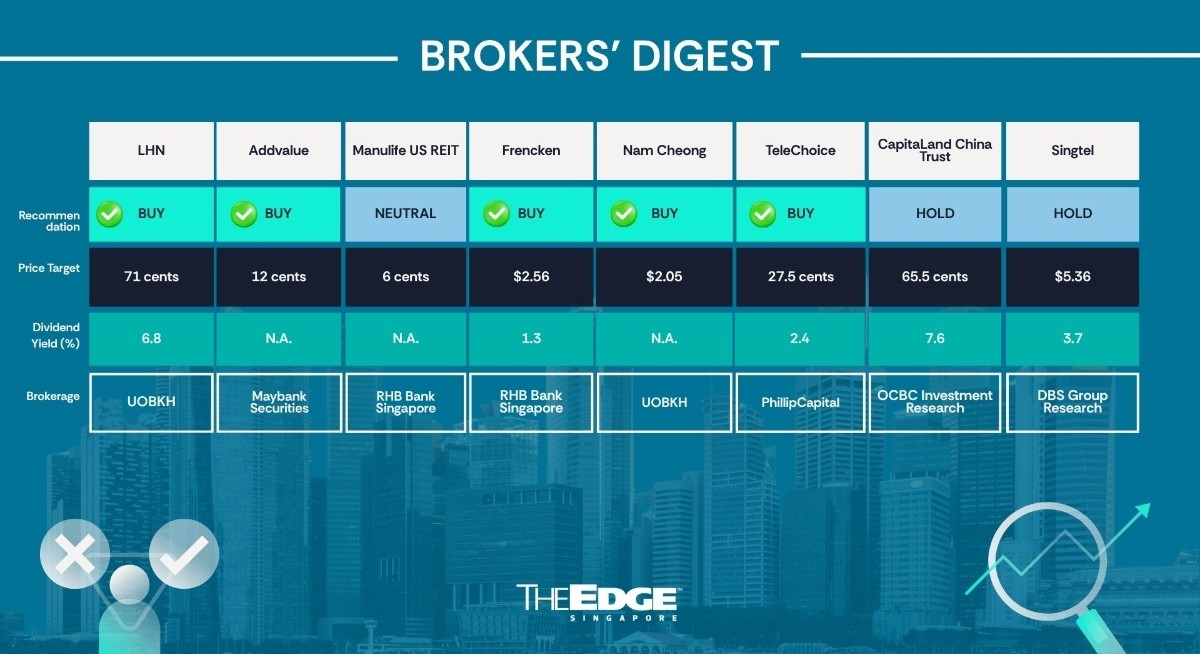

UOB Kay Hian ‘buy’ 71 cents

Resilient portfolio

UOB Kay Hian is reiterating its “buy” call on LHN (SGX:41O![]() ) with a lower target price of 71 cents from 84 cents previously. Analysts Heidi Mo and Tang Kai Jie like that the group continues to see strong occupancy rates across its core space optimisation business, signalling a “firm start” to FY2026 ending Sept 30.

) with a lower target price of 71 cents from 84 cents previously. Analysts Heidi Mo and Tang Kai Jie like that the group continues to see strong occupancy rates across its core space optimisation business, signalling a “firm start” to FY2026 ending Sept 30.

As at the end of 1QFY2026, co-living (Coliwoo) occupancy stood at 96.5%, an increase of 0.4 percentage points (ppt) q-o-q, while industrial and Work+Store spaces recorded healthy occupancies of 95.3% (–0.3 ppt q-o-q) and 93.1% (–5.9 ppts q-o-q due to the joint venture (JV) starting 1QFY2026), respectively.

See also: Broker's Digest: OUE REIT, HPH Trust, JustCo, CapitaLand Investment, Addvalue, CICT

“The resilient occupancy rates underscore the defensive, recurring nature of the group’s income base, supported by sustained tenant demand, which is likely to continue driving growth in LHN’s space optimisation business,” say the analysts.

LHN spin-off listed Coliwoo in November 2025, allowing Coliwoo its own platform to raise funds, while LHN can also focus on growing its other businesses. The Coliwoo portfolio expanded to 3,200 rooms, up from 2,933 rooms at the end of FY2025, attributable to a new accommodation management contract with a transport operator and 1 King George’s Avenue’s JV acquisition.

Of the 3,200 rooms in Coliwoo’s portfolio, 865 are currently under renovation, with the majority expected to be ready over FY2026. “We expect to see a continued uplift to operating metrics as these rooms come on-stream,” say Mo and Tang.

See also: Citing defensive yield, Beansprout initiates coverage on United Hampshire US REIT

Meanwhile, LHN’s capital recycling efforts are gaining pace. In 1QFY2026, LHN completed the sale-and-leaseback of Coliwoo Hotel Pasir Panjang ($43.9 million), transitioning the asset to a more asset-light structure while retaining operational control. The group has also recently proposed the sale of seven of its freehold assets, with a combined price tag of $218.5 million, with the intention of leasing them back and managing the properties, unlocking more value for the group.

LHN’s Work+Store business continues to deliver resilient, recurring income, supported by a high occupancy rate of 93.1% across its seven facilities and 2,014 units as at end-1QFY2026. While portfolio size remained unchanged during the quarter, management is focused on yield and margin optimisation, with plans to upgrade selected basic units into air-conditioned storage (around 10,000 sq ft targeted in FY2026), which the analysts believe should support higher rental rates and profitability over time.

Meanwhile, the facilities management segment continued to gain traction in 1QFY2026, with 14 new contracts secured and 100 contracts renewed, serving 119 clients across multiple sectors. Carpark operations also expanded steadily, with the portfolio reaching 105 carparks (around 28,500 lots) as at quarter-end, reinforcing the division’s scale and recurring income profile.

LHN also has two carpark projects in its pipeline, which are expected to add another 1,232 vehicle parking spaces to its facilities management business. Going forward, LHN aims to grow its facilities management segment through targeted M&A. As for the group’s energy and property segments, it is expected to continue scaling up through disciplined, asset-light initiatives. — Samantha Chiew

Addvalue Technologies

Price target:

Maybank Securities ‘buy’ 12 cents

For more stories about where money flows, click here for Capital Section

Possible US listing

Jarick Seet of Maybank Securities has maintained his bullish “buy” call and 12 cents target price for now on Addvalue Technologies (SGX:A31![]() ) . “Addvalue is benefiting from two of the sexiest and high-growth themes besides AI — drones and space,” says Seet in his March 20 note.

) . “Addvalue is benefiting from two of the sexiest and high-growth themes besides AI — drones and space,” says Seet in his March 20 note.

“We expect to see a rapid growth phase in the next few years following an inflexion point in FY2025 ended March 31, 2025. We believe Addvalue is one of the rare Asian space/drone plays in rapid growth mode,” he adds. Just recently, the company announced it is working to unlock the market value of its Inter-Satellite Data Relay System (IDRS) business in the US.

“We think a potential spinoff listing in the US market is highly possible, given the much richer valuations of its US peers, coupled with a potential listing of SpaceX and the high level of interest in the space sector,” says Seet.

He estimates that the IDRS business may generate between US$15 million ($19.17 million) and US$20 million in FY2027 revenue and between US$25 million and US$30 million in FY2028.

Addvalue’s production capacity is being expanded from 100 to 200 units per year by the end of 3QFY2026. Seet observes that Addvalue’s US peers are trading at valuations of 70–200 times price-to-sales; the company has a potential market cap in the US$200 to US$300 million range. “This allows Addvalue to raise capital at a much higher valuation and could also potentially sell a portion of the business and return cash to shareholders,” says Seet.

Meanwhile, the company has maintained steady new-order momentum. Most recently, on March 9, it won new IDRS orders worth US$3.7 million, bringing its total order book to a record of US$26.4 million. “We expect a higher frequency and value of orders ahead,” says Seet, whose target price of 12 cents is based on 35 times blended FY2027/2028 estimated valuation.” — The Edge Singapore

Manulife US REIT

Price target:

RHB Bank Singapore ‘neutral’ 6 US cents

FY2025 financials below expectations

RHB Bank Singapore analyst Vijay Natarajan is remaining “neutral” on Manulife US REIT (MUST) (SGX:BTOU![]() ) even though the REIT’s FY2025 stood below expectations. For the 12 months ended Dec 31, 2025, MUST reported gross revenue of US$113.9 million ($145.7 million), 32% lower y-o-y.

) even though the REIT’s FY2025 stood below expectations. For the 12 months ended Dec 31, 2025, MUST reported gross revenue of US$113.9 million ($145.7 million), 32% lower y-o-y.

Net property income fell by 33.4% y-o-y to US$53.2 million. Income available for distribution also fell by 33.2% y-o-y to US$25.5 million, translating to a distribution per unit of 1.44 US cents, 33% lower y-o-y. As at December 2025, MUST reported a 1.6% y-o-y decline in portfolio valuations, which are said to be “bottoming out”.

At its results call on March 19, MUST’s CEO John Casasante shared that the REIT was in active discussions to sell Figueroa at a slight discount to its latest valuation of US$98 million. If successful, the move would enable the REIT to repay its remaining debt of around US$56 million under its Master Restructuring Agreement ahead of its June deadline.

MUST also plans to invest in two more assets, which are expected to be completed by the end of the year. “These assets are likely to come from Tranche 1 & 2 of its portfolio, which are considered more challenging and capex-intensive,” says Natarajan.

Part of the proceeds from these divestments will likely be used to acquire industrial, living sector, and retail assets across the US and Canada under MUST’s new mandate. MUST also believes its sponsor’s large North American real estate portfolio and network can aid in a successful portfolio pivot, the analyst notes.

Natarajan’s new target price is pegged to a revised FY2026 book value multiple of 0.3 times, as he does not expect dividend payments in the near term. “Note that our estimates are based on MUST’s current portfolio, and are therefore subject to revisions as MUST executes its revamped growth strategy,” he says. — Felicia Tan

Frencken Group

Price target:

RHB Bank Singapore ‘buy’ $2.56

Pick up later this year

Alfie Yeo of RHB Bank Singapore has raised his target price for Frencken Group (SGX:E28![]() ) from $2.03 to $2.56, as there is now better visibility into its semiconductor customers, which will drive a pick-up in earnings growth in the second half of the year.

) from $2.03 to $2.56, as there is now better visibility into its semiconductor customers, which will drive a pick-up in earnings growth in the second half of the year.

Frencken’s earnings in FY2025 ended Dec 31, 2025 were in line with his estimates, with a slight 5% increase to $39 million over the preceding FY2024. Revenue in the same period was up 10% to $778 million. The company plans to pay a first and final dividend of 2.75 cents per share, equivalent to a 30% payout ratio.

According to Yeo, Frencken’s semiconductor segment previously slowed in 3QFY2025 due to excess inventory in its customers’ channels. In the most recent 4QFY2025, a recovery has started and appears to extend into 2HFY2026.

“While the outlook remains positive for Frencken on the earnings front, there is also optimism in the market’s positive fund flows, which has led to Frencken’s rerating,” says Yeo in his March 19 note.

Yeo observes that Frencken’s peers, since last May, have already re-rated to a 24 times forward P/E from 12–16 times previously. “In view of the firm earnings outlook, fund flows, and higher liquidity in the Singapore market, we now peg the stock from 19 times to 24 times FY2026 earnings, which is the peer average,” says Yeo. — The Edge Singapore

Nam Cheong

Price target:

RHB Bank Singapore ‘buy’ $2.05

Upside from chartering and new builds

Syahril Hanafiah of RHB Bank Singapore has initiated coverage of Nam Cheong (SGX:1MZ![]() ) with a “buy” call and target price of $2.05, given that the group is well-positioned for multi-year growth, thanks to its young fleet of offshore support vessels on long-term charters. More recently, the Sarawak-based company, after a hiatus of years, started to win contracts to build ships again, which will drive further earnings.

) with a “buy” call and target price of $2.05, given that the group is well-positioned for multi-year growth, thanks to its young fleet of offshore support vessels on long-term charters. More recently, the Sarawak-based company, after a hiatus of years, started to win contracts to build ships again, which will drive further earnings.

The company’s fleet is just nine years old on average, which makes the ships more attractive than the industry average of 14 to 16 years. In addition to multi-year contracts that provide earnings visibility, Nam Cheong also ships available for spot charters, which enables it to capture near-term upside.

Also, following years of under-investment in new ships due to the downturn, there is now greater demand for vessels as the industry is on an upcycle. Newer vessels, in particular, are in demand as indicated by the pick-up in resale activity.

Customers are placing orders for new ships too. Nam Cheong was recently given a US$64.5 million ($82.5 million) contract to build four offshore support vessels. “We believe that the growing appetite for younger builds could revitalise activity at Nam Cheong’s Miri shipyard, which has the capacity to build up to 12 vessels per year,” says Syahri.

In light of the ongoing dispute between Petronas and Petroleum Sarawak, Syahri says Nam Cheong is unlikely to face material disruption. According to the analyst, Sarawak’s offshore activity is expanding moderately as the state works to open more offshore areas for exploration, which will drive greater demand for offshore support vessels.

As a Sarawak-based operator, Nam Cheong is naturally aligned with this growth and well-positioned for state‑led offshore developments. At the same time, Nam Cheong maintains established commercial ties with Petronas, Malaysia’s national oil company. “With Sarawak’s rising strategic importance and Nam Cheong’s deep regional roots, the group remains well buffered against regulatory uncertainty,” reasons Syahri.

Other key re-rating catalysts, according to the analyst, include exposure to the renewable energy market, such as offshore wind energy; new geo-tech vessels with a variety of enhanced features; and accelerated debt repayment that could be sped up through potential future vessel sales, which can help lower financing costs.

Syahari expects Nam Cheong to record a three-year core earnings CAGR of 15%, mainly driven by its chartering segment with stable vessel utilisation and charter rates, gradual fleet expansion, and balance sheet deleveraging. His target price of $2.05 is based on 11 times FY2027 earnings, in line with its regional peers. — The Edge Singapore

TeleChoice International

Price target:

PhillipCapital ‘buy’ 75 cents

Growth prospects of mobile devices logistics

TeleChoice International (SGX:T41![]() ) reported FY2025 earnings that came in as expected by Paul Chew of PhillipCapital. However, with growth momentum in its main mobile device distribution segment — known as personal communication solutions, or PCS — and as it manages to turn around its smaller managed services and network buildout segments, Chew has raised his target price from 21.5 cents to 27.5 cents.

) reported FY2025 earnings that came in as expected by Paul Chew of PhillipCapital. However, with growth momentum in its main mobile device distribution segment — known as personal communication solutions, or PCS — and as it manages to turn around its smaller managed services and network buildout segments, Chew has raised his target price from 21.5 cents to 27.5 cents.

In the most recent fiscal year ended December 2025, TeleChoice’s revenue grew 27% y-o-y to $276 million, driven largely by the logistics management business the company provides to Malaysian operator U-Mobile. Adjusted patmi in the same period was up 20% y-o-y to $4.4 million, due to lumpy inventory provisioning. To signal its appreciation for shareholders, TeleChoice plans to pay a final dividend of 0.45 cent, up from just 0.125 cent paid for the preceding FY2024.

Specifically, revenue from the business of handling device logistics for key customer U-Mobile jumped 42% y-o-y to $200 million, driven by the telco’s growth in subscriber numbers and higher postpaid plan penetration. TeleChoice also increased the number of outlets, widened the range of phones and introduced more accessories, notes Chew.

On the other hand, TeleChoice had to make higher inventory provisions. Chew notes that there was a spike in inventory writedown, or a $2.5 million increase to $3.8 million. “We believe it is a general inventory provisioning rather than actual obsolescence,” he reasons.

According to Chew, the PCS segment will continue to be a key growth driver, riding on U Mobile’s aim to increase market share with the rollout of its 5G network, which implies more business for TeleChoice.

Also, its network engineering services segment will see growth with new managed services in Indonesia and the installation of network equipment in Malaysia.

A third business segment, ICT, or information and communication technology, is “recovering” as TeleChoice pursues more projects in healthcare and financial services, he adds.

For the current FY2026, Chew has raised his patmi forecast by 13% to $8.3 million and, applying the same 15 times P/E as other Singapore-listed proxies in the system integration and software sectors, derives a higher target price of 27.5 cents.

Down the road, the company is mulling further expansion into new, higher-growth segments within the digital infrastructure, including data centres, says Chew. — The Edge Singapore

CapitaLand China Trust

Price target:

OCBC Group Research ‘hold’ 65.5 cents

Expected yield-based returns of more than 8%

Ada Lim of OCBC Group Research upgraded her call for CapitaLand China Trust (CLCT) (SGX:AU8U![]() ) from “sell” to “hold” on March 23, noting that at current levels, this REIT should enjoy support from its FY2026 distribution yield of 7.6%.

) from “sell” to “hold” on March 23, noting that at current levels, this REIT should enjoy support from its FY2026 distribution yield of 7.6%.

Since her previous note on Feb 5, in which she downgraded this counter, CLCT’s share price has corrected by close to 18%, in part due to weaker sentiment across the S-REITs sector after the Iran war stoked inflation concerns and pushed back rate-cut expectations.

With expected total potential returns of 8.2% based on the March 20 closing price of 64.5 cents, she has kept her fair value at 65.5 cents.

CLCT is Singapore’s largest China-focused REIT, holding eight shopping malls, five business park properties and four logistics park properties across 11 Chinese cities. However, the portfolio is a mixed bag.

Since China’s emergence from the pandemic, there has been a divergence in performance between CLCT’s retail and new economy assets. “While the malls have benefited from a gradual consumption recovery, as well as active asset enhancement initiatives (AEIs) and repositioning, growth momentum and business sentiment remain lacklustre for the new economy assets,” says Lim.

“In the new term, we expect the retail portfolio to remain the anchor for CLCT’s performance, while downside risks in terms of occupancy and rental reversions persist for the new economy assets,” she adds.

Lim notes that China’s retail sales grew 2.8% y-o-y in the first two months of 2026, and CBRE Research is expecting cautious consumer sentiment and ample new supply to continue placing downward pressure on overall retail rents before a potential stabilisation in 2027.

For the logistics sub-sector, rents are expected to gradually bottom out and rebound around 2028, supported by limited new supply before 2030.

For Lim, potential catalysts include positive retail sales momentum buoyed by pro-consumption policies; higher-than-expected rental reversions; and, last but not least, distribution per unit-accretive acquisitions, AEIs and effective capital recycling.

On the other hand, risks include a slowdown in macroeconomic conditions, which would dampen consumer and business sentiment, significant costs to backfill vacancies and further depreciation of the renminbi against the Singapore dollar. — The Edge Singapore

Singapore Telecommunications

Price target:

DBS Group Research ‘hold’ $5.36

India associate Bharti’s share price easing

DBS Group Research analyst Sachin Mittal has downgraded Singapore Telecommunications (Singtel) (SGX:Z74![]() ) to “hold”, citing limited upside after a sharp re-rating. He has lowered his target price to $5.36 from $5.71 previously.

) to “hold”, citing limited upside after a sharp re-rating. He has lowered his target price to $5.36 from $5.71 previously.

Over the past 12 months, Singtel’s share price has risen by more than 51%, with about half of the gains driven by a narrowing of the holding company discount. The rest came from higher valuations of its regional associates and a modest re-rating of its core business.

However, that discount has now compressed to approximately 7%, an eight-year low, leaving what Mittal describes as limited scope for further re-rating. The shift reflects diverging share price performance between Singtel and its largest associate, Bharti Airtel.

Bharti Airtel shares have declined about 13% year-to-date, while Singtel has gained roughly 12%. A weaker Indian rupee against the Singapore dollar has further reduced Bharti’s contribution in Singapore-dollar terms, even though it still accounts for about half of Singtel’s sum-of-the-parts valuation.

Mittal expects Bharti Airtel’s downside risks to weigh on earnings, as tariff hikes are likely to be delayed until late 2026 or early 2027 amid pressure on consumer spending from higher energy costs.

Factoring in a delayed tariff increase of about 15%, he estimates a 3% to 4% downside risk to Bharti’s FY2027 ebitda forecasts and a steeper 12% to 15% downside to net profit expectations. While earnings are still projected to grow around 25%, this falls short of consensus expectations of more than 40%.

As a result, Mittal expects Singtel’s FY2027 earnings to come in about 7% below consensus, largely due to weaker contributions from Bharti and currency headwinds.

Reflecting these changes, he has lowered his valuation for Bharti Airtel, cutting its target price to INR2,000 ($27.24) and reducing the implied value of Singtel’s stake to $2.60 per share from $3.13 previously.

On the domestic front, Mittal flags potential pressure on Singapore telecom earnings. Sector consolidation has been delayed pending regulatory approval for a merger between smaller operators, while StarHub has guided for a 20% to 25% decline in group ebitda in 2026, suggesting a slower recovery in the mobile market.

Singtel has delivered about $200 million in annual cost savings over the past three years, supporting earnings stability. However, these savings have largely been exhausted, and consensus forecasts of stable Singapore operating profit in FY2027 may be optimistic.

“In the absence of more cost savings coupled with an intensified competition from a more aggressive StarHub, we cannot rule out downside risk of 5% to 6% to consensus Singapore telco estimates or 2% to 3% to consensus ebit estimates for the operating company,” writes Mittal in his March 23 note.

Mittal keeps his valuation of Singtel’s core operations unchanged at six times forward EV/Ebitda for Singapore and Optus, while maintaining a 25 times forward EV/Ebitda for its data centre business, implying a core value of about $1.57 per share.

Dividend yield also offers limited support, with Singtel yielding below 4%, compared with a five-year average of 4.8%, he adds.

Singtel continued with its $2 billion share buyback programme on March 23. It paid between $4.92 and $4.97 for more than 3.36 million shares. — Nurdianah Md Nur