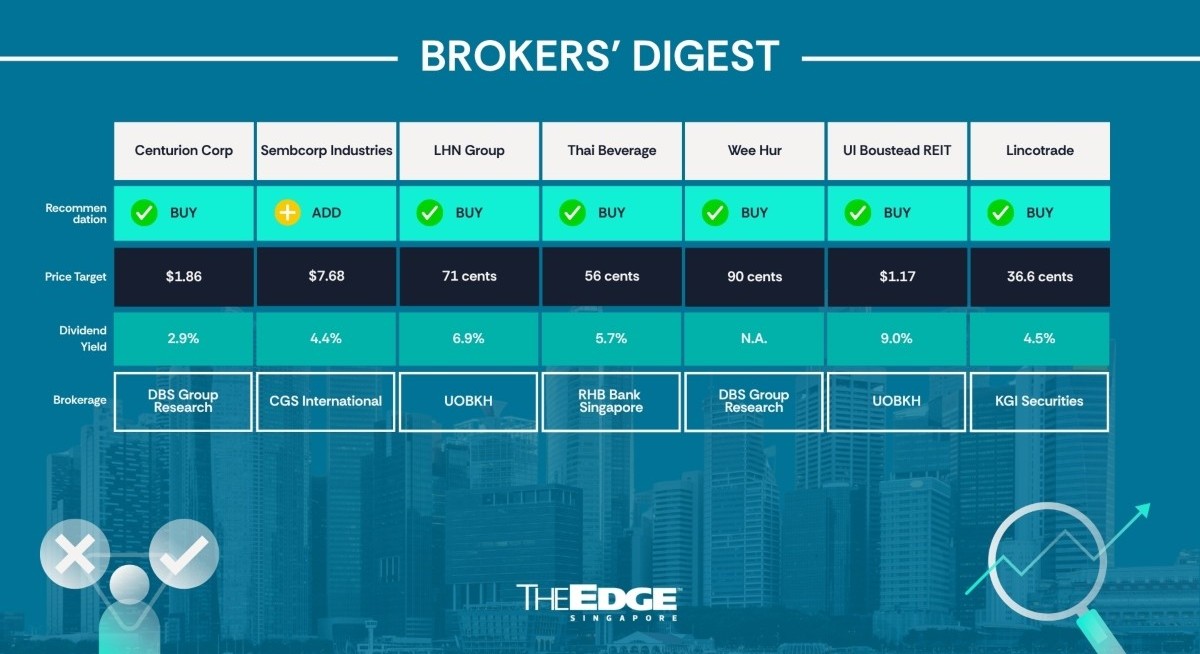

Bed growth drives earnings visibility

A group of DBS Group Research analysts, Derek Tan, Geraldine Wong, and Ng Jia Hui, has initiated coverage of Centurion Corporation (SGX:OU8![]() ) , citing growth in bed counts that will increase visibility for the diversified living-sector accommodation provider.

) , citing growth in bed counts that will increase visibility for the diversified living-sector accommodation provider.

As at end-March, Centurion owns and manages 40 operational assets comprising approximately 81,388 beds, with its Singapore PBWA portfolio operating under the established “Westlite” brand and its PBSA assets under the Dwell and Epiisod brands.

In addition, Centurion is also the sponsor of Centurion Accommodation REIT (CAREIT), which provides a pipeline of assets to support the REIT’s growth while advancing its asset-light strategy.

Three income streams

From the analysts’ perspective, following CAREIT’s listing, Centurion’s earnings framework has evolved into a diversified platform with three income streams.

These are: operating income from owned and operated assets, fee income from management services, and investment income from CAREIT units. The DBS analysts believe this will create a more capital-efficient, scalable and recurring-income business for Centurion.

See also: CGSI reiterates ‘add’ call with higher target price of $5.20 on SATS

“Centurion has been scaling its portfolio through acquisitions and developments across its core PBWA and PBSA segments in both existing and new markets, and into new living-sector segments, strengthening its growth runway while enhancing long-term income visibility and earnings resilience,” the team states.

On the other hand, as CAREIT’s sponsor, Centurion stands to earn fees ranging from REIT and property management to project management, which are expected to continue to grow in line with the REIT’s expanding portfolio.

Last October, Centurion secured a property management agreement (PMA) to manage an existing 548-bed dormitory on Jurong Island. This was followed by a second PMA in February to manage a 1,500-bed dormitory in the Gul Drive vicinity, to commence upon the property’s receipt of the relevant licence.

With Centurion holding approximately a 38.1% stake in CAREIT, the analysts foresee a steady stream of distributions for Centurion, supported by the REIT’s distribution policy of paying out 100% of its annual distributable income through FY2027.

Australian expansion

Meanwhile, Centurion has marked a key strategic expansion in April by entering the key worker accommodation (KWA) segment through the acquisition of two operational assets in Western Australia. This is a resource-rich region Down Under which accounts for roughly two-thirds of the country’s mining production and over 90% of its iron ore output.

The region supports more than 13,000 jobs and attracts a diverse mix of workers across mining and extraction, construction, engineering, oil and gas operations, and energy infrastructure.

For more stories about where money flows, click here for Capital Section

“Against this backdrop, the acquisition provides Centurion with exposure to structurally resilient, long-duration demand underpinned by large-scale resource projects and fly-in, fly-out workforce rotation cycles, which sustain recurring accommodation demand through continuous inbound and outbound labour flows,” the team predicts. As such, the DBS team is initiating a “buy” call and a target price of $1.86 on Centurion. Their valuation is based on a sum-of-the-parts approach.

“We value Centurion’s stake in CAREIT based on our target price of $1.30 and applying a 12 times EV/Ebitda multiple to the management services platform, reflecting its recurring, asset-light earnings. Owned and operated assets, excluding CAREIT assets, are valued at their fair values, while Australia KWA assets are valued at a 10 times EV/Ebitda on projected earnings,” the team explains.

According to the analysts, this will yield an SOTP valuation of $2.07, translating into a target price of $1.86 after applying a 10% holding-company discount. — Teo Zheng Long

Sembcorp Industries

Price target:

CGS International ‘add’ $7.68

Completion of Alinta acquisition

Lim Siew Khee and Meghana Kande of CGS International have kept their “add” call and $7.68 target price on Sembcorp Industries (SGX:U96![]() ) following the completion of its acquisition of Australia-based power company Alinta. The A$6.5 billion ($5.9 billion) deal was first announced last December. Under the terms of the deal, Sembcorp will book an A$208 million one-off acquisition-related expense in 1HFY2026.

) following the completion of its acquisition of Australia-based power company Alinta. The A$6.5 billion ($5.9 billion) deal was first announced last December. Under the terms of the deal, Sembcorp will book an A$208 million one-off acquisition-related expense in 1HFY2026.

With the completion of the deal, Sembcorp has announced a management share plan under which certain senior managers of Alinta will receive up to 3% of the equity in a new class of non-voting shares.

The analysts are expecting Alinta to contribute a core net profit of $115 million in FY2026, then increase to $230 million–$240 million on a post-financing-cost basis over the full year from FY2027 onwards.

According to Lim and Kande, over 60% of Alinta’s 3.4GW portfolio is located on the East Coast, in Victoria and Queensland.

Citing data from the Australian Energy Market Operator (AEMO), they note that average power prices in these two states during the March-June period, after the start of the US-Iran war, trended between –2% and +10% versus the pre-war January-February period. “The largely stable price trend is attributable to a higher share of renewables and battery storage,” state Lim and Kande.

Alinta aside, the CGSI analysts note that the average Uniform Singapore Energy Price (USEP) for June reached $218/MWh, up nearly 75% from the average of $125 over January-February. “We think elevated USEP and ongoing geopolitical uncertainties should drive higher spark spreads for Sembcorp’s Senoko portfolio that is pending recontracting in 2026.

Based on their ground checks, Lim and Kande note that spark spreads range from $50 to $70, depending on contract length.

Citing Sembcorp’s “defensive” gas earnings profile, backed by cost-through mechanisms and potential upside from gas portfolio optimisation in a tight market here in Singapore, the analysts have reiterated their “add” call and target price, which is based on 12 times FY2027 earnings, which is a discount to 16 times fetched by peers due to Sembcorp’s slower earnings growth.

“We think Sembcorp’s current valuation of 9.5 times FY2027 P/E is an attractive entry point for investors and keeps Sembcorp as one of our country’s top picks,” they add.

For them, key re-rating catalysts are announcements of new power purchase agreements (PPAs) and the unlocking of value in India’s renewable energy assets via IPOs or asset recycling.

On the other hand, downside risks include prolonged power plant shutdowns and unfavourable regulatory changes that could impact its operations. — The Edge Singapore

LHN Group

Price target:

UOB Kay Hian ‘buy’ 71 cents

Resilient occupancy rates

LHN’s (SGX:41O![]() ) 1HFY2026 earnings came in below expectations, but given the defensive, recurring nature of its income, UOB Kay Hian analysts Tang Kai Jie and Heidi Mo have maintained their “buy” call and 71 cents target price.

) 1HFY2026 earnings came in below expectations, but given the defensive, recurring nature of its income, UOB Kay Hian analysts Tang Kai Jie and Heidi Mo have maintained their “buy” call and 71 cents target price.

For the half year ended March, LHN reported revenue of $60.9 million and patmi of $16.8 million, which were just 44% and 38% of its forecasts.

The company is keeping its interim dividend at one cent. While LHN has no formal dividend policy, Tang and Mo expect the company to maintain a 40% payout ratio over the next two years, implying a yield of 5%–6%.

LHN attributes the decline to its property development and facility management businesses, but this is partially offset by higher revenue from residential properties and Coliwoo in the space optimisation business.

The company’s occupancy remains firm in 1HFY2026, supported by high occupancy across its space optimisation business.

As at end-1HFY2026, LHN’s co-living unit Coliwoo saw its occupancy edge up by 0.5 percentage points (ppt) q-o-q to 97%. Its industrial and Work+Store spaces were up 1.2 ppt q-o-q to 96.5%, and down 0.3 ppt q-o-q, respectively. Commercial space occupancy, meanwhile, was stable at 84.5%, down 1.5 ppt q-o-q.

“The resilient occupancy rates underscore the defensive, recurring nature of the group’s income base, supported by sustained tenant demand, which is expected to drive growth in the space optimisation business,” the analysts state.

The residential properties under Coliwoo saw revenue growth of 16% y-o-y to $27.4 million, with more to come as the company is in the midst of renovating 1,021 of its 3,568 rooms. “We expect to see a continued uplift to operating metrics as these rooms come on-stream,” state Tang and Mo.

The industrial & commercial properties were mixed. Industrial properties revenue fell 4% y-o-y to $12.4 million due to higher finance lease classifications, partly offset by a new property; commercial properties revenue was up 54% y-o-y to $2.3 million on fewer finance lease classifications.

Going forward, LHN expects to recognise more revenue from its property development in 2HFY2026. Also, LHN’s facilities management segment is seen to be resilient, with parking expansion and energy growth driving momentum.

Tang and Mo’s 71-cent target price is based on 10 times FY2027 earnings, which is 1 standard deviation above the mean. “We see limited near-term upside for LHN, as the group remains in a transitional phase following the Coliwoo spin-off and continues to reposition its business mix. We expected better earnings recovery and a stronger forward earnings profile in FY2027,” they add. — The Edge Singapore

Thai Beverage

Price target:

RHB Bank Singapore ‘buy’ 56 cents

Softer outlook

Alfie Yeo of RHB Singapore remains positive on Thailand’s broader economy and on Thai Beverage’s (SGX:Y92![]() ) earnings growth. However, after 1HFY2026 earnings were reported recently, Yeo has become more cautious, trimming his earnings forecast and target price.

) earnings growth. However, after 1HFY2026 earnings were reported recently, Yeo has become more cautious, trimming his earnings forecast and target price.

“We are positive on Thai Beverage for its strong market leadership position and longer-term prospects in Thailand and Vietnam, even though we are turning more cautious on our earnings forecast,” says Yeo, who has kept his “buy” call, but with a reduced target price of 56 cents from 62 cents previously.

From his perspective, Thai Beverage’s valuation remains “compelling” at just 10 times FY2026 earnings, which is below its historical mean of 15 times. This stock is also seen as offering an “attractive” yield of 6% for the current FY2026.

In the most recent 1HFY2026, Thai Beverage reported a slight y-o-y decline in both revenue and earnings. The various product segments posted mixed performance, suggesting uneven recovery in earnings growth. “Amid our positive stance over Thailand and Vietnam economies over the longer term, we look forward to firmer signs of performance improvement and recovery,” says Yeo.

With the slight decline in 1HFY2026 numbers, Yeo has trimmed his FY2026 earnings estimates by 4% accordingly. He is also projecting a slower growth rate for FY2027 and FY2028 and has cut his respective earnings projections by 10% and 11%, leading him to trim 9% off his previous target price. — The Edge Singapore

Wee Hur Holdings

Price target:

DBS Group Research ‘buy’ 90 cents

Strategically positive development

Ng Jia Hui of DBS Group Research has maintained her “buy” call and 90 cents target price on Wee Hur Holdings (SGX:E3B![]() ) after its plans to enter Hong Kong’s purpose-built student accommodation (PBSA) market through two investments.

) after its plans to enter Hong Kong’s purpose-built student accommodation (PBSA) market through two investments.

The first, Starvia by Y Suites on Fortress Hill, is a 246-bed PBSA asset held via a joint venture with Starvia Holdings and is expected to commence student leasing in 2H2026.

Building on this, Wee Hur acquired One Bedford Place, a 26-storey Grade-A commercial building in Tai Kok Tsui, Kowloon, for around HK$750 million ($95.6 million), which is deemed by Ng as a “deep-value purchase” given its 62% discount to its previously cited valuation of HK$1.98 billion.

Wee Hur plans to convert the asset into a PBSA development with around 500 beds, with operations targeted to commence in 1H2028.

“We view Wee Hur’s entry into Hong Kong’s PBSA market as a strategically positive development that expands the group’s exposure to one of Asia’s most compelling student accommodation markets, underpinned by strong policy-backed demand and a significant shortage of quality student housing,” says Ng.

“Hong Kong’s ambition to strengthen its position as an international education hub has driven a steady increase in non-local student enrolment, while PBSA has failed to keep pace,” she adds.

Citing data from real estate consultancy Colliers, Ng notes that the market now has a shortage of around 94,000 beds, with demand projected to rise to 172,200 beds by 2028, resulting in a widening supply gap of around 120,000 beds.

“This structural imbalance should support sustained occupancy and rental growth for well-located PBSA assets,” says Ng.

She especially likes how One Bedford Place was acquired at a deep discount to its previously cited valuation, providing a compelling margin of safety through its substantial embedded value and attractive entry price.

“The attractive pricing, alongside Wee Hur’s proven track record in Australia, serves as a strong testament to its turnaround execution and could catalyse further investment opportunities across Asia,” adds Ng. — The Edge Singapore

UI Boustead REIT

Price target:

UOB Kay Hian ‘buy’ $1.17

Growth in ‘high-value’ aerospace industry

Jonathan Koh of UOB Kay Hian has reiterated his bullish call on UI Boustead REIT (SGX:UIBU![]() ) for the second time in three weeks, citing the REIT’s distinct edge from its strong presence in the high-value, growing aerospace industry.

) for the second time in three weeks, citing the REIT’s distinct edge from its strong presence in the high-value, growing aerospace industry.

Last week, Bombardier announced it was spending $100 million to double its presence in Singapore. The Canadian company, which already operates within the Seletar Aerospace Park (SAP), is building a new facility on Seletar Aerospace Road, expected to be ready in the second half of 2028.

Boustead Singapore, which is backing UI Boustead REIT, lists the Bombardier Aerospace Singapore Service Centre (Phase 2) on its website as one of the development projects it is undertaking.

Just before Bombardier’s announcement, UIBREIT had announced on May 22 that was is developing a build-to-suit integrated aerospace facility for a leading global aerospace corporation at the SAP, with a net leasable area of 252,113 sq ft and a development value of $104 million. The REIT holds a 51% stake in the co-development, while Boustead Singapore owns the remaining 49%. The lease is on a triple-net basis for 22.5 years, with built-in rental escalations of 2-3%.

The development, which will be UIBREIT’s fourth property in SAP, provides a yield on cost of 8.6%, which is 120 basis points above UIBREIT’s projected FY2027 net property income yield of 7.4% for its Singapore portfolio, says Koh. With this new development, UIBREIT’s exposure to the high-value automotive, aerospace & avionics sector is expected to expand from 19.3% to 22.1% of rental income, he adds.

Upon completion, the development will increase UIBREIT’s SAP footprint to over 581,000 sq ft, strengthening its position within the government-supported aerospace ecosystem. For context, Singapore accounts for 10% of global maintenance, repair and operations (MRO) output and 20% of the world’s engine MRO output, says Koh.

Koh sees positive signals from other existing UIBREIT tenants. For one, engine maker Safran has announced a joint venture with SIA Engineering to set up a full-fledged CFM LEAP engine workshop here. Safran, according to Koh, could explore expanding its existing facility at 26 Changi North Rise, leased from UIBREIT, due to a step-up in its activity level.

“The contemplated asset enhancement initiative could increase the overall gross floor area from 65,000 sq ft to 117,000 sq ft, about 1.8 times the original size,” he estimates. Koh, citing an attractive DPU yield of 9% for FY2027 and 8.8% for FY2028, has maintained his “buy” call on this counter and set a target price of $1.17.

In contrast, CapitaLand Ascendas REIT’s yield is estimated at 5.9%, and AIMS APAC REIT’s at 6.3%. — The Edge Singapore

Lincotrade & Associates Holdings

Price target:

KGI Securities ‘outperform’ 36.6 cents

Revenue growth and margin resilience

Alyssa Tee of KGI Securities has initiated coverage on Lincotrade & Associates Holdings (SGX:BFT![]() ) with an “outperform” call and a target price of 36.6 cents, on the premise that the contractor, sitting on a record order book of $117.2 million — nearly triple that from $39.5 million in June 2024 — is well set for revenue visibility.

) with an “outperform” call and a target price of 36.6 cents, on the premise that the contractor, sitting on a record order book of $117.2 million — nearly triple that from $39.5 million in June 2024 — is well set for revenue visibility.

Of the existing order book, Tee, citing the company’s management, expects around 60% to be recognised in 2HFY2026 and 30% in FY2027. In addition, prospects are strong with a tender pipeline of around $200 million. Lincotrade, with its BCA L6 grading and growing commercial fit-out track record, has a historical win rate of 40%–50%.

Tee points out that Lincotrade is enjoying a favourable shift in the types of contracts it handles. She notes that commercial projects account for 89.6% of the order book; 1HFY2026 gross margin expanded by 2.8 percentage points to 15%, alongside 58.2% y-o-y revenue growth.

Data-centre projects, which account for around 23% of backlog, carry higher complexity and typically command better margins, adding a margin-accretive dimension to the commercial mix, says Tee. “We expect continued mix improvement to sustain gross margins within management’s 12-15% medium-term target, with upside should data-centre contribution grow,” she adds.

Meanwhile, Lincotrade is set for another earnings stream by making 100 beds available for rent at its Tuas factory. At an estimated rate of $450 per month, Tee figures this business will generate annual rental income of around $540,000. The factory has a carrying value of $13.1 million, but according to Lincotrade, the property has a bank valuation of $19 million.

Tee notes that Lincotrade’s 1HFY2026 earnings of $3.9 million have already exceeded $2.6 million chalked up for the whole of FY2025. She expects further improvements ahead, as fixed-cost absorption should drive additional operating leverage as revenue scales toward management’s $100 million target.

Shareholders are set to receive more dividends ahead as the company’s management has committed to a minimum 40% payout for FY2026, twice its formal 20% policy floor, with capex moderating after FY2026 to support sustained shareholder returns, says Tee, whose target price of 36.6 cents is derived using a discounted cash flow methodology.

“A record order book, ongoing mix shift towards higher-margin commercial and data centre-related projects, and a meaningful free cash flow inflexion from FY2027 as Tuas-related capex concludes and working capital normalises underpin our positive view,” says Tee. — The Edge Singapore