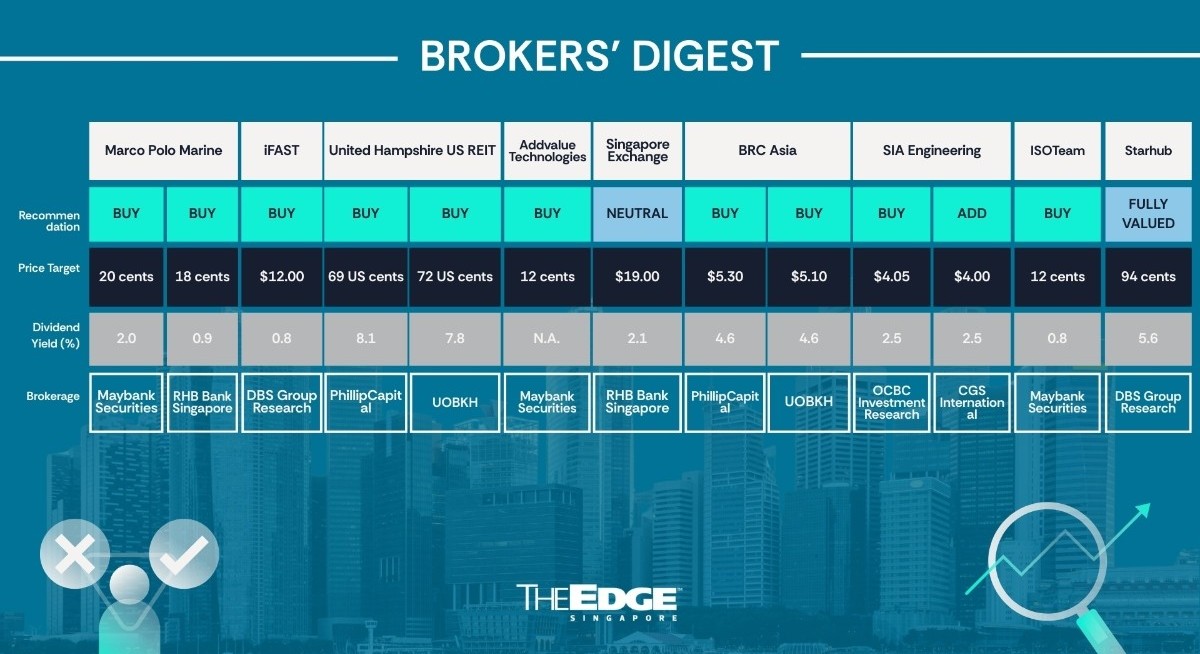

Maybank Securities and RHB Bank Singapore remain confident in Marco Polo Marine (SGX:5LY![]() ) (MPM) after it reported revenue of $32.8 million, 27% higher y-o-y, for the 1QFY2026 ended Dec 31, 2025.

) (MPM) after it reported revenue of $32.8 million, 27% higher y-o-y, for the 1QFY2026 ended Dec 31, 2025.

Believing MPM is entering a “rapid” growth phase from FY2026 to FY2030, Maybank analyst Jarick Seet is maintaining his “buy” rating at an unchanged target price of 20 cents, representing a 32% upside to the counter’s Feb 16 closing share price of 15.1 cents.

In his Feb 19 report, Seet anticipates MPM to perform even better in the second and third quarters of FY2026. Despite increasing its fleet size, he notes that utilisation improved y-o-y from 71% to 76% in 1QFY2026, leading to revenue growth and a stronger y-o-y gross profit margin of 14% from 10.6%.

In addition, Seet also expects fleet utilisation will be even higher q-o-q through 3Q before easing in 4Q before rising again in 1Q. Looking ahead, he expects MPM’s next-gen commissioning service operation vessel, or CSOV Plus, to boost profitability around FY2028/2029.

See also: UOB Kay Hian maintains 'buy' call on Food Empire with $3.49 target price

Another reason for Seet’s optimism is Michael Kum’s investment in MPM. In January 2026, Kum, through Halom Investments, bought 150 million shares in MPM at 13 cents each. Seet believes that Kum has a “strong” track record of identifying and investing in growing marine industry companies. He also thinks that MPM’s direction and growth could potentially benefit from Kum’s connections and experience.

Maybank projects MPM’s earnings per share to grow significantly from FY2027 to FY2030 on the back of fleet expansion and potential newbuild contracts as it expands its shipyard capabilities and capacity with a fourth new dry dock, which became operational in August 2025.

Meanwhile, in his Feb 23 report, RHB analyst Alfie Yeo maintains MPM at “buy” with a target price of 18 cents per share, an increase of 0.3 cents from his Jan 19 report. With revenue and gross profit remaining “on track” to meet estimates, Yeo views MPM as a “steady” company, with growth supported by increasing fleet size, new fourth dry dock at MPM’s shipyard and a “strong” orderbook.

See also: Goldman Sachs says Chinese cross-border curbs, effective July 1, had limited impact “so far”

Segmentally, Yeo notes that the deployment of the new CSOV and three crew transfer vessels not only increased fleet size and capacity, but also led to a “more favourable” sales mix. With the new vessels earning better rates and utilisation rising, gross profit for the segment rose y-o-y from 41.1% to 42.7%.

For shipbuilding and repair, Yeo points out that the segment recorded a y-o-y revenue decline of 9% to $10 million, mainly due to fewer shipbuilding activities, but offset by more ship repair projects.

In the immediate future, Yeo expects FY2026 growth to be driven by a combination of its newly deployed vessels and enhanced shipyard capacity, enabling MPM to take on more ship repair projects. The analyst remains “buoyant” on MPM’s outlook as revenue will be progressively recognised from its $198 million advanced oceanographic research vessel ship building order for Taiwan’s National Academy of Marine Research. Margin-wise, Yeo sees sustained demand at “attractive” rates — supporting “firm” gross margins — for MPM’s four newly deployed vessels.

Over the longer term, Yeo points out that MPM is on track to submit its listing application for its 49% indirectly-owned subsidiary, PKR Offshore, to the Taiwan Stock Exchange by September 2026. The listing will enable MPM to raise funds for vessel development, including CSOVs, to better serve high-growth offshore wind markets.

Yeo believes that MPM’s Feb 19 closing price of 16 cents represents a “compelling” P/E to growth ratio of less than one. Its discounted cash flow-based valuation target price of 18 cents reflects a forward P/E of 15 times for FY2026. — Lin Daoyi

iFast Corp

Price target:

DBS Group Research ‘buy’ $12

Strong 4QFY2025 earnings

For more stories about where money flows, click here for Capital Section

Ling Lee Keng of DBS Group Research has raised her target price for iFast Corp (SGX:AIY![]() ) from $10.23 to $12 after it announced higher revenue and earnings in FY2025 ended Dec 31, 2025, on Feb 12. After iFast’s record-strong performance for 4QFY2025, where net profit rose 8% y-o-y to $32.9 million, Ling expects the momentum will continue with 2026 a “strong” year for the company. With record revenue and growth in assets under administration (AUA) in the quarter, Lim is sanguine that AUA will continue to grow, driven by “healthy” net inflows and “progressive monetisation” of pension mandates.

) from $10.23 to $12 after it announced higher revenue and earnings in FY2025 ended Dec 31, 2025, on Feb 12. After iFast’s record-strong performance for 4QFY2025, where net profit rose 8% y-o-y to $32.9 million, Ling expects the momentum will continue with 2026 a “strong” year for the company. With record revenue and growth in assets under administration (AUA) in the quarter, Lim is sanguine that AUA will continue to grow, driven by “healthy” net inflows and “progressive monetisation” of pension mandates.

For the quarter, iFast reported revenue growth of 45.7% y-o-y to $151.7 million, bringing full-year revenue to $514.6 million, which represented a 34.4% increase from FY2024. Full-year net profit rose 50.1% to $100 million, driven by higher AUA, stronger growth in the Hong Kong ePension business, resilient growth in the core wealth management platform, and iFast Global Bank achieving its first full year of profitability.

Net inflows totalled $4.72 billion and AUA reached $31.98 billion, a 27.9% increase from the previous year. Geographically, AUA grew 27.8% y-o-y for Singapore, while Hong Kong, Malaysia and China saw growth of 20.7%, 19.6% and 74.9% respectively.

Ling believes Hong Kong and Macau to be part of iFast’s growth story in 2026. For Hong Kong, growth will be driven by the maturing ePension platform, “expanding” client assets and a new revenue stream when the Occupational Retirement Schemes pension administration business commences contribution in 2H2026.

Ling sees the Macau ePension as a catalyst for accelerating the adoption of iFast solutions. She adds that upside drivers include sustained inflows across key markets, expansion of payment services and deeper fintech ecosystem integration, which will reinforce earnings visibility. — Lin Daoyi

United Hampshire US REIT

Price targets:

PhillipCapital ‘buy’ 69 US cents

UOB Kay Hian ‘buy’ 72 US cents

Strong income visibility

In his Feb 23 report, Darren Chan of PhillipCapital highlighted that United Hampshire US REIT’s (SGX:ODBU![]() ) (UHREIT) 2HFY2025 and FY2025 distribution per unit (DPU) of 2.30 US cents (2.9 cents) and 4.39 US cents, which were up 12.2% and 8.1% y-o-y, respectively, formed 54% and 103% of his FY2025 forecast.

) (UHREIT) 2HFY2025 and FY2025 distribution per unit (DPU) of 2.30 US cents (2.9 cents) and 4.39 US cents, which were up 12.2% and 8.1% y-o-y, respectively, formed 54% and 103% of his FY2025 forecast.

“Growth was driven by new lease commencements, contributions from Dover Marketplace, acquired in August 2025, rental escalations on existing leases and lower finance costs,” states Chan.

While UHREIT’s occupancy for grocery & necessity properties remained high at 97.7%, its self-storage properties saw occupancy decline to 88.7% due to seasonality and tenant turnover.

“The portfolio’s stability is underpinned by strong grocery & necessity occupancy rate, a long weighted average lease expiry (WALE) of 7.7 years, a 90% tenant retention rate, and minimal leasing risk in FY2026, with only 2.9% of grocery & necessity leases expiring,” explains Chan.

Chan sees the above as key contributing factors to strong income visibility and supports UHREIT’s long-term growth. As such, he is keeping a “buy” call on UHREIT with an unchanged target price of 69 US cents based on the dividend discount model (DDM), while keeping his estimates unchanged. “UHREIT currently trades at an attractive FY2026 dividend yield of 8.4% and P/NAV of 0.76 times,” he says.

At the same time, Jonathan Koh of UOB Kay Hian sees UHREIT “pulling multiple levers”, such as asset recycling, accretive acquisitions and asset enhancement initiatives (AEI) to drive sustainable growth.

In his Feb 23 report, he sees UHREIT could benefit from full-year contributions from the acquisitions of Dover Marketplace and Wallingford Fair in FY2026.

“It could consider recycling assets by divesting self-storage properties, which have a yield of around 5% and reinvesting in strip centres that could yield between 6% and 7%,” adds Koh.

On the AEI front, UHREIT is developing a new 5,000 sq ft store on excess land and is pre-leased to Florida Blue, a health insurance company, under a 10-year lease agreement. The property, which opened in Nov 2023 and has already contributed positively, he says.

The analyst adds that the new store is expected to generate rental income upon completion in 4QFY2026, and UHREIT’s management has estimated capex at US$2 million and a 10% return on investment.

Also, UHREIT trades at a FY2026 distribution yield of 8.8%, which represents an attractive yield spread of 4.7% above the 10-year US government bond yield of 4.1%. It trades at a P/NAV of 0.77 times,” states Koh.

As such, Koh is maintaining his “buy” call on UHREIT with a target of 72 US cents, based on the DDM with a cost of equity of 8.5% and terminal growth of 1.5%. — Teo Zheng Long

Addvalue Technologies

Price target:

Maybank Securities ‘buy’ 12 cents

Rare, profitable, high-margin growth stock

Maybank Securities’ Jarick Seet has initiated coverage on Addvalue Technologies (SGX:A31![]() ) with a “buy” call and a target price of 12 cents. Seet’s target price represents an upside of 45% and is based on a blended FY2027/FY2028 P/E of 35 times.

) with a “buy” call and a target price of 12 cents. Seet’s target price represents an upside of 45% and is based on a blended FY2027/FY2028 P/E of 35 times.

“Addvalue Technologies is one of the rare profitable, high-margin, growth stocks in both the space and drone industries and a turnaround story,” says Seet in his Feb 19 report.

He also notes several tailwinds for the company, including an expected increase in satellite launches in FY2026 to FY2030, a higher customer base, from four to five clients eight years ago to over 20 clients as of 2025, a surge in the pace and size of orders, as well as rising demand and investment in the space sector, including for drone solutions.

Addvalue, which returned to profitability in the FY2025 ended March 31, 2025, was also removed from the Singapore Exchange’s (SGX) watch-list in October 2025.

The company had been on the exchange’s financial watch-list since December 2023 and said it would have fulfilled the criteria of existing on the watch-list by its own merits by the end of the six-month review period on Dec 1, 2025.

“After almost going under, Addvalue is benefiting from the two highest growth and sexiest themes besides AI (artificial intelligence) — drones and space,” says Seet. “We expect to see a rapid growth phase in the coming years following an inflexion point in FY2025,” he adds.

The company is deemed by the analyst as a “rare Asian space/drone play in rapid growth mode”. In addition, its peers’ valuations are “much higher” with most of them not yet profitable, he points out.

From FY2026 to FY2028, Seet expects Addvalue to report revenues of US$20 million ($25.3 million), US$30 million and US$45 million, respectively.

Core net profit for the three years is expected to be at US$4 million, US$8 million and US$13 million, respectively. The figures are supported by the company’s record order book of US$26 million. To Seet, risks include delays in satellite launches by its customers, client concentration risk and execution risk in overseas markets. — Felicia Tan

Singapore Exchange

Price target:

RHB Bank Singapore ‘neutral’ $19

EDQP boost

Shekhar Jaiswal of RHB Bank Singapore has kept his “neutral” call on Singapore Exchange Group (SGX:S68![]() ) , but raised his target price to $19 from $18.50, reflecting higher 1HFY2026 trading and clearing fees, thereby raising his FY2026 to FY2028 earnings estimates by 0.9% to 3.3%.

) , but raised his target price to $19 from $18.50, reflecting higher 1HFY2026 trading and clearing fees, thereby raising his FY2026 to FY2028 earnings estimates by 0.9% to 3.3%.

“Policy tailwinds are improving the medium-term outlook, which should support liquidity, issuance, and turnover,” states Jaiswal in his Feb 16 note.

On Feb 12, the government announced another $1.5 billion to the Equity Market Development Programme (EQDP), bringing the total boost to the local market to $6.5 billion. “This should further help fund managers build deeper Singapore equity exposure, bring in third-party inflows, and improve market liquidity,” says Jaiswal.

In addition, on Feb 14, deputy chairman Chee Hong Tat of the Monetary Authority of Singapore (MAS) announced the formation of the Growth Capital Workgroup, tasked with strengthening Singapore as a growth-capital hub, covering measures across deal origination, fundraising, capital mobilisation and capital recycling.

The workgroup will complete its review by the end of next year and provide interim updates on its recommendations along the way. “These initiatives should support both primary issuance and secondary trading for SGX,” he adds.

Jaiswal is now assuming the exchange’s securities daily average value (SDAV) to sustain an uptrend from $1.3 billion in FY2025 to $1.84 billion by FY2028.

In addition, he believes that SGX will pay a total dividend of 59.8 cents by FY2028, above the 52.5 cents the exchange is guiding to. “Despite our more constructive dividend outlook, the yield remains modest,” says Jaiswal, noting SGX’s share price appreciation.

Jaiswal says he likes the stock, but he figures the market has already priced in the near-term uplift in trading volumes. He is keeping his FY2027 target multiple at 26 times P/E, which is two standard deviations above this counter’s 10-year average forward PE and broadly in line with regional peers, except India. “We still like owning SGX for its constructive medium-term setup, but valuation caps near-term upside,” he says. — The Edge Singapore

BRC Asia

Price targets:

PhillipCapital ‘buy’ $5.30

UOB Kay Hian ‘buy’ $5.10

Better-than-expected 1QFY2026 earnings

BRC Asia’s (SGX:BEC![]() ) better-than-expected 1QFY2026 results ended Dec 31, 2025, have prompted analysts to raise their already bullish target prices further. In addition, the steel supplier’s order book maintained strong momentum, rising 16% q-o-q and 47% y-o-y to $2.2 billion, driven by orders from major projects such as the airport’s Terminal 5.

) better-than-expected 1QFY2026 results ended Dec 31, 2025, have prompted analysts to raise their already bullish target prices further. In addition, the steel supplier’s order book maintained strong momentum, rising 16% q-o-q and 47% y-o-y to $2.2 billion, driven by orders from major projects such as the airport’s Terminal 5.

In 1QFY2026, patmi jumped 40% y-o-y to $27.3 million, with delivery volumes up 42% y-o-y.

The company is estimated to command a 55-60% share of Singapore’s steel market, positioning it to benefit from rising construction activity.

In his Feb 16 note, PhillipCapital’s Yik Ban Chong suggests that BRC Asia can secure further contract wins in the coming quarters, including Marina Bay Sands Integrated Resort expansion contracts, New Tengah General & Community Hospital and MRT LTA extension contracts.

He has raised his FY2026 earnings estimates by 16% and has raised his target price from $5.10 to $5.30. Chong, who has a “buy” call, also notes that this counter is trading at an attractive FY2026 dividend yield of 5.3%.

UOB Kay Hian’s Tang Kai Jie and Heidi Mo, in their Feb 16 note, point out that BRC Asia has been improving its balance sheet, reducing debt and increasing net cash to $42 million as at the end of 2025.

Noting that operating cash flows have remained resilient at $53 million, they expect an attractive dividend yield of 5% in FY2026.

In the foreseeable future, BRC Asia is expected to benefit from the construction boom, with various infrastructure and building projects well underway or in the pipeline.

“Collectively, these large-scale developments should sustain a healthy pipeline of tender opportunities and help cushion against external market volatility,” say Tang and Mo, who have kept their “buy” call on this counter.

Their new target price of $5.10, from $4.90 previously, is pegged to 14.0 times FY2026 earnings, which they say is justified as it reflects BRC Asia’s strong positioning as the dominant player in Singapore’s steel market, and its status as a prime proxy for the ongoing construction upcycle, underpinning its earnings visibility and supporting a sustained growth trajectory. — The Edge Singapore

SIA Engineering

Price targets:

OCBC Group Research ‘buy’ $4.05

CGS International ‘add’ $4

Bullish following 9MFY2026 update

Analysts are upbeat over SIA Engineering Co’s (SGX:S59![]() ) (SIAEC) outlook after the company reported a net profit of $125.2 million for the 9MFY2026 ended Dec 31, 2025, 17% higher y-o-y. SIAEC’s 3QFY2026 net profit rose by 9.7% y-o-y to $41.9 million.

) (SIAEC) outlook after the company reported a net profit of $125.2 million for the 9MFY2026 ended Dec 31, 2025, 17% higher y-o-y. SIAEC’s 3QFY2026 net profit rose by 9.7% y-o-y to $41.9 million.

OCBC Group Research’s Ada Lim has upgraded her rating to “buy” from “hold” as SIAEC’s 9MFY2026 results “met expectations” with its basic earnings per share (EPS) for the nine months at 75.1% of her full-year forecast.

In her Feb 20 report, Lim likes SIAEC for several reasons, including its “constructive” outlook for its maintenance, repair and overhaul (MRO) business.

Citing data from the International Air Transport Association (IATA) that aircraft and engine order backlogs have reached almost 60% of active fleets as at December 2025 and Airbus guidance of lower-than-expected commercial plane deliveries in 2026, Lim also notes that limited aircraft and engine availability is hindering “significant” growth for aviation.

However, with the aircraft MRO segment in an “upcycle”, Lim is confident in SIAEC’s strategy to expand capacity. She notes that the company has secured the necessary regulatory approvals for the first of two hangars at Base Maintenance Malaysia (BMM), with the second hangar expected to come online in 2HFY2027. In addition, she points out that the company will commence line maintenance operations in Manila after the quarter.

Lim, who also has a higher fair value estimate of $4.05 from $3.68 previously, has lowered her cost of equity (COE) assumption to 7.1% from 7.6% due to lower risk-free rate and beta inputs. Lim has also increased her terminal growth rate assumption to 2.25%, 25 basis points higher.

CGS International’s (CGSI) Raymond Yap is also bullish on SIAEC with an unchanged “add” call.

Yap says SIAEC is “on track” for a “good” FY2026, although there may be several short-term pressures which contributed to a “flattish” q-o-q net profit. These include the 23.9% q-o-q drop in earnings before interest and tax attributed to “gestation losses” on the new hangar at BMM and also the start of line maintenance operations at the new Techo International Airport in Cambodia in September 2025. That said, the company’s results for the 3QFY2026 and 9MFY2026 still stood broadly in line with his estimates.

On the 17% y-o-y rise in 9MFY2026 core net profit, Yap attributes this to two reasons: the upward revision in contract rates charged to the SIA group from April 1, 2025 and the easing of supply chain constraints that allowed SIA Engineering to raise its output for engines and component repairs.

Yap also highlights several growth drivers for SIA Engineering. These include business expansion in Asia — the BMM hangars, potential operation of base maintenance facilities in India on behalf of Air India, and MRO capacity and capability enhancement for next-generation aircraft.

In particular for the company’s capability/capacity upgrading, Yap singles out the company’s letter of intent (LOI) with Safran Aircraft Engines in November 2025 to broaden SIAEC’s “partnership in CFM LEAP engine maintenance services” and the “potential formation of a JV (joint venture) in LEAP engine MRO in Singapore”. He alludes to the company’s engine services division at Changi becoming more efficient at turning around LEAP engines and to one of its outfits in Malaysia being able to repair a high-value component, the Air Data Inertial Reference Unit (ADIRU).

Downside risks for CGSI include project execution delays and larger-than-expected gestation losses for expansion projects. Yap expects gestation losses to see a peak between October 2026 and March 2027 when BMM’s second hangar is operationally ready. He also expects that the expansion of Singapore Aero Engine Services Private Limited (SAESL) will impact SIAEC’s financials from FY2026 to part of FY2028.

Yap’s unchanged target price of $4 is based on a target P/E of 25 times, which is one standard deviation above the mean since 2006. — Lin Daoyi

ISOTeam

Price target:

Maybank Securities ‘buy’ 12 cents

Cost savings from property acquisition

Jarick Seet of Maybank Securities has maintained his “buy” rating and 12-cent target price on ISOTeam (SGX:5WF![]() ) following the company’s announcement of the acquisition of a factory at 68 Loyang Way for $5.7 million.

) following the company’s announcement of the acquisition of a factory at 68 Loyang Way for $5.7 million.

ISOTeam will be converting this property to a workers’ accommodation that has the capacity of between 200-400 beds.

Seet, in his Feb 25 note, estimates that the company can achieve cost savings of $1.3 million a year, rising to $2.5 million following the expansion.

In addition, the company is expected to announce more orders in the near future, totalling $20 to $30 million, as a continuation of the pick-up in the pace of order wins. ISOTeam’s announced order book, as at Feb 11, was $176.2 million.

Of course, investors will be paying close attention to how ISOTeam can start deploying drones for painting works. The company, the only painting contractor with this plan in the pipeline, will begin with a pilot deployment in March. “We believe this will re-rate ISOTeam significantly if it can deliver these solutions,” says Seet.

The company recently reported 1HFY2026 earnings of $3.3 million, a 70% y-o-y increase, which supports the analyst’s expectation that ISOTeam will report a “stronger” FY2026.

Also, the company is likely to divest non-core assets worth between $7 and 10 million. Seet expects a portion of the proceeds from the sales could be used to reward shareholders with special dividends or higher ordinary dividends. — The Edge Singapore

StarHub

Price target:

DBS Group Research ‘fully valued’ 94 cents

Recovery only from FY2027

DBS Group Research has downgraded StarHub (SGX:CC3![]() ) to “fully valued” with a lower target price of 94 cents, down from $1.19.

) to “fully valued” with a lower target price of 94 cents, down from $1.19.

Analyst Sachin Mittal forecasts ebitda to fall about 20% in FY2026, broadly in line with StarHub’s guidance for a 20% to 25% decline, as consumer revenue slips and enterprise-related operating costs rise.

He projects a roughly 2.5% drop in consumer revenue next year, with mobile service revenue down about 2% as premium customers continue migrating to lower-priced SIM-only plans.

Without a big upward revision in the pricing for SIM-only offerings, blended mobile average revenue per user (ARPU) is likely to remain broadly stable in FY2026. “On a positive note, we expect the effect of sector consolidation to be visible in FY2027 with about 5% rise in mobile ARPU,” wrote Mittal in his Feb 19 note.

Similar pressure is expected across entertainment and fixed broadband, while higher capital expenditure and operating expenses tied to enterprise investments will weigh on margins.

StarHub plans to raise capital expenditure to 13% to 15% of revenue, focusing on cybersecurity and network retooling. Mittal says these enterprise investments should drive enterprise order book growth in FY2026 and lead to higher revenue in FY2027 and FY2028.

“This will enhance revenue visibility and build a moat that could take peers five to seven years to replicate,” he adds. At the same time, management has guided for $70 million in cost savings over FY2025 to FY2028, with the bulk of savings expected in FY2027 and FY2028.

Mittal now values StarHub’s core business at a 12-month forward EV/Ebitda of 6.3 times to arrive at 61 cents per share, down from 86 cents previously, excluding its stake in cybersecurity unit Ensign. He conservatively values Ensign at 25 cents to 41 cents per share based on two to three times its 12-month forward revenue, with a midpoint at 33 cents per share.

StarHub has also committed to a six-cent dividend for FY2026, which Mittal expects will help underpin the share price. — Nurdianah Md Nur