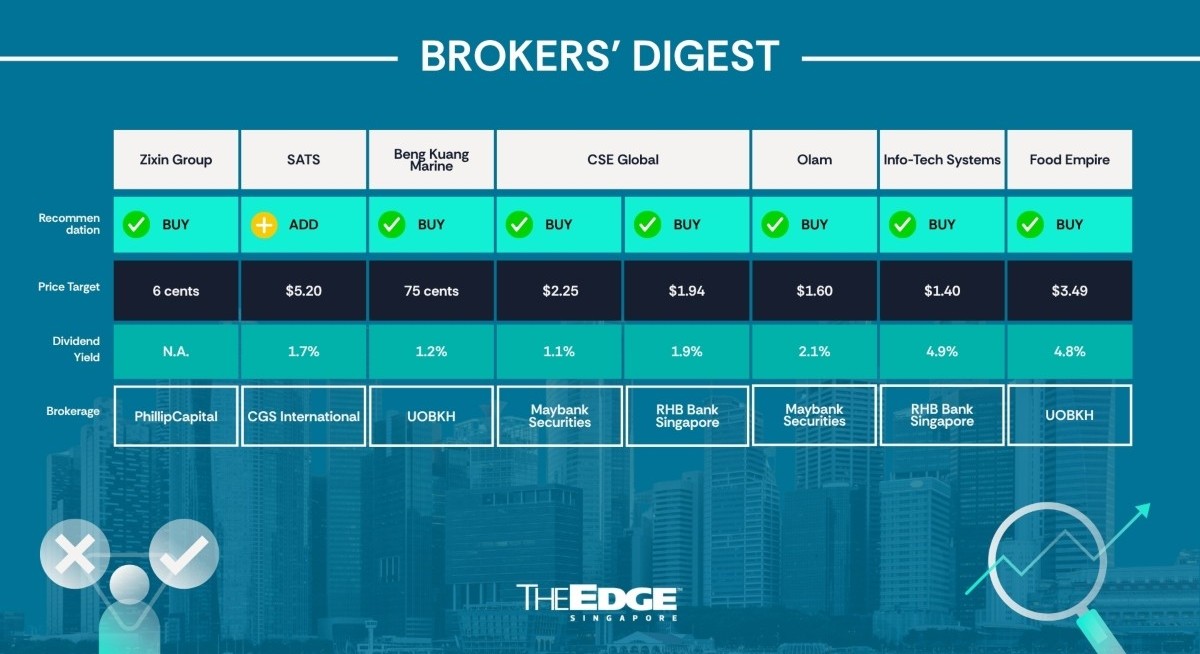

Sustained growth

Serena Lim Yi Qi and Paul Chew of PhillipCapital have maintained their upbeat call on sweet potato company Zixin Group (SGX:42W![]() ) after its 2HFY2026 earnings exceeded expectations.

) after its 2HFY2026 earnings exceeded expectations.

For the six months to March, Zixin reported earnings of RMB45.4 million ($8.7 million), up 29.9% y-o-y, with revenue up 44.3% to RMB386.8 million, driven by higher sales volumes. This brings its full-year FY2026 earnings to RMB61.4 million, up 43.8%, and revenue of RMB607.5 million, up 43%.

The company reported a “robust” performance in the fresh sweet potato segment, with earnings nearly doubling thanks to higher sales volume.

See also: OCBC keeps ‘buy’ on OUE REIT following proposed divestment of Crowne Plaza Changi Airport

According to the analysts, the volume growth was supported by the company’s smart warehouse infrastructure, which extends the shelf life of produce and reduces spoilage, allowing a higher percentage of inventory to be directed to revenue-generating sales channels.

Moving forward, Zixin is bracing for pressure on its margins, no thanks to higher costs, including fertiliser costs. Even so, Zixin expects sales volume growth to offset these headwinds, the analysts say.

For the processed products segment, Zixin also enjoyed steady growth, with earnings up 12.5% y-o-y. Besides stronger volumes, the growth was helped by a broader product range, notably the additive-free, vacuum-packed steamed sweet potatoes launched in FY2025 alongside the existing sweet potato crisps and fries.

See also: JP Morgan reiterates overweight for CLI as it ramps up listed and unlisted FUM

The processed chips and steamed sweet potato products remain the segment’s primary growth engines, with sales surging 71% y-o-y.

For the current FY2027, Lim and Chew expect this segment to grow by 30%, driven by improved production of high-margin premium products and an increase in the number of white-label customers for specific products such as sweet potato crisps.

On the other hand, the analysts point out that Zixin’s gross margin dipped by 330 basis points to 31.2% in 2HFY2026, mainly due to higher procurement costs from external farmers, as internal production was insufficient to meet demand despite a strong harvest season.

“In addition, purchases from external farmers are subject to taxes, and the larger procurement volume further intensified the impact of these costs, resulting in margin compression,” state Lim and Chew.

For FY2027, they expect Zixin to drive growth from continued strong demand for processed sweet potato products, driven by an increasing number of white-label customers in China and international markets.

The company is also shifting towards higher-margin offerings like sweet potato powder, supported by increased production at one of Zixin’s manufacturing facilities, which is operating now at 40% capacity, leaving room for further ramp-up

They expect Zixin to enjoy sustained demand for premium fresh sweet potato varieties such as Hong Yao and Black Gold, supported by high quality and competitive pricing.

For more stories about where money flows, click here for Capital Section

Further upside may come from incremental revenue contribution from trading activities on Hainan island and continued regional sales in Southeast Asia. In addition, the nascent animal feed segment, which generates revenue from selling sweet potato peeling and other waste materials, is set to see higher volume.

All in, the analysts have raised their FY2027 revenue estimates by 23% and net profit estimates by 29%, resulting in a higher target price of 6 cents, up from 5.5 cents previously. — The Edge Singapore

Sats

Price target:

CGS International ‘add’ $5.20

Extensive network

Tay Wee Kuang and Lim Siew Khee from CGS International have reiterated their “add” call on Sats (SGX:S58![]() ) following the brokerage house’s recent non-deal roadshow (NDR).

) following the brokerage house’s recent non-deal roadshow (NDR).

At the NDR, Sats’ management attributed the outperformance in cargo tonnage handled against global air cargo industry over the past 10 straight quarters to its strategic network that has a presence in 15 of the world’s top 30 air cargo stations and covers air trade routes that facilitate around 50% of the world’s air cargo volume.

“We believe its extensive cargo network also enabled Sats to capture the re-routing opportunities that have emerged as a result of supply chain disruptions arising from the Middle East crisis, which began at the end of February,” according to Tay and Lim.

At the same time, Sats’ management explains that growth in air cargo demand continues to be driven by the technology and e-commerce industries.

Meanwhile, Sats revealed that it is seeking opportunities to expand its air cargo operations into regions where it currently has limited or no presence, including Latin America, Africa and Central Asia. According to the company, expansion can take any form apart from M&As, such as joint ventures and operating contracts with air cargo station owners and operators.

“Sats’ key considerations for expansion of its cargo operations include retaining operational oversight to ensure delivery of its service levels, as well as whether the location serves a strategic purpose, such as entry into a key cargo hub to enhance its cargo network to better serve its existing customers,” the CGSI team explains.

Regarding its financial target, Sats’ management shared that it is on track to achieve its FY2029 financial targets of $8 billion in revenue, 20% ebitda margins, 10% ebit margin and 15% return on equity.

From Tay and Lim’s perspective, for Sats to achieve its FY2029 targets, it will need to augment its current organic growth trajectory with bolt-on acquisitions, which have not yet been factored into their estimates.

To better reflect profitability, they have lifted their FY2027 and FY2028 earnings per share (EPS) by 0.9% and 7.5%, respectively. However, they have also reduced FY2029’s EPS by 19.9% due to an underestimation of operating expenditure and the tax rate previously.

With that, their discounted cash flow-based target price for Sats is raised to $5.20, up from $4.68. Both analysts have assigned a lower weighted average cost of capital of 10.2% from 11.2% previously to reflect the lower risk premium associated with its resilient business model, given its more diversified geographical footprint today.

“We reiterate our “add” call as we see visibility for Sats to achieve a three-year net profit CAGR beyond 18%,” they add.

Re-rating catalysts include an uptick in food solutions profitability and entry into new key air cargo hubs, while downside risks mainly come from a deteriorating global economy resulting in a slowdown in e-commerce volumes and weakened consumer sentiment. — Teo Zheng Long

Beng Kuang Marine

Price target:

UOB Kay Hian ‘buy’ 75 cents

Contract wins underappreciated

In a June 17 report, analysts Tang Kai Jie and Heidi Mo of UOB Kay Hian (UOBKH) believe that the market has “underappreciated” the two recent contract wins totalling $28.6 million by Beng Kuang Marine’s (SGX:BEZ![]() ) subsidiary Asian Sealand Offshore and Marine (ASOM).

) subsidiary Asian Sealand Offshore and Marine (ASOM).

The contracts for the life extension of floating, production, storage, and offloading (FPSO) vessels were announced on June 4, bringing Beng Kuang’s pro forma order book to $92.5 million. Meanwhile, Beng Kuang’s shares have declined from a high of 60 cents on May 14 to 49 cents on June 16. As such, both analysts believe this represents an “attractive” entry point for the counter.

As part of the consolidation of ASOM into a wholly owned subsidiary of Beng Kuang by the end of the month, Tang and Mo expect earnings from the two contracts to be fully captured by Beng Kuang, with stronger revenue visibility for FY2026–FY2027.

They also believe that the successful execution of these initial tank service works could position ASOM favourably for subsequent phases of the FPSO life extension programmes, providing potential opportunities for additional contract awards over the coming years.

Tang and Mo add that the firm’s management expects additional contract awards this quarter. The company is currently undertaking five FPSO projects in Guyana and has potential for four more in Central America.

Reflecting management’s confidence, the company is increasing the FPSO headcount from 30 to about 120 between June and September so as to support the expected ramp-up in operations. Beng Kuang also plans to deploy a floatel by September to support its FPSO operations in Angola.

Another reason for UOBKH’s confidence is institutional investment in the company. Announced in May, Beng Kuang’s founder divested part of his stake to multiple investors, including Amova Asset Management and Tokio Marine Life Insurance Singapore.

At the same time, management increased its holdings, a move UOBKH views positively as it strengthens alignment between management and investors.

Moreover, Beng Kuang has been focused on paring its debt. With a net cash position of $26.9 million and minimal debt, the company’s balance sheet is likely to strengthen further as it shifts towards an asset-light operating model under its BKM 2.0 strategy, positioning it well to capitalise on opportunities amid strong industry tailwinds.

UOBKH maintains its “buy” rating at an unchanged target price of 75 cents, implying a 53.1% upside. This valuation is 14 times the 2027 forward P/E, which is 1.5 standard deviations above the historical average. As Beng Kuang is currently trading at around 9.2 times P/E, the counter is trading at a discount, according to UOBKH.

“Beng Kuang’s strong fundamentals, underpinned by a superior return on equity of 38.8% versus the industry average of 17.3% and a strong net cash position, continue to support the case for valuation re-rating,” states UOBKH. — Lin Daoyi

CSE Global

Price targets:

Maybank Securities ‘buy’ $2.25

RHB Bank Singapore ‘buy’ $1.94

Attractive opportunity to accumulate

Jacrick Seet of Maybank Securities has maintained his “buy” call on CSE Global (SGX:544![]() ) despite the recent weaker market sentiments and the resignation of its lead independent director, Tan Chian Khong. “We believe that the recent share price correction of more than 20% represents an attractive opportunity for investors to accumulate shares of CSE,” says Seet, who sees no impact on the company’s core fundamentals.

) despite the recent weaker market sentiments and the resignation of its lead independent director, Tan Chian Khong. “We believe that the recent share price correction of more than 20% represents an attractive opportunity for investors to accumulate shares of CSE,” says Seet, who sees no impact on the company’s core fundamentals.

“Meanwhile, CEO Lim Boon Kheng has increased his stake in the company from 3.7% to 3.71% by taking up the option of a scrip dividend, highlighting his confidence in the core potential of the company,” Seet states.

The Maybank analyst also thinks that Tan’s resignation may act as a check while also highlighting that management is the company’s key value driver.

The current 1HFY2026 might see some impact on margins as the company incurs higher costs while ramping up a new site. However, improvements should come later in the year. With the newly leased facility ready, production for its data-centre client is now in the midst of ramping up, and we expect q-o-q revenue improvement, especially from 2QFY2026 to 3QFY2026, says Seet, who is also expecting more orders from the company’s key data centre client if CSE could complete its orders at a much faster pace.

Overall, Seet remains bullish on CSE’s outlook and sees potential for a multi-year growth story. “The company expects to more than triple capacity by FY2027 and FY2028, and we expect it will secure another data centre client by 1QFY2027,” Seet predicts.

As such, CSE, as a proxy for the data centre boom in the US, remains a “buy”, with an unchanged target price of $2.25.

Meanwhile, with the independent Tan’s resignation, Alfie Yeo of RHB Bank Singapore, who has kept his “buy” call and $1.94 target price, expects CSE’s growth will “continue in the way that it has intended, steered by the chairman and the Board” and that the share price should stabilise, barring any

major developments to the strategic review.

“Otherwise, we see earnings growth being driven by the US$1.5 billion worth of Amazon orders that are anticipated over the next five years. We have projected a sturdy 27% earnings CAGR for FY2025 to FY2028,” Yeo says, noting that CSE, valued at below 1 time PEG ratio, is trading at around 20 times

forward P/E — below its FY2025–FY2028 earnings CAGR of 27%. — Teo Zheng Long

Info-Tech Systems

Price target:

RHB Bank Singapore ‘buy’ $1.40

Beneficiary of structural shifts towards AI

Syahril Hanafiah of RHB Bank Singapore has maintained his “buy” call and $1.40 target price on business software provider Info-Tech Systems, noting that the company is well-positioned to capture rising demand for artificial intelligence upskilling.

The industry Info-Tech is in enjoys strong structural tailwinds from government support for AI-driven workforce transformation. “We like this stock for its asset-light enterprise solutions with a growing user base in the SME market across various geographies,” says Hanafiah.

Citing United Nations estimates, Hanafiah says the global AI market is projected to reach US$4.8 trillion by 2033. At the same time, AI could affect 40% of jobs, with up to one-third of the positions in advanced economies at risk of automation.

“The same advanced economies, however, are better placed to benefit where 27% of jobs could be improved by AI, boosting productivity and complementing human skills; this will take time and effort for the full potential of AI to be realised,” he adds.

Hanafiah notes that Singapore has been proactive in keeping up with this frontier technology, including a commitment of over $1 billion from 2025 to 2030 to encourage AI research, real-world deployment and talent development.

The Singapore government has announced that those who register for and complete eligible AI courses will be entitled to a six-month free premium AI subscription. This initiative is expected to take effect in the second half of the year, but no details on course eligibility have been announced yet, he says.

The analyst calls this “structural shift” in policies an opportunity for Info-Tech Systems, particularly for its learning courses segment, operated via Info-Tech Academy, which now offers more than 15 courses, including six AI-related ones.

Course participants can tap SkillsFuture funding to subsidise course fees. “While eligible courses under SkillsFuture offer a wide range of skills and learning, we think the government is putting more emphasis on AI-related upskilling given the fast-evolving nature of this technology and how disruptive it can be to the labour market,” Hanafiah suggests.

According to company management, Info-Tech Systems is “actively expanding” its AI course offerings to meet growing market demand and support workforce upskilling initiatives.

“The focus would be on practical, industry-relevant AI courses across various business functions, and management is planning to add six or seven more courses on AI by the end of this year. With AI courses making up the majority of registrations year to date at the Academy, we believe Info-Tech Systems is well positioned to further capture this growing market amid supportive public policies,” Hanafiah says. For now, he is keeping his call and target price pending further developments. — The Edge Singapore

Food Empire Holdings

Price target:

UOB Kay Hian ‘buy’ $3.49

Steady returns, capacity expansion

John Cheong and Tang Kai Jie of UOB Kay Hian have maintained their bullish call on Food Empire Holdings, noting that the instant coffee maker has not only outperformed its peers’ growth but also has significant capacity expansion in the pipeline, poised for further growth.

“The next two years mark the most concentrated period of capacity additions in Food Empire’s history, with four facilities across four countries coming online sequentially,” state the analysts in their June 22 note, referring to Kazakhstan, Malaysia, India and Vietnam.

In the most recent 1QFY2026, the company delivered another record quarter, with broad-based revenue growth of 16.9% y-o-y to US$159.7 million.

Cheong and Tang observe that Asia surpassed the company’s traditional markets in Russia and Central Asia for the first time, accounting for 58% of its revenue, underscoring the payoff of its diversification strategy. Besides Vietnam, India is an increasingly important market, with its revenue share rising from 5.4% in 2021 to 12.3% in 2025, the analysts note.

Cheong and Tang point out that robusta coffee, a key ingredient, used to cost US$5,821 per tonne last February. It has since eased to US$3,670 per tonne — not as low as the 2022 levels that marked the recent surge, but still seen as helping Food Empire enjoy better margins nonetheless. “2025 captured some of this relief, and we expect further gradual margin expansion in 2026 as the commodity is sensitive to weather shocks,” they note.

Food Empire’s steady returns to shareholders have also been noted. Between 2021 and 2025, the company has returned a total of $228.5 million to shareholders, comprising $196 million in dividends and the remaining via share buybacks. The dividend trajectory from 2.2 cents in 2021 to a record of 12 cents in 2025 is a five-year CAGR of 53%, and 2025 marked the first-ever interim dividend.

In another positive development, the company has recently completed a one-for-five bonus issue, which Cheong and Tang interpret as a signal of management’s confidence in the sustainability of earnings and as designed to improve secondary-market liquidity. The bonus issue has increased the share base by 20% to 661.7 million shares.

The analysts continue to value the stock at 25 times FY2026 earnings, or 2.5 standard deviations above the long-term average, thereby deriving a target price of $3.49. Food Empire is now trading at just 17 times 2026 P/E, a 28% discount to the peer average of 24 times. — The Edge Singapore