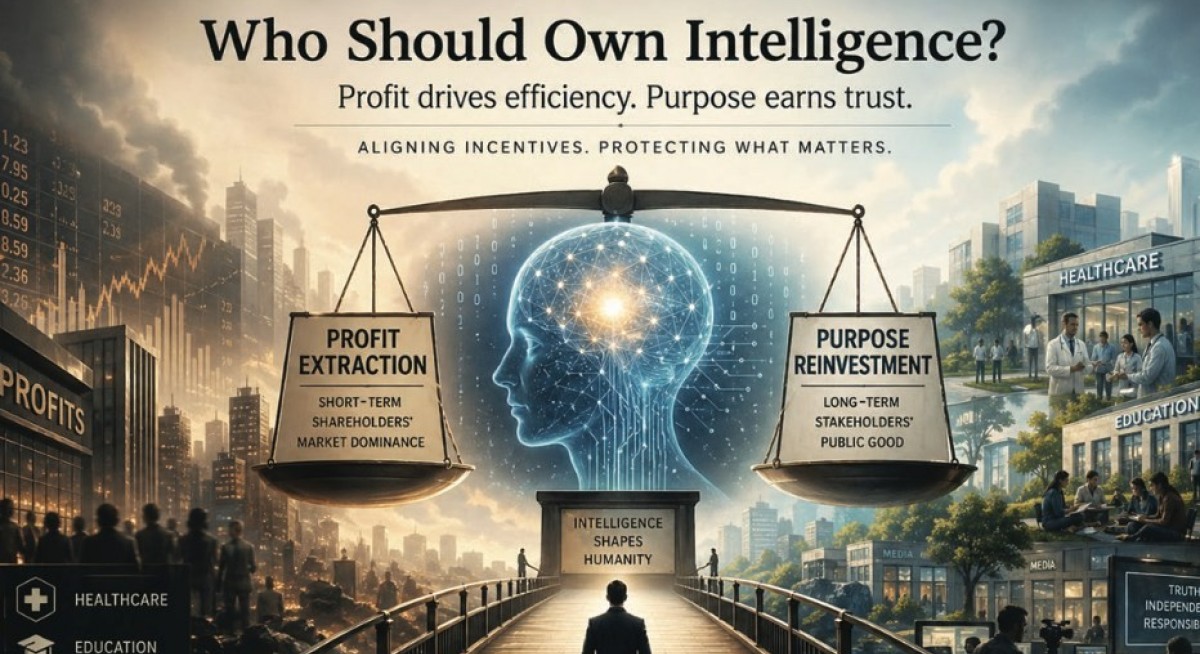

A misunderstood model

A private not-for-profit enterprise is often misunderstood as a charity. It is not. It operates with the same commercial discipline as any private company — charging fees, managing costs, competing for talent and generating surpluses.

See also: The future of media in the AI age (Part 7/9): The interpretation economy

The difference lies not in how it is run, but what it does with the profit.

Instead of distributing earnings to shareholders, it retains and reinvests them into its mission — improving services, lowering costs or expanding access. In other words, it is run like a business but owned by its purpose.

The real problem is incentives

See also: A recurring pattern in the history of information

At the heart of the issue is not ideology, but incentives.

Essential services are not ordinary markets. These are basic necessities, not discretionary goods. They are built on trust, judgement and information asymmetry. Yet, they are increasingly run like profit-maximising businesses.

- A patient cannot fully evaluate a diagnosis.

- A student cannot price the long-term value of a degree.

- A reader cannot verify every claim they consume.

Yet we run these sectors as if they were ordinary transactions. The distortions are predictable.

- In healthcare, more procedures, more tests, longer hospital stays than justified, more billing complexity.

- In education, escalating tuition fees and credential inflation that expand faster than capacity, quality and employment potentials.

- In media, editorial lines are shaped by advertisers, silence on powerful corporate interests and attention-driven content crowding out substance, clarity and scrutiny.

When truth competes with revenue, revenue usually wins. This is not a failure of capitalism. It is a failure of misapplied incentives.

The next frontier: Intelligence itself

For more stories about where money flows, click here for Capital Section

If these tensions are already visible in healthcare, education and media, they become far more consequential in artificial intelligence (AI).

AI is not merely another industry. It is rapidly becoming a foundational layer that mediates information, shapes judgement and increasingly influences decisions at scale.

In media, incentives influence what is published. In healthcare, incentives influence what is prescribed. In AI, incentives may influence how reality itself is interpreted and acted upon. If media shapes narratives, AI may shape reasoning itself. (Scan the QR code for more on the subject in the article, “AI isn’t coming for your job. It’s coming for your mind”.)

When profit shapes intelligence

The same structural problem reappears — but amplified.

When AI systems are developed under purely profit-maximising models, incentives do not disappear. They scale.

Models are optimised for engagement rather than truth. Capabilities may be released ahead of safety. Closed ecosystems may prioritise dominance over openness. The risk is no longer just overcharging or bias.

It is that the system through which people access knowledge and make decisions becomes subtly aligned to commercial objectives. At that point, profit is no longer influencing outcomes. It is influencing how outcomes are understood.

Why this cannot be left to the binary

Yet it would be naïve to conclude that AI should be removed from private enterprise altogether. The pace, scale and capital required to build advanced AI system are unprecedented. Private firms are pushing the frontier precisely because they can mobilise resources, talent and risk taking.

But this only sharpens the dilemma. Left purely to profit, incentives may diverge from social outcomes. Removed entirely from private enterprise, progress may stall — or shift to less accountable domain.

The familiar binary — state versus market — breaks down. Read our article, “Rethinking the 'State vs Private' debate” (The Edge, May 4, 2026).

Proof that a third path exists

Some of the most trusted institutions already follow this model.

In healthcare, organisations such as the Mayo Clinic and Cleveland Clinic are among the most respected in the world. Their doctors are salaried, not paid per procedure. The system is designed to optimise outcomes, not volume and revenue.

In media, the Scott Trust exists to safeguard the independence of The Guardian. It has no shareholders to satisfy, and no quarterly earnings to defend.

Even the world’s leading universities — Harvard and Oxford — operate as not-for-profit institutions. They charge fees, generate surplus and compete globally. But profits are not extracted. It is reinvested into mission, reputation and longevity.

These are not charitable afterthoughts. They are not fringe experiments.

Why does this matter now?

Because trust is eroding.

- Patients increasingly question whether treatments are necessary.

- Students question whether degrees are worth the cost.

- Readers question whether what they read is influenced.

The underlying suspicion is the same: am I being served, or monetised?

At the same time, these sectors are becoming more complex. These sectors are not transactional. They rely on judgement that cannot easily verified. This creates information asymmetry — where providers hold power. In such environments, profit maximisation becomes dangerous.

When profit maximisation enters systems built on trust, reputational capital and intergenerational outcomes, the consequences are not just inefficiency. They are structural.

For AI — a structural necessity?

The institutions that build and control advanced AI systems may need to operate with the discipline and capability of private firms, but without the imperative to extract profit at the expense of long-term trust and safety.

In such a model, surplus is not the objective, but a means — reinvested into alignment, robustness, accessibility and long-term development. Because in AI, the cost of misaligned incentives is not measured only in inefficiency. It is measured in how decisions are made, how truth is understood and, ultimately, how societies function. Scan QR code for The New Yorker article, “Sam Altman May Control Our Future – Can He Be Trusted?” (April 6, 2026).

But not-for-profit is not a panacea

But it would be naïve to romanticise the not-for-profit model.

Removing profit does not automatically create virtue. Profits, for all the flaws, provide something essential: discipline. It forces trade-offs. It punishes failure. It rewards efficiency.

Remove it, and new risks emerge — complacency, bureaucracy, entrenched management and mission drift disguised as virtue.

Many not-for-profit institutions fail not because they lack purpose, but because they lack pressure.

Without shareholders:

Who demands performance?

Who forces tough decisions?

Who shuts down failure?

The uncomfortable truth is this: removing bad incentives does not automatically create good ones.

If this model is to work, it must replace profit with something equally rigorous. That means governance with real authority — boards that can act, not just advise. It means transparency based on outcomes, not activity — patient results, learning quality and editorial trust. It means external benchmarking, so performance is measured, not assumed. And it means leadership incentives tied to mission, not scale, so growth does not quietly become a substitute for profit.

Without these, this model is not a solution. It is simply a different failure mode.

The real question: Where should profit be allowed?

None of these arguments suggest profit has no place. In consumer goods, technology, manufacturing — it drives innovation, efficiency and scale.

But in sectors where trust is foundational, outcomes are hard to verify, and consequences are societal, the cost of misaligned incentives is too high.

In healthcare, it can cost lives. In education, it shapes generations. In media, it distorts reality itself. In AI, it may shape how reality itself is understood.

These are not markets where “buyer beware” is sufficient.

The future will not be ideological. Governments will still play a role in ensuring access and regulation. For-profit firms will continue to drive innovation.

But private not-for-profit institutions (or purpose-owned private enterprises) may become something more important: anchors of trust. Not because they are morally superior, but because their structure aligns incentives with purpose.

Conclusion: Rebuilding trust through structure

In the end, this is not about choosing between state and market. It is not about profit versus purpose.

It is recognising a harder truth. When profit becomes the objective in systems that depend on trust, trust erodes. When it enters systems that shape intelligence itself, the consequences compound. And once eroded, it cannot simply be priced back in.

This model is not a perfect answer. But it is a serious attempt to solve the right problem. Run with the discipline of the private sector. But serve with the purpose of the public good.

Because the question is no longer whether we can afford to remove profit from these systems — but whether we can afford to let the architecture of truth, judgement and intelligence be driven by it.

Note: Look out for our upcoming articles on AI and a series of articles on the future of media in the AI age.

Portfolio commentary

The Malaysian portfolio was up 0.4% for the week ended May 6. The biggest winners were LPI Capital (+4.0%), Hong Leong Industries (+2.9%) and Maybank (+1.6%), while the only loser was United Plantations (-4.2%). Total portfolio returns now stand at 216.6% since inception. This portfolio is outperforming the benchmark FBM KLCI, which is down 4.0% over the same period, by a long, long way.

The Absolute Returns Portfolio, meanwhile, gained 1.4%, lifting total portfolio returns to 38.0% since inception. We added Schneider Electric to our portfolio last week and the stock has gained 6.7% since then. Sun Hung Kai Properties (+4.4%) and SPDR Gold Minishares Trust (+3.2%) were the other notable gainers while the two losing stocks were Berkshire Hathaway (-1.2%) and ChinaAMC Hang Seng Biotech (-0.9%).

The AI portfolio outperformed last week, up 4.9%, with all stocks ending in positive territory. The top gainers were Marvell (+10.0%), Cadence Design (+7.6%) and Datadog (+7.3%). We disposed of all our holdings in RoboSense Technology and reinvested the proceeds into HP Enterprise. Total portfolio returns improved to 9.2% since inception.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks, including the particular stocks mentioned herein. It does not take into account an individual investor’s particular financial situation, investment objectives, investment horizon, risk profile and/or risk preference. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.