Ignore the short-term noise

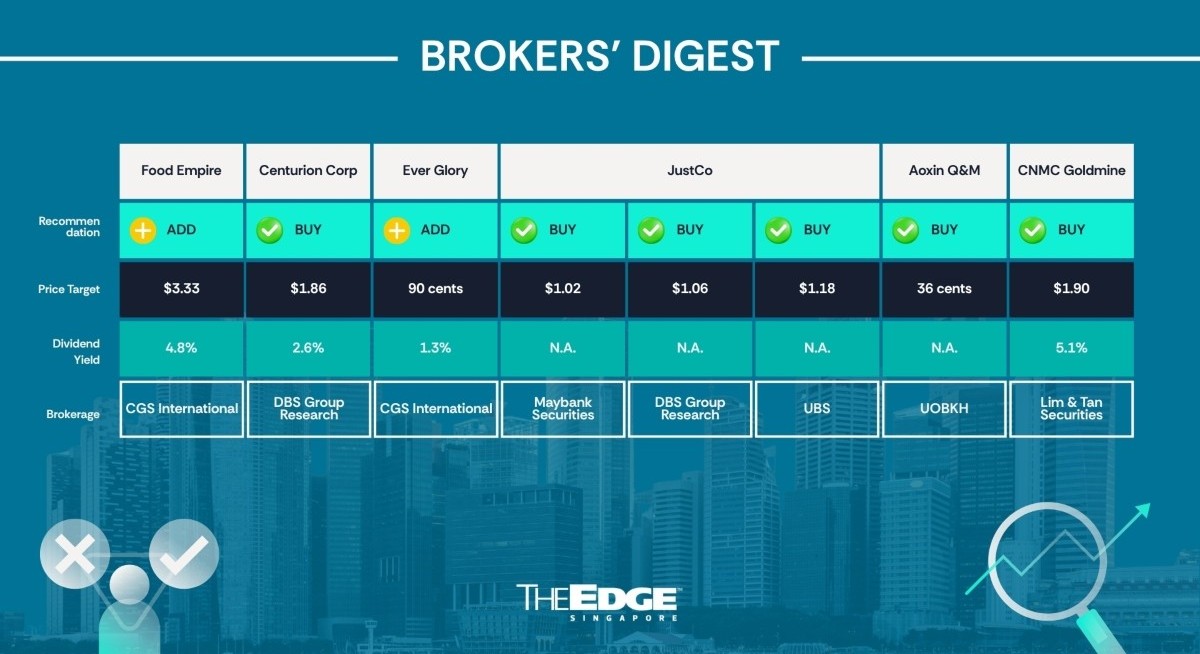

William Tng of CGS International has remained upbeat on Food Empire Holdings (SGX:F03![]() ) . He urges investors not to be “distracted” by the “short-term noise” of the ongoing fighting in the Middle East.

) . He urges investors not to be “distracted” by the “short-term noise” of the ongoing fighting in the Middle East.

Citing an interview with CEO Sudeep Nair published in The Edge Singapore on June 26, Tng notes that due to the constriction in oil supply, the company has seen a 20% increase in its packaging material costs. This is deemed not serious enough to “significantly” affect its margins.

Tng estimates that labour and packaging form around 30% of Food Empire’s cost of goods sold. He believes that, despite fears over higher input costs, Food Empire has, over the years, built strong branding to support its efforts to grow its own-brand products.

See also: RHB keeps Marco Polo Marine at ‘buy’ with 21 cents target

Tng estimates that the company will report 1HFY2026 revenue of US$303.7 million, up 10.8% y-o-y and 0.3% h-o-h, as well as net profit of US$ 34.9 million, up 10.6% y-o-y but down 6% h-o-h. He also expects the company to maintain an interim dividend of 3 cents.

Now, to reflect a larger share base following a recent one-for-five bonus issue, Tng has cut his FY2026 and FY2028 EPS forecasts by 16.7% and 16.8%, respectively.

He has kept his 9%–13% core EPS growth over FY2027 to FY2028 and, by applying the same 20.5 times FY2027 earnings valuation multiple, derived a lower target price of $3.33.

See also: Analysts positive on FCT’s potential award to build ‘next suburban retail landmark’ at Bayshore

Tng notes that at this valuation, Food Empire has been accorded a 1.4.5% premium to its international peers’ 17.9 times 2027 sector average. He justifies the higher valuation to Food Empire’s better three-year EPS CAGR and 4.8% dividend yield.

Potential re-rating catalysts include improving operating margins on stabilising market demand; sustained market share in its key market, Russia, which accounts for nearly a third of revenue; and resolution of the Russia-Ukraine conflict.

Downside risks include escalation of the conflict, which could affect its Russian operations, and depreciation of the ruble against the US dollar, leading to lower revenue in US dollar terms, the currency in which Food Empire reports. — The Edge Singapore

Centurion Corporation

Price target:

DBS Group Research ‘buy’ $1.86

Two new potential sites

Dormitory operator Centurion Corporation (SGX:OU8![]() ) has submitted the highest bids for two sites allocated for the construction of new dormitories, according to tender results published by JTC Corporation and on the public-sector e-procurement portal GeBIZ.

) has submitted the highest bids for two sites allocated for the construction of new dormitories, according to tender results published by JTC Corporation and on the public-sector e-procurement portal GeBIZ.

For more stories about where money flows, click here for Capital Section

The first site is a 2.84ha plot on Lok Yang Way. With a gross plot ratio of 2.0, the site can accommodate 5,000 beds, and Centurion put in a bid of $221.7 million. This tender drew 10 bids and closed on June 23.

The second site, at Kranji Close, covers 2.21ha and has a higher gross plot ratio of 3.0, which means some 7,000 beds can be built. Centurion bid $343 million. This tender also drew 10 bids and closed on June 12.

If Centurion is awarded both sites, it could increase its capacity for purpose-built workers’ dormitories by 12,000 beds, representing a 30% expansion from its current capacity of 39,918 beds.

“The developments would further strengthen the group’s market-leading position in Singapore’s worker accommodation sector,” says DBS Group Research analyst Ng Jia Hui in a July 13 note.

“While being the highest bidder does not guarantee an award and the evaluation process is expected to take 1–2 months, a successful outcome would be a positive catalyst for Centurion,” she adds.

Both sites will come with a 30-year lease each. From Ng’s perspective, this can help provide a long runway for recurring earnings growth and enhance earnings visibility.

She estimates that the projects can generate yield on cost between 5.7%–6.2% and deliver a 19%–21% uplift in ebit (once completed in FY2028–FY2029), supported by favourable demand-supply dynamics in Singapore’s worker accommodation market.

“In addition, the new assets could further enhance Centurion’s pipeline of stabilised assets for potential future injection into Centurion Accommodation REIT, supporting its capital recycling strategy,” says Ng, who has kept her “buy” call and $1.86 target price, which will be revisited if the tender is successful. — The Edge Singapore

Ever Glory United Holdings

Price target:

CGS International ‘add’ 90 cents

More order book wins

Then Wan Lin and Natalie Ong of CGS International have kept their “add” call for Ever Glory United Holdings (SGX:ZKX![]() ) . They say the mechanical and engineering firm is set for further earnings growth, driven by an order book that could reach $1 billion, up from $950 million as of May.

) . They say the mechanical and engineering firm is set for further earnings growth, driven by an order book that could reach $1 billion, up from $950 million as of May.

This is supported by their investment thesis of strong order momentum from its tender pipeline of more than $4 billion as of February.

For the upcoming first-half results, the CGSI analysts expect the company to report revenue of $117 million. At this level, it is a 309% y-o-y and 33% h-o-h jump, driven by the consolidation of Guthrie Engineering, which was acquired in 2HFY2025, as well as ongoing execution of its $950 million order book.

Then and Ong further estimate Ever Glory’s core 1HFY2026 net profit to reach $10 million, up 12% h-o-h, with gross profit margin potentially coming in stronger than their FY2026 estimate of 16%, as higher-margin contracts won in 2025 start to be recognised.

They say Ever Glory can chalk up approximately another $400 million in order wins by the end of the second half of this year, which would likely include $250 million to $300 million in public infrastructure projects flagged earlier, as well as $100 million to $120 million from private projects.

For Then and Ong, investors should look out for Ever Glory’s potential dual-primary listing in Hong Kong, with trading possibly commencing by 2QFY2027. However, they do not see this as an immediate catalyst. They note that Ever Glory’s closest Hong Kong-listed comparables include Analogue Holdings and Accel Group, which have smaller M&E engineering segment earnings bases and more diversified earnings streams.

The analysts have maintained their target price of 90 cents, based on 15 times FY2027 earnings, a level 1.5 standard deviations above the company’s historical three-year mean and in line with the regional peers’ average.

Then and Ong maintain that this is a “reasonable” level given Ever Glory’s “robust” earnings growth of 28% between FY2025 and FY2028. Re-rating catalysts include stronger-than-expected order wins, margin expansion, share buybacks and accretive M&As. On the other hand, downside risks include sharper-than-expected cost escalation and delays in project awards or execution. — The Edge Singapore

JustCo Holdings

Price targets:

Maybank Securities ‘buy’ $1.02

DBS Group Research ‘buy’ $1.06

UBS Global Research ‘buy’ $1.18

Visible earnings growth

On July 15, Liu Miaomiao of Maybank Securities initiated coverage of the newly listed JustCo Holdings (SGX:JCO![]() ) with a “buy” rating and a target price of $1.02. Liu says her valuation is supported by metrics including visible earnings growth, improving occupancy and strong operating leverage.

) with a “buy” rating and a target price of $1.02. Liu says her valuation is supported by metrics including visible earnings growth, improving occupancy and strong operating leverage.

Liu’s report follows a July 14 call by Dale Lai and Derek Tan of DBS Group Research, who deemed the stock worth $1.06. On June 25, Michael Lim and Terence Lee of UBS initiated coverage of the stock with a target price of $1.18. All three houses were involved in the listing. The co-working operator was listed less than two months ago at 94 cents. Its share price promptly dropped to as low as 50 cents before ending July 15 at 70.5 cents.

With 50 centres across 10 cities, the flexible workspace platform delivered a strong operating performance in FY2025 ended Dec 31, 2025, with revenue increasing 12.5% y-o-y. Revenue growth was supported by a y-o-y 6.6-percentage-point (ppt) increase in occupancy, a 12.9% y-o-y rise in workstation capacity and 13.1% growth in memberships, notes Liu.

The group swung into a net profit of US$2.7 million ($3.5 million) in FY2025, while results from operating activities rose more than fourfold due to better utilisation. The way Liu sees it, the business demonstrated its scalability with cash ebitda “surging” 118.5% y-o-y to US$13.5 million.

Liu believes in JustCo’s growth prospects due to expanding pipeline visibility and improving operational efficiency. She forecasts workstation capacity to grow at a CAGR of about 19.5% from FY2025 to FY2028, which would support revenue CAGR of roughly 22%. Furthermore, with occupancy estimated to increase by three percentage points by FY2028, Maybank expects stronger operating leverage to support cash ebitda margin expansion from 9.4% in FY2025 to 14.1% in FY2028. As such, cash ebitda is expected to grow at a CAGR of 43% from FY2025 to FY2028.

Using a target EV/Cash ebitda multiple of 8.5 times for FY2027, she values the business at $1.02. This is a “modest” premium to the lower quartile of peers, reflecting JustCo’s “strong” FY2025 to FY2028 expected revenue and cash ebitda CAGR of 22% and 43%, balanced against execution risks and relatively limited operating scale.

Liu believes that JustCo’s growth potential is undervalued at the current 3.3 times EV/Cash ebitda with $151 million of net cash. — Lin Daoyi

Aoxin Q&M Dental Group

Price target:

UOB Kay Hian ‘buy’ 36 cents

Potential transfer increases visibility

UOB KayHian analyst Tang Kai Jie has maintained his “buy” recommendation on Aoxin Q&M Dental Group (SGX:1D4![]() ) following its application to transfer its listing status from Catalist to the Mainboard.

) following its application to transfer its listing status from Catalist to the Mainboard.

In his July 9 report, Tang noted that this marks an important milestone reflecting its stronger financial position and growing business maturity.

“The application follows three consecutive years of improvement in its underlying operating performance, with underlying profit before tax increasing from about RMB2.7 million in FY2023 to RMB7.7 million in FY2024 and RMB8.4 million [$1.6 million] in FY2025,” Tang states.

If approved, the analyst believes that Aoxin Q&M will see an enhancement to its corporate profile and increased visibility among a broader base of institutional and international investors.

Earlier this year, in addition to the proposed transfer of listing status, Aoxin Q&M announced its expansion into China through two agreements to acquire two separate dental groups in Central and Southern China.

Tang also pointed out that Aoxin Q&M’s unique acquisition model utilises the Sino-Foreign Equity Joint Ventures and strategic partnerships to scale up operations efficiently.

As such, he is maintaining his “buy” recommendation with an unchanged target price of 36 cents for Aoxin Q&M, representing a 44% upside. “Our target price is pegged to 52.5 times the FY2027 P/E ratio, which is 2.5 standard deviations above historical averages based on its parent company’s (Q&M Dental Group) P/E band. Our valuation peg aims to capture more potential upside from more acquisitions by Aoxin Q&M in the China dental market,” Tang concludes. — Teo Zheng Long

CNMC Goldmine Holdings

Price target:

Lim & Tan ‘buy’ $1.90

Recent weakness an opportunity

Lim and Tan Securities says CNMC Goldmine’s (SGX:5TP![]() ) recent price weakness offers an opportunity for investors to buy. Analyst Chan En Jie maintains the company’s “buy” rating and raises the target to $1.90 in his July 10 report, up from $1.53.

) recent price weakness offers an opportunity for investors to buy. Analyst Chan En Jie maintains the company’s “buy” rating and raises the target to $1.90 in his July 10 report, up from $1.53.

At the current valuation of around 6.6 times forward P/E and 5.1% dividend yield, CNMC is “attractive”, according to Chan. Presumably, a key factor for his optimism includes revenue contributions from the miner’s newly upgraded carbon-in-leach plant, which is boosting daily processing capacity by 60% to 800 tonnes of gold-bearing ore. Chan notes that the expansion has begun to bear fruit, boosting gold output by 45% to 26,039 ounces in FY2025, with the company expecting to see full-year contributions from increased capacity starting in 2026.

In addition, CNMC is boosting production by opening a second underground mining facility and will be constructing two new vertical underground mining infrastructure facilities at its Sokor mine in Kelantan, Malaysia. The total estimated cost is US$12 million ($15.5 million), and it will provide open access to deeper, higher-grade ores and enhance overall production quality once fully operational in 2027.

That said, he sounded a note of caution about potential delays to the second underground facility due to water accumulation issues at the supporting shaft of the underground mining project. He also notes that actual gold production depends on ore grade, which may fluctuate from period to period.

Beyond the mining facilities, a comparative advantage for mining companies such as CNMC is their operating leverage, given their relatively fixed cost base. With all-in costs of around US$1,500 per ounce of gold, these costs are “safely” below current gold prices, which exceed US$4,000 per ounce. This means CNMC is positioned to benefit more when gold prices rise and, conversely, to earn less when they drop.

Another potential headwind for CNMC is regulatory issues, with Chan pointing out that tax penalties and higher royalty rates potentially cast uncertainty over the counter. CNMC announced in December 2025 that it received a notice of additional assessment of US$7.2 million from the Inland Revenue Board of Malaysia for the period of FY2019–FY2024. The company strongly disagrees with the tax liability and intends to file an appeal and challenge the additional tax assessments.

The Kelantan State Land and Mines Office has also issued a circular stating that the royalty rate payable on minerals produced in Kelantan will be increased as of January. The royalty rate payable for gold was revised to 15% from 10%, and for silver to 12% from 10%. CNMC notes that it has not been served with an official publication in the gazette and intends to submit an appeal against the proposed increases in the royalty rate payable.

Lim and Tan expect CNMC to post “strong” results for 1HFY2026, supported by average gold prices of US$4,680 per ounce since the start of the year. The $1.90 target is based on valuations that blend a peer-average 9.5 times FY2026 P/E with a discounted cash flow analysis, using a weighted-average cost of capital of 12% and terminal growth of 0%. Backed by net cash of US$62.6 million, or 17% of market cap, Lim and Tan projects earnings growth of 31% and 8% for FY2026 and FY2027, respectively, translating into a 5.1% forward dividend yield based on a 34% payout ratio. — Lin Daoyi