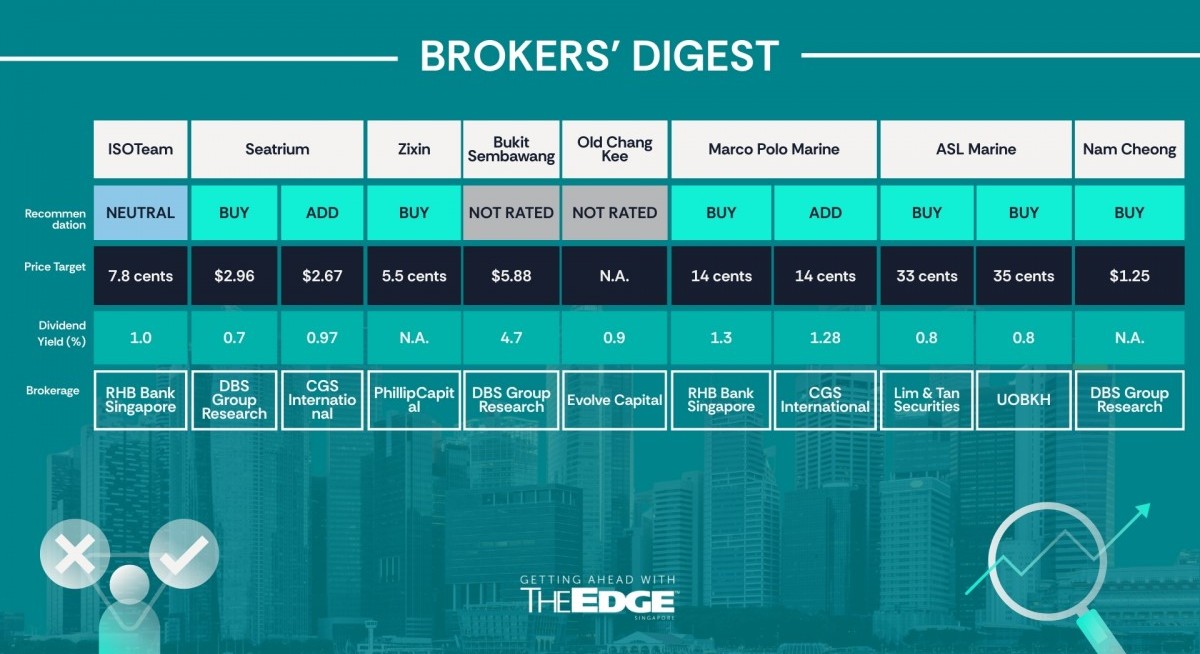

RHB Bank Singapore ‘neutral’ 7.8 cents

Dilution pressure; awaiting new orders

Alfie Yeo of RHB Bank Singapore has held his “neutral” call and 7.8 cents target price on ISOTeam, as he awaits better valuation and earnings performance.

Yeo, in his Nov 27 note, cautions that shareholders face a 12% EPS dilution following a recent fundraising round.

See also: Broker's Digest: OUE REIT, HPH Trust, JustCo, CapitaLand Investment, Addvalue, CICT

“Dampeners to its immediate growth visibility include an 11% lower order book in FY2025 ended June 30 vs FY2024, slower pace of revenue recognition, moderating construction GDP growth, and slow commercialisation of its drone technology,” says Yeo.

On Sept 25, Yeo had downgraded the counter from “buy” to “neutral” while holding his target price at 7.8 cents, as he warned of slow revenue recognition.

In addition, Yeo notes that Singapore’s construction sector growth moderated in 3Q2025, up 3.1% from the 6.2% jump in 2Q2025.

See also: Citing defensive yield, Beansprout initiates coverage on United Hampshire US REIT

In FY2025, the company also reported an 11% lower order book of $162 million, down from $183 million in FY2024, potentially dampening the immediate-term revenue available for recognition.

The recent $10 million fundraising was intended to support the commercial deployment of its drone fleet for painting work.

“Full commercialisation of its drone technology will take time. With pilot projects targeted only from 4QFY2026, commercialisation is expected only in FY2027,” notes Yeo, adding that another $2 million is needed for drone R&D costs.

“Even after drone commercialisation in FY2027, revenue should ramp up progressively before it benefits from a full year’s contribution in FY28F,” reasons Yeo.

“Most importantly, ISOTeam’s order book needs to grow. We await more project wins and for the pace of project recognition to pick up before we consider upgrading our stock recommendation to ‘buy’,” adds Yeo.

The $10 million raised recently came from a share placement and a convertible bond issue. He warns that ISOTeam shareholders will face further EPS dilution when the bonds are up for conversion at 9.126 cents. Yeo estimates another 4.44% dilution when this happens.

“We look to price in this EPS dilution when bondholders consider converting their holdings into shares, at a level where our target price or the current share price is nearer to the conversion price,” says Yeo.

For more stories about where money flows, click here for Capital Section

Meanwhile, ISOTeam faces downside risks, including higher raw material and labour costs, a slowdown in the pace and revenue recognition of projects, delays in launching the drone project, and slowing new order wins, which results in a weaker order book. — The Edge Singapore

Zixin Group

Price target:

PhillipCapital ‘buy’ 5.5 cents

Earnings dilution from share options

Serena Lim of PhillipCapital cut her target price for Zixin Group following the company’s 1HFY2026 earnings, which fell short of expectations.

In 1HFY2026 ended Sept 30, revenue was up 40.8% y-o-y to RMB220.6 million ($40.37 million), driven by growth across its segments.

However, earnings were up by just 3.9% y-o-y as the company incurred higher income tax and R&D costs. At this halfway mark, the bottom line was just 29% of what she expected for FY2026.

She remains upbeat about the company’s prospects, given the visible growth plans and as indicated in her Nov 28 note, kept her “buy” call.

On the other hand, with Zixin’s share base expanding because of the issuance of share options, Lim has cut her target price from 6 cents to 5.5 cents.

In 1HFY2026, Zixin’s processed products segment saw sales volume increase by 40.7% y-o-y, driven by expanded capacity. This helped lift earnings for processed products by 68.6% y-o-y.

Earnings from its fresh sweet potato segment declined 39% y-o-y, despite higher production, as Zixin paid farmers more for sweet potatoes grown by them. Prices rose due to typhoon-related disruptions. Margins were further compressed due to higher overheads, specifically new machinery.

Nonetheless, from 30.2% in 1HFY2026, Lim expects Zixin’s gross margin to improve slightly to 31.5% for the full year, supported by higher fresh sweet potato output during the harvest season and by increasing production volume of high-margin processed products from the new facility.

Lim sees a few long-term catalysts. For one, Zixin, backed by higher R&D spending, is producing a larger share of so-called premium seedlings to better capture growing demand.

In addition, Zixin expects to ramp up its output over at its Hainan operations, where the planting area is five times that of its existing central location at Liancheng in Fujian province.

“This positions Hainan as a primary multi-year growth driver as capacity scales and downstream processing infrastructure are progressively deployed,” says Lim. — The Edge Singapore

Bukit Sembawang Estates

Price target:

DBS Group Research ‘unrated’

‘Potential dividend powerhouse’

DBS Group Research analysts Tabitha Foo and Derek Tan see one of Singapore’s longest-standing residential developers, Bukit Sembawang Estates, as a “potential dividend powerhouse”.

In a Nov 28 unrated report, the DBS analysts see the company’s core engine lies with the property development segment, underpinned by a substantial landbank of more than 1.5 million sq ft, which could be progressively redeveloped into landed homes.

This equates to an estimated gross development value (GDV) of $2.5 billion ($9.54 per share), providing multi-year income visibility.

“Given Singapore’s acute land scarcity and tightly regulated supply, the structurally tight supply-demand backdrop continues to underpin price resilience of landed properties across cycles — making Bukit Sembawang’s landbank all the more valuable,” they state.

In both Foo and Tan’s view, Bukit Sembawang is a good potential candidate for outsized capital return and anchored by a “best-in-class” balance sheet.

“The company stands out among Singapore developers with its fortress balance sheet and its high-quality landbank. The group holds record cash of $2.25 per share and carries zero debt, affording it exceptional financial flexibility and scope to deliver materially higher payouts.

Based on their estimates, a “bonanza” special dividend of up to $1.00 per share is well within reach for Bukit Sembawang, which underscores the embedded capital efficiency and near-term catalysts for a meaningful re-rating of the company’s stock.

With this, the DBS analysts have indicated a fair value of $5.88 a share for Bukit Sembawang’s stock. Their fair value is pegged to a 45% discount of their revalued net asset value, in line with the rest of the developer peers. — Teo Zheng Long

Old Chang Kee

Price target:

Evolve Capital ‘unrated’

In need of fresh growth catalysts

Evolve Capital analyst Ethan Aw, in his Nov 28 un-rated report, highlights Old Chang Kee’s need for fresh growth catalysts amid the broader slowdown in the F&B sector.

In the recent 1HFY2026 earnings, Old Chang Kee’s revenue growth was flat at only 0.2% y-o-y, with both outlet and non-outlet sales remaining stable.

“The flat performance was partly attributable to the loss of a corporate customer; excluding this, non-outlet sales would have shown modest positive growth. Although the company has been introducing new food initiatives at its outlets, it hasn’t been spared from the broader F&B slowdown,” states Aw.

Back in his June initiation report on Old Chang Kee, Aw says that the company continues to prioritise expanding its non-outlet sales channels as a means of diversification and to improve utilisation of its central kitchen.

On the profitability front, Old Chang Kee’s gross profit was broadly unchanged, but ebitda and patmi declined by 8.1% and 19.3% y-o-y, respectively. The weaker bottom line was mainly driven by higher staff costs following wage adjustments under the government’s Progressive Wage Model (PWM), implemented in March 2023.

Under the PWM framework, workers’ wages are expected to increase by approximately 5%–10% per year on average from March 2023 to February 2026.

Aw would like to see the company introduce new key catalysts to spur top-line growth, especially given rising cost pressures from wages and rentals.

“Current initiatives such as the introduction of new food sets at its outlets are unlikely to meaningfully grow profitability in the near-medium term, in our view, especially since its outlet count has generally remained stable for quite some time,” says Aw.

On the balance sheet front, Old Chang Kee remains healthy with a strong net cash position and total cash holdings of $56.2 million as of 1HFY2026.

Meanwhile, Aw states that Old Chang Kee’s management has begun exploring opportunities in the Ready-to-Eat (RTE) segment, including the potential rollout of some of its popular products, such as frozen curry puffs, in supermarkets.

“We view this as a positive, as it aligns with the group’s strategy to grow its non-outlet sales channels. These initiatives are not expected to require additional capex, as the production of RTE products can be supported by existing machinery,” adds Aw. — Teo Zheng Long

Seatrium

Price targets:

DBS Group Research ‘buy’ $2.96

CGS International ‘buy’ $2.67

FPU contract win

Analysts from DBS and CGS International (CGSI) remain upbeat on Seatrium’s prospects after the offshore and marine player announced it won a second contract to build a floating production unit (FPU) for BP. With the Tiber FPU win, Seatrium has secured more than $2 billion in contracts for 2025.

DBS’s Ho Pei Hwa maintains her “buy” rating and $2.96 target price. She estimates the new contract win for the Tiber FPU at around $1.3 billion, similar to the Kaskika FPU.

Net order book would “hover around” US$16 billion ($20.8 billion) by the end of the year, according to her report issued on Nov 26. With the bulk of projects from Petrobras and Tennet being series-built with staggered deliveries (presumably with staggered payments), Ho expressed concern about the company’s revenue coverage, which is estimated to be less than two times.

However, she thinks that Seatrium “will likely” win more contracts for floating, production, storage, and offloading (FPSO) vessels and high-voltage direct current (HVDC) stations from these two customers next year. Ho also notes that Seatrium is pursuing contracts worth $30 billion.

Despite the stock underperforming this year due to low order wins and adverse developments such as Maersk’s cancellation of a wind turbine installation vessel (WTIV) order, Ho remains optimistic about Seatrium. Possible tailwinds for a re-rate include more sizeable contract wins and higher margins.

Meanwhile, Lim Siew Khee and Meghana Kande from CGSI maintain their “buy” call and $2.67 target price in their Nov 26 analysis. Their view is shaped by Seatrium’s path to profit recovery and its FY2025–FY2027 growth forecast, which is underpinned by higher-margin orders.

Their target price is calculated based on a forecast FY2026 P/B of 1.3 times. They gave a 10% discount to the counter’s historical P/B of 1.5 times to account for lumpy contract wins.

Although the pair estimated a similar value for the Tiber FPU contract as Ho, they wrote that Seatrium has a current order book of around $17.9 billion.

Lim and Kande estimate “gross margins of 10%–12%” for Tiber FPU, which will be primarily built in Singapore. This is in line with management’s guidance in previous analyst briefings of mid-teens risk-adjusted project margins.

The duo also analysed Seatrium’s potential contract wins, predicting $6 billion in orders for 2026, based on the $30 billion in contracts the company is pursuing.

Since Seatrium is overseeing the integration/module construction for two other FPSOs for ExxonMobil via Modec and SBM Offshore, they believe potential contract wins include FPSO integration/module fabrication for Modec following the final investment decision for ExxonMobil’s seventh offshore oil development in the Stabroek block in Guyana. They note that cost overruns and project cancellations are key risks for the counter. — Lin Daoyi

Nam Cheong

Price target:

DBS Group Research ‘buy’ $1.25

'Rerating catalysts in sight'

DBS Group Research, on Dec 3, reiterated its “buy” call and target price of $1.25 for Nam Cheong, alluding to a possible re-rating.

This comes on the back of the potential finalisation of a commercial agreement between Sarawak’s state-owned Petroleum Sarawak (Petros) and Petronas. Sarawak’s utility and telecommunication minister Julaihi Narawi said that the accord will be concluded by Dec 31 at the latest.

The East Malaysian state holds about 60% of the country’s gas reserves and accounts for nearly 90% of its LNG exports. It has established the Sarawak gas roadmap, which aims to increase domestic gas usage from 7% to at least 30% by 2030.

However, the initiative seems to have lost momentum, with Petronas cutting capex by around 20% to RM43 billion ($13.52 billion) this year due to the state’s gas overhang and a moderation in oil prices.

DBS notes that the Petros-Petronas pact will be a “breath of fresh air”, offering “regulatory certainty and strong support for upstream investments in the region” and “reigniting upstream investment momentum and demand” for offshore assets.

If the agreement is finalised by year-end, Malaysian offshore support vessel (OSV) supplier Nam Cheong is well positioned to capitalise on the renewed appetite for offshore assets. Propelling the counter’s growth includes two idling OSVs, which would be in demand once upstream activity revitalises, adding 7% to 8% to group profit, says DBS.

The report adds that the shipyard, capable of handling six to eight OSVs simultaneously, is key to growth, with one newbuild order adding 2% to 3% to earnings and fair value. DBS has not factored in the potential earnings into its FY2026 forecast, although it predicts they would add 10% to 20% to the FY2026 bottom line.

At a target price of $1.25, or eight times forecast FY2026 earnings, DBS highlights Nam Cheong as an “undervalued OSV gem” because it trades at only five times earnings. Despite steady income streams that are 60% to 70% backed by long-term charters, DBS points out that the counter “remains unwarrantedly undervalued” relative to peers ASL Marine (nine times P/E), PACRA (10 times P/E) and Marco Polo Marine (14 times P/E).

Based on the above factors, DBS suggests that a rerating is on the cards, writing: “We believe potential newbuild orders and the redeployment of idling vessels in 1Q2026, especially with Sarawak gas resolution, to drive share price re-rating after relatively muted earnings growth in 2025.” — Lin Daoyi

Marco Polo Marine

Price targets:

CGS International ‘add’ 14 cents

RHB Bank Singapore ‘buy’ 14 cents

Higher target prices following FY2025 earnings jump

Analysts from CGS International (CGSI) and RHB have reiterated their “buy” call for Marco Polo Marine after the offshore and marine player announced a positive set of results for FY2025 ended Sept 30.

In their report issued on Dec 1, the CGSI pair of Meghana Kande and Lim Siew Khee maintained their target price of 14 cents. Their valuation is based on a forecasted P/E of 13 times for FY2027, which justifies the 40% premium over peers due to earnings visibility.

Meanwhile, using discounted cash flow, RHB’s Alfie Yeo estimates a target price of 14 cents, up from 12.2 cents previously. He adds that this valuation is 13 times the FY2026 forecast P/E, below its 20% CAGR from FY2025 to FY2028.

Marco Polo Marine’s net profit attributable to shareholders jumped to $58.5 million, a y-o-y increase of nearly 170%. The performance was attributed to one-off gains and stronger performance for the ship-chartering segment.

Meanwhile, gross profit margin strengthened to 44.1% from 39.3% a year ago, while gross profit rose 11.8% y-o-y to $54.2 million.

The CGSI analysts noted that full-year revenue was in line with expectations. Excluding extraordinary contributions, core patmi of $25.2 million was “ahead” of expectations.

They attributed gross margin improvement to the new commissioning service operation vessel (CSOV) that has been chartered to Siemens Gamesa at a day rate of US$65,000 ($84,000) since April.

However, for FY2026 to FY2028, they forecast that gross margin could decrease and “stabilise” between 36% and 43% as the CSOV will be chartered to a long-term contract with Vestas at US$45,000 per day. Gross margin could also decrease as work begins on a newbuild order, which typically carries lower margins.

Kande and Lim are optimistic about the upcoming new projects that would propel long-term growth into FY2028. With a new dry dock that began operations in August, they expect an increase in ship repair work and revenue from newbuilds in FY2027.

For chartering revenues, they forecast an increase in FY2026 due to contributions from the CSOV and two new anchor-handling tug supply (AHTS) vessels coming into service in the 2HFY2026.

They forecast a FY2028 net profit of $46.8 million, representing a 23% CAGR from FY2025 to FY2028. They attribute the profit increase to a second CSOV scheduled for delivery in 2QFY2028 and a $198 million newbuild contract for a research vessel to be built over FY2027 to FY2029.

Key downsides for Kande and Lim include lower-than-expected utilisation of yards or fleets, and delays in offshore wind projects that affect vessel demand.

Similarly, Yeo is bullish on Marco Polo Marine due to its “accelerating growth outlook” and has gained more confidence in the company’s prospects with FY2025’s operating profit “outperforming strongly”.

He notes that revenue grew in the ship chartering segment on the back of the first CSOV’s deployment and three additional crew transfer vessels (CTV). Fleet utilisation also increased to 71%, compared to 68% for FY2024.

Yeo attributed the revenue decline for shipbuilding and repair to the construction of its already deployed CSOV, which reduced its shipyard’s capacity for third-party shipbuilding projects. However, this decline was offset by more shipbuilding projects with higher contract values and an increase in the shipyard utilisation rate for ship repair to 83% from FY2024’s 74%.

Although both ebit and core earnings outperformed his earlier estimates by 29% and 14%, respectively, he does not expect revenue to increase in FY2026 or FY2027. However, he believes margins will be stronger and has raised earnings forecasts by 15% and 13% for FY2026 and FY2027, respectively. He writes that the forecast is “premised on a higher fleet size, improved charter rates, stronger utilisation rates, and the recent shipbuilding contract coming through”. — Lin Daoyi

ASL Marine

Price targets:

UOB Kay Hian ‘buy’ 35 cents

Lim & Tan Securities ‘buy’ 33 cents

Higher-than-expected 1QFY2026

ASL Marine’s higher-than-expected earnings for 1QFY2026 ended Sept 30 have prompted analysts from UOB Kay Hian (UOBKH) and Lim & Tan Securities to increase their target prices to 35 cents and 33 cents from 33 cents and 30 cents, respectively. Both brokerages have maintained their “buy” calls.

In light of the company’s strong showing, UOBKH is raising its earnings forecasts for FY2026 to FY2028 by 6% to 9%. Based on valuing ASL’s peers at a P/E of 11.6 times FY2026 forecasted earnings, ASL is thus trading at a 25% discount, with its current price hovering around nine times the P/E of FY2026 forecasted earnings. With more contract wins and deleveraging on track, UOBKH analyst Heidi Mo believes ASL is undervalued relative to its peers.

Nicholas Yon from Lim & Tan forecasts profit to increase to $32.2 million and $35.8 million for FY2026 and FY2027, respectively. The TP is based on an unchanged 2027 forecast P/E of 9.5 times. He notes a “bull-case scenario” in which earnings could reach $36 million or $39 million if contract wins and margins increase.

In 1QFY2026, ASL Marine announced revenue of $94.2 million and net profit of $8.3 million, a y-o-y increase of 12.1% and 1,560% respectively.

In her report issued on Dec 2, Mo wrote that the first quarter earnings formed 30% of full-year estimates and “beat our expectations”. The unexpected result was attributed to “stronger ship repair and shipbuilding contributions” as well as improved chartering margins and substantially lower finance costs.

Analysing the various business segments, both analysts are upbeat on ASL’s prospects and note that the shipbuilding segment remains anchored to the $83 million order book.

For ship chartering, Mo expects gross margin to have “risen meaningfully toward the mid-teens, supported by the deployment of more vessels at higher day rates”. With the new $82 million contracts secured in October, she notes that chartering margins are expected to remain in the 10% to 15% range as the utilisation rate improves throughout FY2026.

Meanwhile, Yon thinks there is also room for growth for the ship chartering segment as utilisation and charter rates improve while the company “renews older contracts at higher prices”.

Yon also believes that ship repair will be the “standout performer” as the company continues to capitalise on this high-margin and growing business.

With tight drydock capacity across Singapore and Batam, coupled with “sustained demand” for ship maintenance and repair, Mo expects ship repair to continue to deliver “healthy volume growth”. She adds that the new floating dry dock, scheduled for completion in early FY2027, could boost the company’s performance in the medium term.

Mo notes that management has articulated a “clearer strategic focus” on ship repair and chartering, which provides more sustainable recurring income compared to the cyclical nature of shipbuilding.

With ASL’s past participation in key national projects such as the Jurong Island Road Link and the Pulau Tekong reclamation, she believes ASL is well-positioned to secure contracts arising from Singapore’s $100 billion coastal protection plan, including Phases 3 and 4 of the Tuas Mega Port project and the Long Island Reclamation Project.

Another positive development noted by both analysts was the company’s focus on deleveraging, with recent vessel disposals part of a deliberate deleveraging effort. The company also confirmed that FY2025 marked the final year of significant non-cash loan amortisation, paving the way for lower finance costs ahead.

The company shared that financing costs decreased by $4 million as deleveraging efforts gained steam. Borrowings, which reached $592 million in 2016, stood at less than $179 million as at June 30.

In an earlier report, Mo notes that annual interest savings of $7 million to $8 million are expected to lift ASL Marine’s net margins by three percentage points and accelerate free cash flow generation.

UOBKH also believes that the company’s gains offset the impact of the fire that occurred on Oct 25 at ASL Marine’s Batam yard. This was the second fire to occur at the yard this year. An earlier fire occurred on the same tanker at the yard in June.

Share prices could also get a boost should ASL Marine win more contracts and offer a higher dividend payout, notes Mo. — Lin Daoyi