Divestment of Crowne Plaza Changi Airport

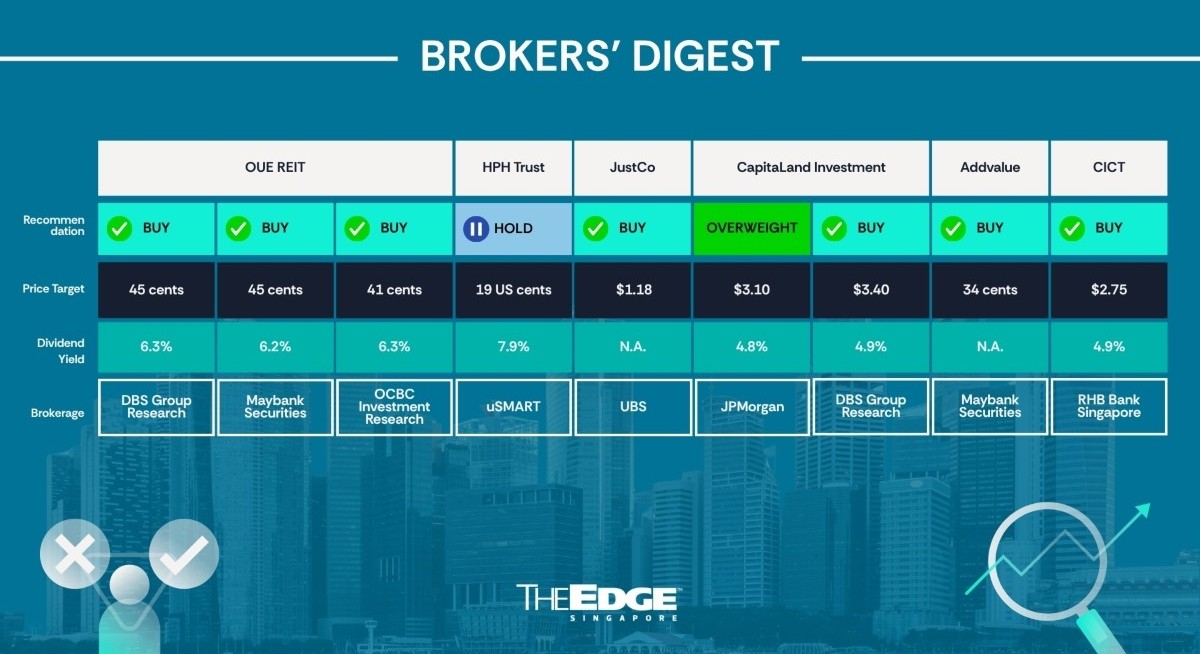

Analysts from DBS Group Research, Maybank Securities and OCBC Group Research remain positive on OUE REIT (SGX:TS0U![]() ) following the recent announcement on the proposed divestment of Crowne Plaza Changi Airport for $500 million.

) following the recent announcement on the proposed divestment of Crowne Plaza Changi Airport for $500 million.

Tabitha Foo of DBS Group Research views this divestment as a positive development for the REIT, given the upcoming hotel management agreement and the master lease expiry in 2028. “OUE REIT would likely face significant refurbishment capex, potential rebranding costs, operational downtime and the loss of minimum rent protection,” Foo says.

Foo believes this divestment is aligned with her value-unlocking thesis on OUE REIT. “If further value unlocking is seen, investors will likely be looking at further dividends to be rewarded for the rise in asset values,” Foo predicts.

See also: Citing defensive yield, Beansprout initiates coverage on United Hampshire US REIT

“Given that the exit price is close to book, this also signifies that OUE REIT’s net asset value (NAV) of 56 cents is realisable and can be achieved. If further divestments materialise, it implies that the current 40% discount is conservative,” Foo explains.

Following this divestment, Foo predicts that there will be questions about an eventual privatisation, given the smaller portfolio size if the sale of One Raffles Place, which is currently on the market, materialises.

Given that the pro forma distribution yield of 6.6% appears attractive for a largely Singapore-focused portfolio and the P/B ratio of 0.6 times, Foo is maintaining a “buy” call with a target price of 45 cents.

See also: Maybank lowers STI target to 5,500 points following market EPS downgrades

Meanwhile, Liu Miaomiao of Maybank Securities is keeping her “buy” call with an unchanged target price of 45 cents, given the upcoming special distribution of $20 million over the first two years following completion of the divestment and potential savings in finance expenses.

“On a pro forma basis, aggregate leverage is expected to decline from 41.5% to 36.6%, creating meaningful debt headroom to support further acquisitions, including an increased stake in Salesforce Tower,” Liu predicts.

Liu adds that while Crowne Plaza Changi Airport contributed 10% of OUE REIT’s FY2025 revenue and will result in a loss in income from FY2027 onwards, OUE REIT’s management has guided that distribution per unit (DPU) could increase by 5.8% after taking into account the special distribution.

“As such, we have incorporated the loss in income from FY2027 onwards while factoring in potential savings in finance expense alongside the special distribution,” Liu says.

Ada Lim of OCBC Group Research, meanwhile, has maintained her “buy” call with an unchanged fair value of 41 cents.

She sees divestment as part of the REIT’s capital recycling strategy to exit mature, lower-yielding assets and redeploy proceeds into higher-quality assets with better returns to close its NAV gap.

“This is a sizeable transaction, in our view — with Crowne Plaza Changi Airport contributing to around 10% of FY2025 revenue and 9.3% of portfolio value — and we are watchful of how the REIT eventually deploys the proceeds, as well as the timing and quality of any potential acquisitions,” Lim says.

For more stories about where money flows, click here for Capital Section

Lim notes that OUE REIT previously announced it is exploring the divestment of One Raffles Place and that this remains ongoing.

“As the buyer is a joint venture involving OUE, unitholders’ approval is required at an extraordinary general meeting (EGM) to be convened in 3QFY2026; thereafter, the transaction is expected to be completed in 4QFY2026. With that, we are leaving our forecast and fair value estimate unchanged in the interim,” Lim says. — Teo Zheng Long

Hutchison Port Holdings Trust

Price target:

uSmart Research Institute ‘hold’ 19 US cents

Operational resilience but ‘structural leakage’

Ng Xin Yang of uSmart Securities has downgraded his call for Hutchison Port Trust Holdings (HPH Trust) (SGX:NS8U![]() ) to “hold” from “buy”, along with a lower target price of 19 US cents (24.6 cents), down from 25 US cents, after forming a view that operational improvements and better cash flow generated by the terminals owned by the trust may not necessarily translate to better payout for unitholders.

) to “hold” from “buy”, along with a lower target price of 19 US cents (24.6 cents), down from 25 US cents, after forming a view that operational improvements and better cash flow generated by the terminals owned by the trust may not necessarily translate to better payout for unitholders.

From his perspective, the key investment issue for HPH Trust is therefore cash-flow pass-through.

According to Ng, writing in his June 24 note, HPH Trust’s FY2025 results reaffirmed that its terminals in mainland China have shown operational resilience. Revenue, operating profit, and profit attributable to unitholders all improved.

However, distribution per unit (DPU) was down from 12.2 HK cents (2.01 cents) paid in FY2024 to 11.5 HK cents in FY2025, as HPH Trust was required to set aside statutory reserves for its Yantian terminals under Chinese company law. Ng calls this move “the clearest example of structural leakage.”

Excluding this mandatory reserve impact, DPU would have been 14 HK cents, says Ng, citing the management.

Ng describes Yantian as HPH Trust’s key operating asset, supported by its strategic deepwater position in eastern Shenzhen and role within South China’s export gateway network. “Yantian can remain strong, but unitholder returns depend on how much cash survives interest, tax, non-controlling interest, reserve and debt-service layers,” warns Ng.

He points out that non-controlling interest remains the largest structural leakage item. In FY2025, profit attributable to non-controlling interests (NCI) was HK$1.71 billion, compared with HK$748 million attributable to HPH Trust unitholders, reflecting the trust’s partial ownership of key Chinese Mainland assets.

“This structure cuts both ways: NCI absorbs part of the earnings impact from higher consolidated interest cost, partially cushioning unitholders, but it also limits unitholder participation in operating upside,” says Ng.

As such, he has shifted his valuation anchor from asset-value re-rating to sustainable DPU. “Following FY2025, we place greater weight on forward DPU rather than EV/Ebitda or port transaction read-through. EV/Ebitda remains a peer cross-check, but dividend yield is the more relevant anchor for HPH Trust’s listed units,” says Ng.

Ng notes that at the June 22 close of 18.7 HK cents, HPH Trust’s FY2026 distribution yield of around 7.9% remains “supportive” for existing holders. “However, a new entry requires either a wider yield spread or clearer evidence that DPU has stabilised through the FY2026 refinancing and statutory reserve cycle,” says Ng.

For now, key re-rating watchpoints include the upcoming 1HFY2026 interim DPU, 2026 refinancing cost, statutory reserve treatment, NCI payout behaviour, revenue and container volume handled. Lower reserve or normalised non-controlling interest payout could reopen upside; a DPU cut or weaker Chinese Mainland revenue per TEU (20-foot equivalent unit) would further pressure risk-reward.— The Edge Singapore

JustCo Holdings

Price target:

UBS ‘buy’ $1.18

Limited investor familiarity

UBS, one of the underwriters of JustCo’s IPO, issued a report on June 24, initiating coverage on JustCo (SGX:JCO![]() ) with a buy rating and a 12-month price target of $1.18.

) with a buy rating and a 12-month price target of $1.18.

“The share price has fallen since listing and we think it reflects limited investor familiarity with the flex office model and execution concerns,” the UBS report says. That could be a bit of an understatement. JustCo’s IPO price was 94 cents and the stock touched an intra-day low of 49.5 cents on June 25 before closing at 52 cents. The stock ended the week of June 22–26 at 54 cents.

UBS uses an enterprise value to cash ebitda multiple valuation method in valuing businesses similar to JustCo, and is pegged at nine times 2027 EV/Cash ebitda.

“We use JustCo’s 2027 cash ebitda of US$32 million estimate and adopt an EV-to-cash-ebitda framework rather than the conventional Singapore real estate metrics such as price-to-earnings, price-to-book, or dividend yield. This distinction is because JustCo has a different capital structure. The company operates without external debt and generates a high rate of internal cash flows,” UBS explains.

According to UBS, JustCo plans to open 28 centres in 2026, and Japan is a high-margin market to monitor, as slower expansion could weigh on cash ebitda. “The market capitalisation and free float are also small, which heightens liquidity risk. We are constructive and view the extent of the sell-off as difficult to reconcile with valuations at 1.8 times EV/Cash ebitda and 0.4 times price-to-cash-ebitda growth, which is attractive versus peers. The listed workspace peer set is relatively narrow, leaving a wide 4–13 times EV/Cash ebitda trading range and limiting the value of a single point multiple. Our price target is based on a nine times multiple, the midpoint of the range,” the UBS report says.

CBRE data indicate that flexible office penetration rates in Asia Pacific (Apac) stood at 5.4% as of 1H2025, well below the 10.6% rate seen in more developed markets such as Central London. “Against this backdrop, JustCo’s Apac expansion plan underpins our expectation of a +43.5% CAGR in underlying cash ebitda over 2025–2028,” UBS adds. — The Edge Singapore

CapitaLand Investment

Price targets:

JPMorgan ‘overweight’ $3.10

DBS Group Research ‘buy’ $3.40

China REIT

For CapitaLand Investment (CLI) (SGX:9CI![]() ) , which will soon mark its fifth anniversary as a listed entity in its current form, China remains very much a centre of activity, given how it was and still is its largest single overseas geography, with Chinese assets accounting for 24% of CLI’s funds under management (FUM) as at Dec 31, 2025 compared to around 30% in 2021.

) , which will soon mark its fifth anniversary as a listed entity in its current form, China remains very much a centre of activity, given how it was and still is its largest single overseas geography, with Chinese assets accounting for 24% of CLI’s funds under management (FUM) as at Dec 31, 2025 compared to around 30% in 2021.

Since 2021, China’s property sector has been in the doldrums, resulting in large writedowns for CLI. As at FY2025, CLI was nursing a $428 million ebitda loss and a $545 million revaluation loss from China. To address overseas investors’ disinterest in China, CLI introduced a China-for-China strategy. That led to the successful listing of its C-REIT, CapitaLand Commercial C-REIT.

On June 22, CLI announced plans to list a second C-REIT comprising Raffles City Shenzhen and CapitaMall Fucheng in Mianyang (a provincial town in Sichuan province). This upcoming C-REIT could boost the FUM of listed funds by $900 million.

“The approval of CLI’s second C-REIT accelerates the growth of its flourishing listed REIT platform and asset recycling initiatives,” a JP Morgan report, dated June 24, says. “We also believe the large on-balance sheet writedowns that have weighed on the stock are largely behind us, supported by the absence of significant disposal losses and management guidance.”

Despite the challenges in China, CLI has made significant progress since its business was split into CLI and CapitaLand Development. As indicated by JPMorgan, over the past five years, listed FUM has risen 36% to an estimated $79 billion. And, the CLI REITs on the Singapore Exchange are outperforming the S-REIT index. Organic growth drivers position the platform well for continued FUM growth, says JPMorgan, which has an “overweight” call and a $3.10 target price.

The private funds business had a slower start. Still, recent large mandate wins demonstrate growing traction, including $2.4 billion from NTUC Income, the $403 million Asia Pacific Credit Program II (ACP II) and a potential $0.6 billion China private REIT. This follows the establishment of lodging, storage, and credit funds, supplemented by the acquisition of Wingate and SC Capital. “We estimate that private fund FUM has risen 82% over five years to $51 billion,” JP Morgan calculates.

DBS Group Research is also positive on CLI following the approval of its second C-REIT listing in China. “While impact is likely immaterial, it has strategic importance in our opinion as this transaction represents another meaningful step in CLI’s asset-light strategy, providing an avenue to recycle capital from stabilised assets while growing recurring fee income,” DBS observes in a report dated June 25.

“We view the approval positively as it reinforces CLI’s leadership in China’s public REIT market and demonstrates continued regulatory support for commercial real estate securitisation,” says DBS, keeping its “buy” call and $3.40 target price. “Beyond unlocking capital from mature assets, the successful launch broadens CLI’s capital recycling runway and provides additional dry powder for redeployment into higher-growth opportunities.” — The Edge Singapore

Addvalue Technologies

Price target:

Maybank Securities ‘buy’ 34 cents

Accumulation opportunity

Jarick Seet of Maybank Securities has maintained his “buy” call and 34-cent target price on Addvalue Technologies (SGX:A31![]() ) , which is riding on the big new growth theme of space and communications.

) , which is riding on the big new growth theme of space and communications.

He notes that Addvalue’s share price has seen some pullback after SpaceX’s mega listing in the US. Even so, Seet believes this is an “attractive opportunity” for investors to accumulate the stock.

“The successful SpaceX listing helps build the case for high space-sector valuations in the US, which should be positive for Addvalue if it lists its Inter-satellite Data Relay Service (IDRS) business on Nasdaq,” says Seet.

He estimates that Addvalue can fetch a potential market cap for its IDRS unit in the US$180 million ($233 million) to US$250 million range with a successful Nasdaq listing. There is even the potential to return some cash to shareholders.

“This would put Addvalue at the forefront of Singapore’s space/satellite scene and could lead to M&A opportunities. The Singapore valuation could rise if the value of its Nasdaq-listed arm exceeds that of Addvalue’s Singapore market cap. Advanced Digital Radio System (ADRS) orders likely to surge in coming months,” he adds.

As a quick recap, Addvalue’s IDRS division has secured orders of US$15.2 million year to date, compared to only US$4.2 million in 1H2025 and US$3.8 million in 1H2024.

“We believe IDRS orders will continue to surge from increased demand from existing and new customers,” says Seet.

Out of US$5.1 million in orders clinched, one new customer has been secured for multiple IDRS terminals to support upcoming earth observation and in-orbit services.

“With anti-drone solutions now actively demanded by governments globally, including locally, we expect ADRS orders to surge in 2H2026 with larger-sized multi-year orders while IDRS orders likely continue to be secured,” reasons the analyst.

Seet says that besides AI, Addvalue is benefiting from two of the most exciting and highest-growth themes in the investment world: drones and space.

“We expect a rapid growth phase in the next few years after Addvalue’s turnaround in FY2025. It thus ranks as one of our Top Picks in the small-cap tech space.” — The Edge Singapore

CapitaLand Integrated Commercial Trust

Price target:

RHB Bank Singapore ‘buy’ $2.75

Upside potential with Paragon acquisition

Vijay Natarajan of RHB Bank Singapore has kept his “buy” call on CapitaLand Integrated Commercial Trust (CICT) (SGX:C38U![]() ) , given how valuation is deemed “attractive” at just one times P/B, along with a slightly raised target price of $2.75, up from $2.73, after unitholders gave their go-ahead for the $3.9 billion acquisition of Paragon.

) , given how valuation is deemed “attractive” at just one times P/B, along with a slightly raised target price of $2.75, up from $2.73, after unitholders gave their go-ahead for the $3.9 billion acquisition of Paragon.

“The transaction further strengthens CICT’s position as the largest Singapore commercial sector proxy and leading Asia Pacific REIT,” says Natarajan.

As a recap, CICT will acquire the entire Paragon — both retail and office components — at an initial yield of 3.9%.

Upside potential includes rent growth and repositioning potential for retail and medical spaces while CICT is likely to undertake phased asset enhancements, he says.

The transaction will be partly funded by the sale of Asia Square Tower 2 for $2.45 billion, a 10% premium to valuation and an exit yield of around 3%.

Given strong investor demand, CICT has upsized its equity fundraising from $600 million to $750 million, which should keep gearing at 38.7%. The transaction is 1.7% distribution-per-unit (DPU)-accretive on a pro forma FY2025 basis.

Natarajan notes that CICT has trended sideways amid macroeconomic uncertainty, but April retail sales data show positive momentum, with a 5.4% y-o-y increase and inflation remaining benign.

Natarajan believes that tenant sales at CICT’s malls are likely to see a similar uplift, supporting mid-single-digit rental reversion growth in FY2026.

Meanwhile, the office vacancy rate in Singapore CBD was a record low of 3.3% in 1Q2026, down from 4.5% in 4Q25, with around 1% q-o-q rent growth. “We expect rental reversion for its Singapore office portfolio to remain in the mid- to high-single-digit range,” says Natarajan.

According to the analyst, CICT is looking at divesting its assets in Germany, which account for around 3% of its AUM. While market activity remains “weak”, Natarajan believes that Gallileo — its 38-storey Grade A commercial building valued at $520 million — could attract interest from real estate funds, given that CICT had recently entered into a long lease with the European Central Bank.

Meanwhile, CICT is spending some $160 million to enhance Plaza Singapura between 3Q2026 and 4Q2028, with a targeted return on investment of 6%–7%.

Natarajan derives his new target price after raising his DPU estimates for FY2027 and FY2028 by 1% to reflect the Paragon acquisition and the divestment of Asia Square Tower 2 and Bukit Panjang Plaza. — The Edge Singapore