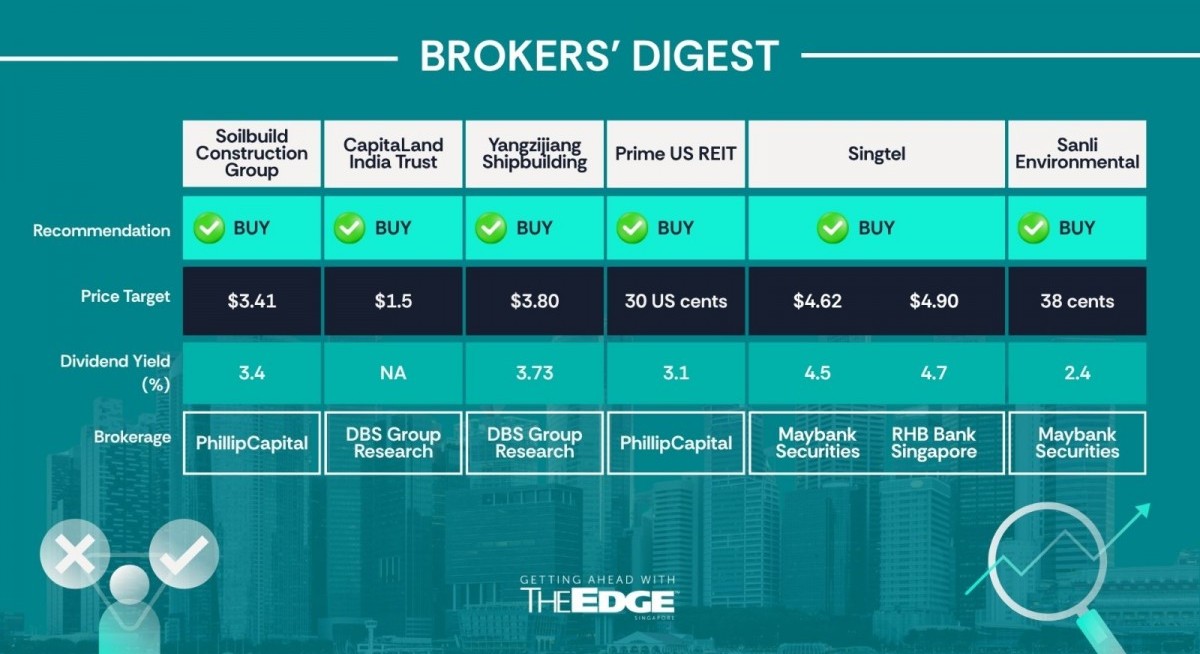

Yik Ban Chong of PhillipCapital has become more positive on Soilbuild Construction Group, as he has raised his valuation multiples for this stock to align it closer with its peers. In his September 29 note, Chong maintained his “buy” call and raised his target price to $3.41 from $2.68.

The construction sector is enjoying strong demand. Between this year and 2027, the government plans to launch 55,000 HDB flats, 22% higher than the historical three-year total of 45,000 flats. In addition, private sector contracts have also increased, with trailing 12-month volume up 62% y-o-y in July. “Based on its strong track record, we believe Soilbuild can secure additional contracts in the private sector in 4Q25,” says Chong.

Chong sees upside potential from the company’s precast segment. In the most recent 1HFY2025, revenue for this segment increased by 77% y-o-y and operating margins by 4.5 percentage points (ppt)y-o-y. He expects precast operating margins for the entire FY2025 to grow by 2 ppt y-o-y to 10.9%, as scale and efficiencies improve.

Chong has maintained his FY2025 revenue and earnings forecasts but increased his valuation multiple to 7.5 times FY2026 earnings, up from 5.9 times previously, to align more closely with the 8.4 times average of other construction firms. — The Edge Singapore

CapitaLand India Trust

Price target:

DBS Group Research ‘buy’ $1.50

Commencement of asset recycling

DBS Group Research has maintained its “buy” call on CapitaLand India Trust (CLINT) following its first divestments since listing. The REIT sold CyberVale in Chennai and Cyber Pearl in Hyderabad to an unrelated third party for INR11 billion, or approximately $161.7 million. The divestment price is at a 3% premium to the last valuation as of the end of 2024.

See also: Keppel DC REIT is JP Morgan’s preferred data centre play in Singapore

Net proceeds from this divestment, if assumed to repay debt, will strengthen the trust’s balance sheet and help lower gearing to 36.8% from 38.5%. The deal is expected to be distribution per unit (DPU) and net asset value (NAV) neutral, with both metrics remaining unchanged before and after the transaction.

From the perspective of DBS, the divestment signals CLINT’s renewed focus on portfolio reconstitution, by divesting legacy and older assets at or near optimal values and reinvesting the proceeds in higher-yielding or assets with a longer runway of growth, such as data centres.

DBS notes that following the divestment, CLINT will still retain sizeable platforms in Chennai and Hyderabad, anchored by international tech parks and upcoming data centres, thereby maintaining exposure to growth clusters while pruning smaller/non-core properties. “Our estimates are maintained for now, pending completion,” says DBS, whose target price is $1.50. — The Edge Singapore

Yangzijiang Shipbuilding

Price target:

DBS Group Research ‘buy’ $3.80

US$180 million order cancellation

DBS Group Research has maintained its “buy” rating and $3.80 target price on Yangzijiang Shipbuilding, following news that it has cancelled orders worth US$180 million ($232 million) placed by a customer facing US sanctions risk.

In a note dated Sept 29, DBS believes that there may be a potential knee-jerk reaction to the contract cancellation news, especially after a recent strong rally towards the high before the US port fees announcement. Nonetheless, the company’s earnings growth and order outlook remain intact, and Yangzijiang remains undervalued relative to regional peers, says DBS.

For more stories about where money flows, click here for Capital Section

The tankers, which were to be delivered between 2026 and 2027, were cancelled after belated disclosure of critical information alleging the buyer’s sole shareholder was involved in a scheme to circumvent US sanctions. This renders the buyer in anticipatory repudiatory breach of the contracts or frustrating them due to supervening illegality. The contract cancellations are not expected to have a material impact.

According to Yangzijiang in its statement on Sunday afternoon, construction had commenced on only one tanker, and no revenue or profit has been recognised. However, deposits totalling about US$22.48 million have been collected. “It remains to be seen the shipowner’s next course of action,” says DBS.

According to DBS, the best-case scenario would be for Yangzijiang to retain the deposits. A neutral outcome would be for the company to return deposits to the buyer and terminate the contracts amicably. The worst scenario is for this unnamed customer to file a lawsuit against Yangzijiang, claiming vessel price appreciation and/or loss of income due to contract termination. “We are leaning towards the best and neutral scenarios for now. It is a new customer with no other outstanding contracts with Yangzijiang,” says DBS.

This order cancellation aside, the company has won new orders totally US$1.9 billion for 44 ships year-to-date, including two new containerships ordered by Seaspan Corp, a long-time customer. DBS notes that the orders by Seaspan were placed after news on US port fees, which suggests resumption of confidence.

Over the past three months, Yangzijiang’s share price has increased by nearly 50%, yet it is still trading at an eight times P/E and a two times P/B. In contrast, regional peers are at 18 times P/E and three times P/B, even though Yangzijiang is generating a return on equity (ROE) of more than 25%, offers a dividend yield of 5%, and is on track for earnings growth of between 10% and 15%. DBS is reiterating its “buy” call and $3.80 target price, which is based on 2.5 times P/B, as it sees earnings growth with potential upside. — The Edge Singapore

Prime US REIT

Price target:

PhillipCapital 30 US cents

Placement, higher distribution

Following news that the company has raised US$25 million ($32.3 million) via a private placement and will also increase its distribution following operational improvements in the US office market, Darren Chan of PhillipCapital has maintained his “buy” call on Prime US REIT and increased his target price from 21 US cents to 30 US cents.

The placement was priced at 19.35 US cents, representing a 10% discount off the closing price on Sept 24. Proceeds will be used to fund capital expenditure, tenant incentives, leasing costs to attract and retain tenants, and to meet existing tenant obligations. At the same time, gearing will be held below 46% while strengthening the balance sheet. “We view the private placement positively,” writes Chan in his Sept 29 note.

“The capital raised is crucial for activating signed leases and supporting upcoming leasing commitments, paving the way for sustainable higher payouts. In addition to the additional capital, the REIT is seeing operational improvements,” he adds.

The REIT is in advanced talks to lease out 150,000 sqft of space, equivalent to 3.5% of its net lettable area (NLA), which will lift its portfolio occupancy to 85% by the end of the year, up from 80.2% in 1HFY2025.

Additionally, Chan anticipates a slight uplift in portfolio valuation at year-end, driven by the signing of new leases. At this level, Prime US REIT is still trading at 0.37 times its book value. With new leases signed, the REIT’s weighted average lease expiry has been extended to 4.7 years, up from 4.3 years in 1QFY2025.

In another positive indication, the REIT, with 10.5% of occupancy starting to commence its cash contribution from 3QFY2025 onwards, the REIT will have sufficient cash flow visibility to sustain the higher payout ratio going forward.

As such, Prime US REIT will raise its distribution from 10% in 1HFY2025 to at least 50% for the current 2HFY2025. It has been withholding distributable income to cover ongoing capital and operational needs.

Based on this new ratio, Chan has raised his FY2025 distribution per unit forecast from 0.26 US cents to 0.62 US cents. He has also lowered his cost of equity from 14.9% to 10.5%, given signs of recovery in the US office market and cash flow visibility from new leases signed in FY2024 and 1HFY2025. Overall, Chan has derived a higher target price of 30 US cents from 21 US cents. — The Edge Singapore

Singapore Telecommunications

Price targets:

Maybank Securities ‘buy’ $4.62

RHB Bank Singapore ‘buy’ $4.90

Selldown is a buying opportunity

Analysts are reiterating their “buy” calls on Singapore Telecommunications (Singtel) despite the recent Optus incidents.

Singtel’s Australian subsidiary Optus experienced two emergency outages on Sept 18 and Sept 28. The first was caused by human error and tragically led to three casualties. Both incidents were confined to emergency services and did not disrupt broader mobile and internet connectivity. They follow a cyberattack in 2022 and a nationwide outage in 2023 that already tested Optus’ resilience.

Noting that the incidents indicate heightened near-term financial risks, Maybank Securities’ analyst Hussaini Saifee lowers his target price to $4.62 from $4.75 previously. He flags the potential for customer churn and weaker pricing power, as well as higher operating and capital expenditures to boost redundancy and additional provisions.

“Although the full impact remains uncertain, a conservative scenario assumes a 5% decline in Optus mobile revenue for FY2027, no margin growth until FY2028, a two to three percentage point (ppt) increase in capex intensity, and A$200 million ($170 million) in provisions. Under these assumptions, Singtel Group’s FY2028 earnings and sum-of-the-parts (SOTP) valuation could decrease by 5%–6%,” writes Saifee in a Sept 30 note.

Meanwhile, RHB Bank Singapore struck a more upbeat tone, maintaining its target price of $4.90. It notes that Optus has invested more than A$9.3 billion in its network over the past five years, dismissing concerns about underinvestment.

“Optus’ transformation involves closing the pricing differential with Telstra and successive ebitda improvements, amongst others. It is too early to conclude whether the latest incidents will derail the positive momentum in postpaid prices seen over the recent quarters. The latest price-ups took effect in late July, and are yet to be reflected in Optus’ numbers,” writes RHB.

Regulatory penalties remain a risk. Optus was fined A$12 million for the 2023 outage and took provisions of A$142 million for the 2022 data breach. Guidance on new provisions is expected with first-half results.

Despite near-term headwinds, analysts point to structural support for Singtel’s stock. The group has launched a $2 billion buyback, offering a forecast dividend yield of approximately 5% in FY2026, and benefits from associates such as Bharti Airtel, Telkomsel and AIS. Expansion in data centres and AI services via its Nxera unit also underpins growth.

Singtel shares have fallen about 7% since the Sept 18 outage, compared with an 11% slump after the 2022 breach. “The selldown represents a good buying opportunity — in our view — with Singtel’s longer-term underlying thesis of return on invested capital (ROIC) improvement, capital management upsides, and ebit growth still intact,” writes RHB. — Nurdianah Md Nur

Sanli Environmental

Price target:

Maybank Securities ‘buy’ 38 cents

‘Well-positioned’ for FY2026 to FY2036 growth

Jarick Seet of Maybank Securities views the prospects of water and waste project developer Sanli Environmental as “even brighter” following a non-deal roadshow (NDR) held with the group’s management on Sept 4.

Presently, Sanli has a tender book valued between $600 million and $800 million. The group is actively bidding for several projects, including the $205 million Public Utilities Board (PUB) Changi NEWater Facility 3.

“We anticipate tender results worth $300 million to $500 million to be announced by the end of November. These potential wins could significantly increase Sanli’s orderbook from $333 million to a range of $600 million to $800 million,” writes Seet.

He believes Sanli has a “strong likelihood” of securing at least $200 million to $300 million of these orders, thus nearly doubling its current orderbook. He adds: “Such an outcome would serve as a significant catalyst for Sanli’s growth trajectory.”

Following the Covid-19 pandemic, elevated raw material and labour costs compressed the group’s margins in the FY2024 and FY2025. Seet anticipates a recovery in margins, particularly in the group’s Engineering, Procurement and Construction segment, as new contracts with improved margins commence in FY2026.

He writes: “Additionally, supported by a robust orderbook of $333 million as of July 10, we project revenue growth of 10% to 15% y-o-y for the next two years.”

Overall, Seet sees that the group is well-positioned for sustained growth from FY2026 to FY2036, driven by PUB water-related projects and the anticipated Long Island tenders.

Sanli is also “among the few” local companies with specialised polder expertise, as evidenced by its successful completion of its first polder project at Pulau Tekong. A polder is a tract of land that lies below sea level and is reclaimed from the ocean, lakes, rivers or wetlands through the building of dykes, drainage canals and pumping stations.

“This positions Sanli favourably to capitalise on the upcoming Long Island project, estimated at $100 billion, enhancing its growth prospects in the sector,” notes Seet. With this, he has kept his “buy” call and target price of 38 cents on the group. He adds that successfully securing a portion of these projects could “establish a multi-year growth trajectory” for Sanli.

Additionally, Sanli is also looking at new revenue streams, such as its magnesium hydroxide business and prequalification to provide water cooling and maintenance systems for a data centre in Johor, Malaysia. “We expect these initiatives to further diversify and strengthen Sanli’s revenue base,” writes the analyst. — Douglas Toh