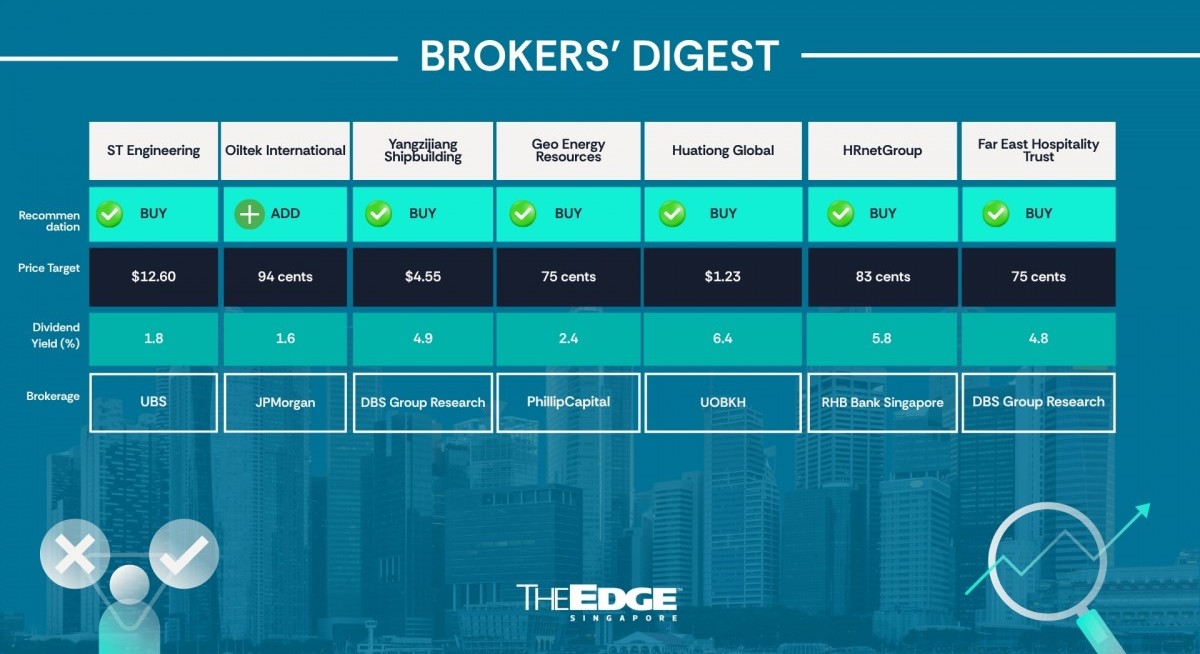

DBS Group Research ‘buy’ $4.55

‘Landlord of the ocean’

DBS Group Research has maintained its “buy” call and $4.55 target price for Yangzijiang Shipbuilding following news that it plans to acquire a 10% stake in one of its long-time customers, which accounts for 10%–15% of its order book.

Under terms of a deal announced on March 10, Yangzijiang will pay US$825.7 million ($1.056 billion) in cash for the stake in Poseidon Corp, indirect parent company of the customer, Seaspan Corp. The acquisition will be funded entirely from Yangzijiang’s existing net cash of some US$3 billion.

See also: JP Morgan reiterates overweight for CLI as it ramps up listed and unlisted FUM

Seaspon Corp is described as the world’s largest independent containership lessor, leasing ships to shipping lines at multi-year fixed rates, providing clear cash flow visibility. DBS calls it the “landlord” of the ocean.

DBS says Seaspan is the world’s largest independent containership lessor, with a young, scaled fleet of 190 vessels totalling 1.92 million twenty-foot equivalent units (TEUs), representing around 6% of global containership capacity and around 14% market share of leased containerships.

Yangzijiang explains that by taking a strategic stake in a major customer, it can gain better visibility into industry dynamics, as it will have a board seat upon completion of the deal.

See also: CGSI and DBS like Thai Beverage with Vietnamese milk

In parallel, an entity privately controlled by Yangzijiang’s executive chairman, Ren Letian, is also taking a separate 5% stake in Poesidon Corp.

Seaspan’s earnings have compounded strongly in the past five years, with patmi rising from US$134 million in FY2020 to US$740 million in FY2025 as the fleet grew from 127 to 190 ships and from 1.07 million to 1.92 million TEU, supported by strong container markets and long-term contract coverage.

DBS says that Seaspon has a clear growth path ahead, with 70 vessels on order, which will increase its fleet size by 36% to 2.62 million TEU by FY2028, providing visibility into earnings growth over the next three years.

At a purchase price of US$825.7 million, the deal is valued at 1.8 times Seaspan’s FY2025 book value of US$459 million and 11.2 times its FY2025 net profit of US$74 million.

From the perspective of DBS, this deal seems “justifiable” given a return on equity of around 17% and a 21% earnings CAGR during 2021–2025, with a potential 10% CAGR ahead, backed by fleet growth.

DBS estimates that the acquisition will accrete annualised profit of over RMB300 million ($55.6 million), or 3% of Yangzijiang’s bottom line and lift ROE by 0.8 percentage points.

“More importantly, the investment strengthens a long‑standing shipowner relationship and supports vertical integration along the containership value chain.

For more stories about where money flows, click here for Capital Section

“Being on the board of a large, growing and relatively young fleet owner gives Yangzijiang line‑of‑sight into replacement and growth needs, improving orderbook visibility and reducing yard cyclicality,” says DBS — The Edge Singapore

Oiltek International

Price target:

CGS International ‘add’ 94 cents

Beneficiary of volatile geopolitics

Krishna Guha of Maybank Securities has upgraded his call on Singapore Technologies Engineering (ST Engineering) from “hold” to “buy”, given that the company is likely to be a key beneficiary of rising global defence spending and the growing use of unmanned systems, such as drones, in warfare.

“In an era of unpredictable geopolitics, global defence spending is on the rise. Historically, global defence spending has averaged 4.5% of GDP pre-1990 and 2.4% since then,” Guha writes in a joint report on March 14 with his colleague Jarick Seet.

“Since 2021, Europe, the Middle East, North Africa and Japan have contributed to the growth of military expenditure with increases ranging from 0.4 percentage point to 1 percentage point of their GDP. Singapore is also stepping up defence spending with 2.9% of GDP, or 18.1% of government expenditure, earmarked for defence in the FY2026 budget,” they add.

“Commentary suggests the Singapore government is prepared to spend more than the usual 3% of GDP on defence if the need arises. Improving the ability to deploy, counter and operate alongside unmanned systems, such as drones, received special mention in the latest budget, along with strengthening Singapore’s cybersecurity capabilities,” they continue.

He notes that the company’s order book of around $33.2 billion as at end-December 2025, was largely driven by $18.7 billion in new contract wins last year. Of the figure, half come from the defence and public security business; international defence sales in Europe and the Middle East doubled in the year, the analyst notes.

Guha has increased his earnings estimates for ST Engineering by 0.5%, 2.6%, and 2.5% for FY2026, FY2027, and FY2028, respectively, as he expects higher revenue from the group’s defence and commercial aerospace businesses.

His new target price implies a blended FY2027/FY2028 multiple of 32 times, backed by a 15% patmi CAGR from FY2025 to FY2028.

From his previous target price of $9.50, Guha now estimates that ST Engineering is worth $12.50, aligning with the broader sell-side consensus, which has raised target prices for this counter above $11.

Earlier, on March 5, Bank of America’s Jessie Lo and Mcrid Wang also turned bullish on ST Engineering. “We previously had a conservative view on ST Engineering, as we believed the Europe’s focus on sovereignty, as well as ST Engineering’s limited track record, were constraining prospects for major order gains,” state the analysts. “We now turn more constructive on the company.”

According to Lo and Wang, their reasons include increasing order‑win potential as a diversified defence supplier outside Europe and the US, margin improvement across businesses driven by scale, and potential recovery in the company’s satcom business following a hefty impairment. They now rate this stock “buy”, from “underperform” earlier.

From an earlier target price of $7.80, which is based on 23 times FY2026 earnings, they now believe this stock is worth $12.20, based on a much higher multiple of 35 times.

On March 17, a team of JP Morgan analysts also turned slightly more bullish on this stock, raising their target price from $12.20 to $12.30. While the company maintained its guidance, JP Morgan sees potential upside to its earnings forecasts, due to a stronger-than-expected pick-up in defence-related orders from customers outside Singapore. ST Engineering has strong growth potential in its commercial aerospace and urban solutions segments. However, investors are now “laser-focused” on its international defence momentum, especially in the context of modern warfare and the rapid evolution in demand for drone countermeasures, missiles and ammunition, says JP Morgan.

The company’s willingness to localise and transfer technology, as well as its asset-light approach and partnerships for technology transfer and production, were seen as key differentiators in a market where supplier diversification and rapid delivery are now critical. “While some tendering may pause in the near term, the cyclical uplift in defence spending is expected to persist, and ST Engineering’s multi-domain capabilities and production scale are positioning it to capture sustained demand as modern warfare evolves,” says JP Morgan.

It expects ST Engineering to achieve a 10% CAGR in revenue between FY2026 and FY2028. However, as margins expand, the company’s recurring profit is expected to grow at a CAGR of 20% over the same period. JP Morgan has applied the same 35 times industry valuation multiple to ST Engineering’s FY2026 earnings estimate to derive a revised target price of $12.30. “The multiple is undemanding, given the better-than-peers’ earnings growth, ROE profile and dividend yield, in addition to the aerospace & defence capex upcycle, strong order book and margin delivery.” — Felicia Tan

ST Engineering

Price targets:

Maybank Securities ‘buy’ $12.50

Bank of America ‘buy’ $12.20

JP Morgan ‘overweight’ $12.30

UBS ‘buy’ $12.60

Beneficiary of volatile geopolitics

As the attacks on Iran drags into nearly a month, Singapore Technologies Engineering (ST Engineering), while not directly exposed, has enjoyed a new wave of upgrades from various analysts, as they all perk up with the stronger growth potential of its defence business.

Krishna Guha of Maybank Securities has upgraded his call on ST Engineering from “hold” to “buy”, given that the company is likely to be a key beneficiary of rising global defence spending and the growing use of unmanned systems, such as drones, in warfare.

“In an era of unpredictable geopolitics, global defence spending is on the rise. Historically, global defence spending has averaged 4.5% of GDP pre-1990 and 2.4% since then,” Guha writes in a joint report on March 14 with his colleague Jarick Seet.

“Since 2021, Europe, the Middle East, North Africa and Japan have contributed to the growth of military expenditure with increases ranging from 0.4 percentage point to 1 percentage point of their GDP. Singapore is also stepping up defence spending with 2.9% of GDP, or 18.1% of government expenditure, earmarked for defence in the FY2026 budget,” they add.

“Commentary suggests the Singapore government is prepared to spend more than the usual 3% of GDP on defence if the need arises. Improving the ability to deploy, counter and operate alongside unmanned systems, such as drones, received special mention in the latest budget, along with strengthening Singapore’s cybersecurity capabilities,” they continue.

He notes that the company’s order book of around $33.2 billion as at end-December 2025, was largely driven by $18.7 billion in new contract wins last year. Of the figure, half come from the defence and public security business; international defence sales in Europe and the Middle East doubled in the year, the analyst notes.

His new target price implies a blended FY2027/FY2028 multiple of 32 times, backed by a 15% patmi CAGR from FY2025 to FY2028.

From his previous target price of $9.50, Guha now estimates that ST Engineering is worth $12.50, aligning with the broader sell-side consensus, which has raised target prices for this counter above $11.

Earlier, on March 5, Bank of America’s Jessie Lo and Mcrid Wang also turned bullish on ST Engineering. “We previously had a conservative view on ST Engineering, as we believed the Europe’s focus on sovereignty, as well as ST Engineering’s limited track record, were constraining prospects for major order gains,” state the analysts. “We now turn more constructive on the company.”

According to Lo and Wang, their reasons include increasing order‑win potential as a diversified defence supplier outside Europe and the US, margin improvement across businesses driven by scale, and potential recovery in the company’s satcom business following a hefty impairment. They now rate this stock “buy”, from “underperform” earlier.

From an earlier target price of $7.80, which is based on 23 times FY2026 earnings, they now believe this stock is worth $12.20, based on a much higher multiple of 35 times.

On March 17, a team of JP Morgan analysts also turned slightly more bullish on this stock, raising their target price from $12.20 to $12.30. While the company maintained its guidance, JP Morgan sees potential upside to its earnings forecasts, due to a stronger-than-expected pick-up in defence-related orders from customers outside Singapore. ST Engineering has strong growth potential in its commercial aerospace and urban solutions segments. However, investors are now “laser-focused” on its international defence momentum, especially in the context of modern warfare and the rapid evolution in demand for drone countermeasures, missiles and ammunition, says JP Morgan.

The company’s willingness to localise and transfer technology, and its asset-light approach and partnerships for technology transfer and production, were seen as key differentiators in a market where supplier diversification and rapid delivery are now critical.

It expects ST Engineering to achieve a 10% CAGR in revenue between FY2026 and FY2028. However, as margins expand, the company’s recurring profit is expected to grow at a CAGR of 20% over the same period. JP Morgan has applied the same 35 times industry valuation multiple to ST Engineering’s FY2026 earnings estimate to derive a revised target of $12.30. “The multiple is undemanding, given the better-than-peers’ earnings growth, ROE profile and dividend yield, in addition to the aerospace & defence capex upcycle, strong order book and margin delivery.”

On March 18, UBS raised its target price from $10 to $12.60. ST Engineering recently won a $470 million order to service army vehicles for Qatar and is hoping for deals from the region. “We expect this momentum to continue, particularly in the naval and armoured vehicles space, where the addressable market is potentially US$78 billion [$100 billion],” says UBS. — Felicia Tan

Geo Energy Resources

Price target:

PhillipCapital ‘buy’ 75 cents

Trifecta of earnings drivers

Despite FY2025 earnings below expectations, Paul Chew of PhillipCapital has become more bullish on Geo Energy Resources, citing an impending “trifecta” earnings boost from rising coal prices, growing production volumes and additional earnings from its infrastructure investments. From an earlier target price of 59 cents, Chew, in his March 16 note, figures that this counter is worth 75 cents.

In FY2025 ended Dec 31, 2024, Geo Energy’s revenue was 113% of Chew’s expectation. Still, earnings were just 70% of what he projected, which can be attributed to a spike in the tax rate from an estimated 22% to 63%, due to a new taxable income computation based on the local coal price index rather than realised coal prices.

That aside, Chew sees a key positive attribute ahead for the company.

For one, Geo Energy’s new 92km-long hauling road, now under construction for US$190 million ($243.3 million) to bring coal more easily from inland mines to the jetty, is 80% complete. The road will undergo testing and commissioning from April, with commercial usage planned this August and September.

When fully operational, the road and jetty system can handle 50 million tonnes per year. Geo Energy will take up half for its own use and lease the remaining half to nearby miners, with meaningful earnings from leasing fees expected in FY2028.

Chew is projecting 2.5 million tonnes to be shipped through the new infrastructure in 4QFY2026. In reaching his revised target price of 75 cents, Chew has lowered the discount applied to this infrastructure segment from 60% to 50%.

Coal production is set to increase as well, not this year but significantly so in the coming FY2027. Chew estimates production this year to remain the same as FY2025’s 12 million tonnes, but will jump to 20 million tonnes in FY2027. At the same time, coal prices are seen to recover from around US$40 per tonne to US$50 or more, he says.

In addition, with more efficient logistics in place, Chew expects Geo Energy to lower its unit production cost by US$3 per tonne, providing a further lift to earnings.

On March 16, the company announced it had completed a fundraising exercise. Via a placement of 35 million new shares at 42.5 cents each, Geo Energy Resources raised gross proceeds of nearly $15 million. “Our business strategy is executing as planned, with key projects and initiatives progressing on schedule,” says executive chairman Charles Antonny Melati. “This progress, together with the additional capital from the share placement, enhances our financial flexibility to accelerate value creation within our business model.” — The Edge Singapore

Huationg Global

Price target:

UOB Kay Hian ‘buy’ $1.23

Record FY2025 performance

UOB Kay Hian analysts Heidi Mo and Tang Kai Jie have raised their target price for Huationg Global to $1.23 from $1.15, following the construction company’s record-high earnings in FY2025 ended Dec 31, 2025.

In FY2025, Huationg’s earnings rose by 21.1% y-o-y to $19.8 million, exceeding Mo and Tang’s expectations by 10%.

Revenue, which rose by 32% y-o-y to $298.8 million, also surpassed the analysts’ expectations by 17%, thanks to a sharp rebound in 2HFY2025 and the y-o-y increase in civil engineering contracts. The segment contributed 93% of group revenue, which more than offset the dormitory segment, which ended in August 2024.

For FY2026 to FY2027, analysts expect the company’s revenue to be $331 million and $351 million, respectively. Their estimates, raised by 16% to 18%, have factored in stronger execution, order wins and new dormitory contributions.

The analysts have also lowered their margin expectations due to an expected increase in fuel prices, resulting in net profit forecasts of $21.1 million and $22.4 million for FY2026 and FY2027, respectively.

Huationg has re-entered the dormitory segment with a new management contract for a 4,000-bed government-built facility. The contract will contribute about $3 million to $4 million in net profits in FY2026. “This contract revives a high-margin income stream and keeps the group well-positioned for future dormitory tenders,” say Mo and Tang.

As at the end of FY2025, Huationg’s orderbook stood at $535 million, as the group continues to participate in major infrastructure projects such as Changi Airport’s Terminal 5, the Cross Island Line and Tuas Megaport. The group also has potential upside from tenders for Tengah Air Base, Pulau Tekong and future Changi developments. “These projects typically engage early-cycle civil contractors, aligning well with Huationg’s capabilities,” Mo and Tang add.

The analysts, who have kept their “buy” call on the stock, believe a potential transfer to the Mainboard could trigger a re-rating.

“As a profitable, dividend-paying company with over $150 million market cap and a consistent track record, Huationg meets the key eligibility criteria for a transfer from the Catalist board to the SGX Mainboard,” the analysts write. “A successful transfer would elevate visibility, improve liquidity and increase the investor base, supporting a potential re-rating.” — Felicia Tan