Overlooked proxy to the construction boom

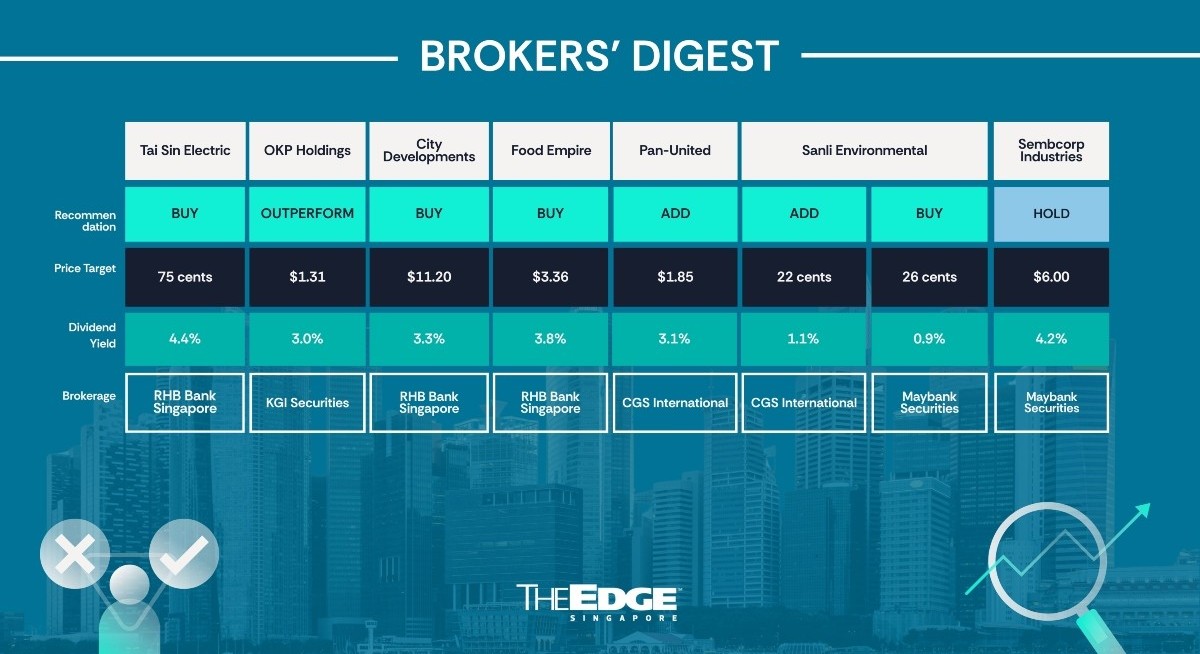

RHB’s Syahril Hanafiah has initiated coverage on electric infrastructure solutions provider Tai Sin Electric (TSE) (SGX:500![]() ) with a “buy” call and a target price of 75 cents.

) with a “buy” call and a target price of 75 cents.

“TSE is poised to benefit from strong domestic construction demand and rising data centre investments. We view TSE as an overlooked yet essential proxy for the construction boom,” says Syahril in his initiation report dated June 4.

According to the analyst, TSE is a beneficiary of the strong domestic construction demand. “As a long-established cable manufacturing player, TSE has benefited from various mega projects in the past, such as Thomson-East Coast MRT Line, Tuas Mega Port and Changi Airport T4, and remains well-positioned to capitalise on the ongoing construction boom,” he adds.

See also: UOBKH maintains 'buy' and 71 cents target price on LHN

Apart from the booming construction demand, Syahril notes that TSE is becoming a regional data centre play, benefiting from the wave across its cable and electrical component segments.

“It has supplied over 70% of Singapore’s data centres, supporting steady revenue growth in FY2025 and 1HFY2026, alongside public construction activity in Singapore and Malaysia,” the analyst states.

Syahril believes that with 1 gigawatt of data centre capacity in Singapore’s development pipeline, TSE is set to benefit from the next wave of demand.

See also: CGS International maintains 'add' call on Sembcorp with target price of $7.68

Meanwhile, TSE has been expanding its footprint in the renewable energy space through the acquisition of solar equipment distributors, Integra RE, in Thailand and the Philippines.

From Syahril’s perspective, this will allow TSE to establish business relationships with RE players in both markets where it previously had no direct presence.

Despite the solid underlying demand for TSE’s cable and electrical components segment, Syahril notes that TSE’s margins are vulnerable to copper price swings. “In 1HFY2026, the group recorded an $11.8 million onerous contract provision following a sharp surge in copper prices, which compressed margins,” Syahril states.

Syahril adds that while further price increases may weigh on earnings, this is partly offset by higher-margin spot contracts and a weaker US dollar.

“We expect provisions to peak at $18.5 million in FY2026, compared to $12.6 million back in 1HFY2026, before reversing by $5.3 million in FY2027 and FY2028, and believe the market should look beyond this, given TSE’s strong fundamentals,” Syahril predicts.

With that, the analyst expects TSE’s core earnings to grow 33% y-o-y in FY2026, driven by strong contract delivery, despite margin pressure expected in 2HFY2026.

“Growth would then slow to 3.2% y-o-y in FY2027 due to fulfilment of onerous contracts, before recovering to 13.8% y-o-y in FY2028 as margins normalise with stabilising copper prices and higher-margin spot contracts,” Syahril adds.

For more stories about where money flows, click here for Capital Section

“Our target price of 75 cents on TSE is pegged to a 12 times FY2027 P/E ratio, at a 10% discount to its closest peer, due to its relatively small size,” Syahril concludes. — Teo Zheng Long

OKP Holdings

Price target:

KGI Securities ‘outperform’ $1.31

Multi-year earnings visibility

Chen Guangzhi of KGI Securities has initiated coverage of construction firm OKP Holdings (SGX:5CF![]() ) with a bullish “outperform” call and a $1.31 price target, citing the ongoing multi-year infrastructure upcycle, which supports the company’s order book replenishment.

) with a bullish “outperform” call and a $1.31 price target, citing the ongoing multi-year infrastructure upcycle, which supports the company’s order book replenishment.

“OKP is well positioned to benefit from Singapore’s sustained infrastructure investment cycle, supported by public-sector projects in civil engineering, transport connectivity, roads, drainage, commuter infrastructure and active-mobility networks,” says Chen in his June 4 note.

“The structural nature of these projects provides a supportive tender pipeline and reinforces OKP’s role as a niche public-infrastructure contractor,” he adds.

Chen notes that with a net order book of $760.7 million as at May 28, including multi-year contracts from LTA, OKP enjoys strong earnings visibility through 2031, which means it can reduce its reliance on short-cycle tender wins and strengthen visibility over medium-term revenue recognition.

Over the years, the company has built up a strong and resilient balance sheet, which gives it the base to bid for more contracts.

“OKP’s sizeable cash position and conservative balance sheet provide an important buffer against project execution risks, cost inflation and working-capital volatility.

“The strong liquidity position also supports performance bonding, procurement flexibility and the ability to bid for larger government-backed infrastructure projects,” adds Chen.

The analyst said that OKP has shown resilience in its margins through disciplined tendering and a track record in the public sector. Although the construction sector faces higher labour, material and energy costs, OKP’s established execution track record, public-sector focus and disciplined bidding approach should support margin stability.

“As industry requirements around manpower, productivity and compliance increase, stronger contractors such as OKP are better positioned to capture quality projects and convert backlog into sustainable earnings,” he adds.

Chen’s target price of $1.31 is based on a discounted cash flow-derived equity valuation with a 10% weighted average cost of capital and a 2% terminal growth rate. — The Edge Singapore

City Developments

Price target:

RHB Bank Singapore ‘buy’ $11.20

Impending strategic review

Vijay Natarajan is staying positive on City Developments (CDL) (SGX:C09![]() ) ahead of its strategic review, expected in the third quarter of this year.

) ahead of its strategic review, expected in the third quarter of this year.

“We expect greater clarity on assets identified of around $5 billion and the timeline for capital recycling, key investment pillars and capital allocation strategies to enhance its flagging return on equity,” says the RHB Bank Singapore analyst in his June 2 note.

“The focused execution of value-unlocking plans remains a key catalyst in narrowing its huge trading discount to its revalued net asset value. This is augmented by the recent strengthening of its board and resilient Singapore market, where it has a dominant presence,” says Natarajan, who is keeping his “buy” call and $11.20 target price.

According to Natarajan, key assets recently identified for divestment by CDL include its legacy UK development platform, valued at around $800 million.

The company has plans to “value unlock” its global living sector portfolio, worth some $4 billion, via a potential injection into a private fund, along with likely changes to its hospitality portfolio.

“While recent interest rate volatility could impact the execution timeline, a clearer articulation of asset-light strategy and identification of core/non-core assets is a key rerating catalyst,” says Natarajan.

Last month, Kwek Leng Peck, who left the board back in 2020 following disagreements over the company’s China strategy, recently rejoined the board in the elevated role of vice-chairman.

Leng Peck is the cousin of CDL’s executive chairman Kwek Leng Beng and the uncle of group CEO Sherman Kwek.

“We believe his reappointment will strengthen the Board’s rigour and lead to more robust deliberations over the group’s divestment and investment strategy, just as CDL embarks on value-unlocking plans,” says Natarajan.

Meanwhile, the analyst notes that the Singapore residential market remains healthy, with CDL’s projects not affected by recent policy changes targeting executive condominiums (ECs), which will take effect only for upcoming land tenders.

CDL has two EC projects in the launch pipeline, and Natarajan expects strong demand as buyers rush in before tighter policy restrictions take effect.

Meanwhile, the high-end Newport Residences, launched in January, saw stronger-than-expected take-up, with around 80% of the 246 units sold year to date at an average of $3,200 psf.

While FY2026 residential sales value is likely to be lower y-o-y due to fewer launches, income contribution is expected to be on par, driven by progressive revenue recognition from earlier-sold projects, says Natarajan. — The Edge Singapore

Food Empire Holdings

Price target:

RHB Bank Singapore ‘buy’ $3.36

Well-poised to capture growth

Alfie Yeo of RHB Bank Singapore has maintained his positive view on Food Empire Holdings (SGX:F03![]() ) , given that the company is well-poised to capture growth as it increases manufacturing capacity across various sites.

) , given that the company is well-poised to capture growth as it increases manufacturing capacity across various sites.

In addition, the company’s cost pressure is easing somewhat, with coffee prices down by around a quarter year to date, on better-than-anticipated supply, harvest, and weather outlooks from key production countries, including Brazil and Vietnam.

“We expect this to lend support to our margin projection in the future. Food Empire continues to track well with our estimates,” says Yeo, who has kept his “buy” call, noting that the stock is trading at a “compelling” Price/EPS growth (PEG) ratio of less than 1, with its forward P/E of 16 times below his 19% FY2025–FY2028 earnings growth CAGR.

Yeo notes that the company’s capacity expansion plans remain intact, with operations at its Kazakhstan manufacturing facility beginning in the first quarter of the year.

Next, the company is expected to increase its spray-dried soluble coffee manufacturing capacity in India by around 60% by FY2027.

Its new Vietnam freeze-dried soluble manufacturing facility will then come on stream by FY2028.

In its May 13 business update, the company reported revenue of US$160 million ($206 million), an increase of 17% y-o-y, with all its markets reporting healthy growth. Russia, in particular, was up 29% y-o-y to US$51 million, driven by higher volumes and selling prices.

Yeo notes that the company’s 1QFY2026 revenue tracks in line with his full-year revenue forecast of 15% y-o-y; thus, he has left his earnings estimates unchanged for now.

Meanwhile, in conjunction with its 1QFY2026 business update, the company has also announced a one-for-five bonus issue, with a June 4 record date. Yeo’s post-bonus-issue target price has been adjusted to $3.36, down from the pre-bonus target price of $3.87.

For Yeo, downside risks to his forecasts include operational disruptions due to the Russia-Ukraine conflict and adverse effects from changes in the value of the ruble and other CIS currencies. — The Edge Singapore

Pan-United Corp

Price target:

CGS International ‘add’ $1.85

Positive industry momentum

Pan-United Corp’s (SGX:P52![]() ) share price has dropped more than 10% from its recent peak of $1.73 more than a fortnight ago. Still, Natalie Ong of CGS International (CGSI) has not only maintained her positive view of this stock but also raised her target price from $1.55 to $1.85, citing the company’s strong balance sheet amid bustling construction activity.

) share price has dropped more than 10% from its recent peak of $1.73 more than a fortnight ago. Still, Natalie Ong of CGS International (CGSI) has not only maintained her positive view of this stock but also raised her target price from $1.55 to $1.85, citing the company’s strong balance sheet amid bustling construction activity.

In the first quarter of the year, demand for ready-mixed concrete (RMC) was up 29% y-o-y to 4 million cubic metres, according to the Building and Construction Authority (BCA).

At this level, the demand for this key building material - in which Pan-United is the largest supplier in town with a market share of around 40%- is tracking the upper range of the full-year forecast of 15 to 16 million tonnes.

Ong points out that historically, demand in the second half of the year tends to be stronger. “As such, we think 2026 demand could reach or surpass BCA’s RMC demand forecast, in line with our 2026 ready-mixed concrete forecast of 16.5 million cubic metres,” she says.

Ong notes that ready-mixed concrete players have largely been able to pass on the higher cost of cement, with prices rising 14% y-o-y to $136 per tonne versus the 16% y-o-y increase in cement prices over the January to March period.

The industry has been flagging rising operating costs, no thanks to higher energy costs driven by the fighting in the Middle East.

Ong points out that the majority of the company’s customer contracts are based on variable/indexed pricing. “As such, we believe that Pan-United has been able to raise average selling prices to pass through the majority of inflationary costs, keeping margins largely protected, giving it an edge compared with its building material/construction peers who have a larger proportion of fixed-price contracts,” she says.

Now, given the inflationary environment, she warns that the company could face a slight deterioration in cash balances and an increase in accounts receivable as higher input and operating costs increase working capital needs.

In its AGM minutes published on May 15, the company says that, in addition to assessing its customers’ creditworthiness, it purchases credit insurance for most of its customers to protect itself against non-payment.

Meanwhile, Ong believes that the company’s net cash, at a “healthy” $93 million as at the end of FY2026, will support her 60% payout ratio assumption, which translates to a 50% jump in dividend per share for FY2026.

In addition, the company has been supporting the share price through buybacks totalling 807,700 shares as of June 4, representing 0.15% of its outstanding shares. It only obtained the mandate to do so on April 23.

Ong has raised her valuation multiple on the stock from 7.4 times EV/Ebitda, based on 0.5 sd of Pan-United’s historical level, to 9 times FY2027 EV/Ebitda, which is 1.4 standard deviations above the 14-year forward level.

She remains upbeat on this stock, given its strong positioning, which should help it capture construction tailwinds, and its improved balance sheet strength.

For Ong, re-rating catalysts include strong industry volume growth and sustained margin strength. On the other hand, downside risks include counterparty credit risks and a slowdown in project offtake volumes, thereby negatively impacting ready-mixed concrete sales and margins. — The Edge Singapore

Sanli Environmental

Price targets:

CGS International ‘add’ 22 cents

Maybank Securities ‘buy’ 26 cents

Cost pressures, delayed revenue recognition

Sanli Environmental’s (SGX:1E3![]() ) FY2026 results were “slightly below” the expectations of Jarick Seet of Maybank Securities, but he expects the current FY2027 to be better. However, given concerns that margins will be hurt by higher raw material costs and delayed revenue recognition, Seet has maintained his “buy” call on the stock, but lowered the target price to 26 cents from 31 cents.

) FY2026 results were “slightly below” the expectations of Jarick Seet of Maybank Securities, but he expects the current FY2027 to be better. However, given concerns that margins will be hurt by higher raw material costs and delayed revenue recognition, Seet has maintained his “buy” call on the stock, but lowered the target price to 26 cents from 31 cents.

For FY2026 ended March, Sanli reported earnings of $2.2 million on revenue of $139.6 million, down 11.4%, mainly due to extended project timelines at one of its existing Tuas projects, which delayed revenue recognition to 2027.

The company was in the news earlier when it announced that a key customer is seeking liquidated damages. This case is pending. “We believe the relationship with this key customer remains strong, as the delayed project has been underway for a long time. Sanli has continued to secure significant contracts from the same customer, including another $13.7 million contract with its major customer for maintenance-related services secured in 1Q2026,” adds Seet.

Seet believes that this year will be one in which Sanli will focus more on execution than on securing new orders. For now, the company’s orders on hand have reached $748.1 million. “Better execution will be vital to any potential uplift in earnings in the future. Sanli will still be tendering for projects, but it will be more selective in future tenders, opting only for higher-margin projects, and potentially moving into the private sector,” he says.

Meanwhile, given the delay in project delivery and the higher costs incurred, Seet has lowered his FY2027 gross profit margin from 18% to 14.7%. As a result, his earnings estimates for FY2027 and FY2028 have been lowered by 21% and 28%, respectively. Applying the same 15.5 times FY2028 valuation, Seet’s target price for this counter has been reduced to 26 cents.

In his separate note, William Tng of CGS International has also cut his target price for this company, while keeping his “add” call, given that earnings growth remains intact. “Sanli needs to convince investors that it can translate these orders into higher net profit,” says Tng in his June 5 note.

With revenue recognition deferred due to delays from other contractors on the projects, he has reduced his FY2027 revenue and earnings forecasts by 29.1% and 23.5% and his FY2028 forecasts by 39.1% and 33.1%.

Key re-rating catalysts, according to him, are higher-than-expected order wins and margin expansion, and faster progress in its magnesium hydroxide slurry production business.

On the other hand, downside risks include unfavourable government policy, such as higher local labour content requirements or levies that may impact margins, as well as more intense industry competition, which may lead to compressed margins. Shortage of workers, poor project management and execution, and lack of access to funding to execute its new order wins are also possible risks. — The Edge Singapore

Sembcorp Industries

Price target:

Maybank Securities ‘hold’ $6

New project participation in Middle East

Krishna Guha of Maybank Securities has raised his target price for Sembcorp Industries (SGX:U96![]() ) from $5.60 to $6 after news that the utilities company has been selected by the Emirates Water and Electricity Company as one of the minority partners in a 2.6 gigawatt (GW) independent power producer project.

) from $5.60 to $6 after news that the utilities company has been selected by the Emirates Water and Electricity Company as one of the minority partners in a 2.6 gigawatt (GW) independent power producer project.

Leading regional utilities firm TAQA will own a 60% stake in the development and a 40% stake in the operations and maintenance (O&M) company. Sembcorp, meanwhile, will have a 20% stake in the development and a 30% stake in the O&M company.

Under the terms of a 21-year power purchase agreement, EWEC will be the sole procurer on a take-or-pay basis for the electricity generated and the agreement will include risk-mitigation provisions in light of the latest regional developments. The plant is expected to begin commercial operations in 2029.

This project will deliver sustainability and cost benefits, with one of the region’s lowest capital expenditure rates per kilowatt-hour and the lowest levelized cost of electricity. “The project underscores Sembcorp’s longstanding partnerships in the region. TAQA and EWEC are Sembcorp’s partner and customer, respectively, in the Fujairah IWPP project,” says Guha, referring to an existing water and power plant in the UAE.

Guha, in his June 8 note, has factored in recent operational trends in renewables, gas and related services, which have led to a 5%–8% cut to his core patmi estimates. However, he has a new target price of $6 after rolling forward his SOTP model.

For now, Guha has lowered his core FY2026 patmi estimates for Sembcorp by 8.5% and his FY2027 estimates by 5.1%, respectively, to account for lower contributions from renewables and integrated urban solutions, as well as lower contracting spreads for Senoko, one of Sembcorp’s key power-generating assets in Singapore.

This counter remains a “hold” for him due to continued earnings consolidation, potential M&A integration risk and higher gearing. — The Edge Singapore