Divesting White Sands; AEI at NEX

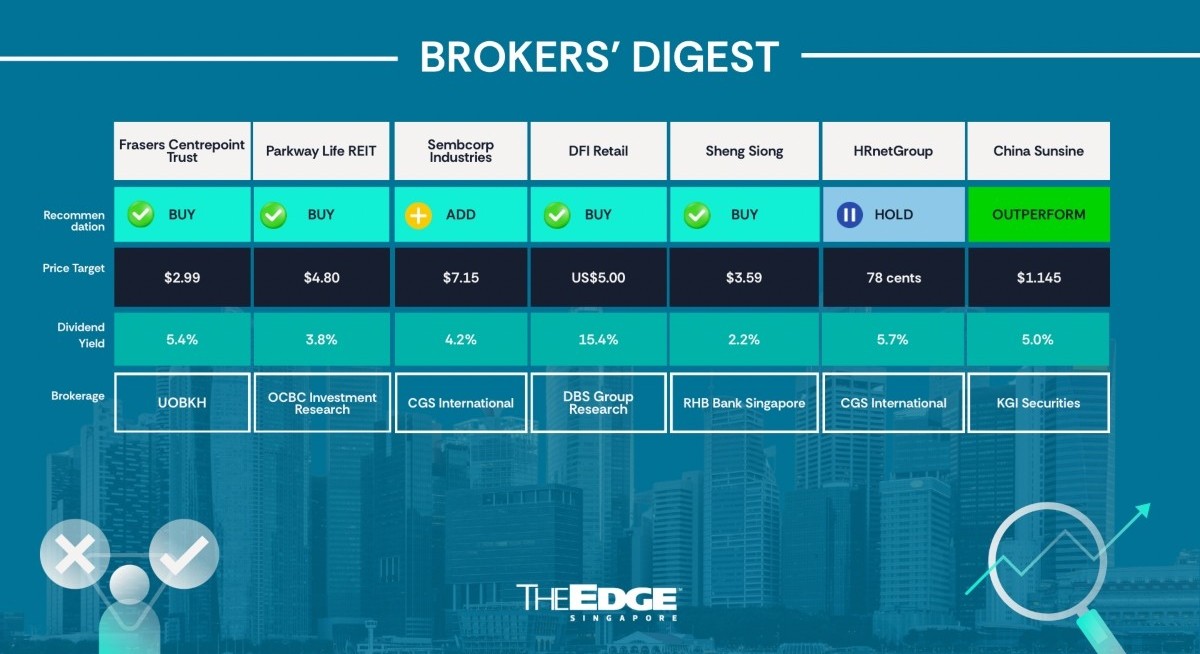

Jonathan Koh of UOB Kay Hian has maintained his “buy” call and $2.99 target price on Frasers Centrepoint Trust (FCT) (SGX:J69U![]() ) following the $467 million divestment of White Sands in Pasir Ris. At this level, the sale is at an 8.4% premium to valuation, with an estimated exit yield of 4.8%, allowing FCT to book a net gain of $32.4 million.

) following the $467 million divestment of White Sands in Pasir Ris. At this level, the sale is at an 8.4% premium to valuation, with an estimated exit yield of 4.8%, allowing FCT to book a net gain of $32.4 million.

“FCT is proactively recycling capital in order to enhance portfolio resilience and reposition for long-term growth,” says Koh.

Koh points out that although White Sands is not only the smallest mall in FCT’s portfolio, it faces competition from the newer Pasir Ris Mall. While fully occupied as of March, the REIT contributed just $11.1 million to net property income in 1HFY2026, or 6.9% of the total.

“The divestment strengthens FCT’s balance sheet with estimated net proceeds of $454 million earmarked for debt repayment,” says Koh. With the sale, FCT’s pro forma FY2025 DPU will be eroded by 1.9%, although this would be offset by a 0.7% net asset value gain as of September 2025, he adds.

The divestment will help lower pro forma aggregate leverage as of September 2025 from 40% to 36.5%, providing additional debt headroom to pursue acquisitions and asset enhancement initiatives (AEIs).

The sale will help streamline FCT’s retail portfolio to eight suburban malls with net leasable area (NLA) of 2.8 million sq ft, while maintaining its focus on necessity-driven retail, food & beverage and essential services.

See also: Keppel DC REIT is JP Morgan’s preferred data centre play in Singapore

Overall, FCT enjoyed strong leasing momentum in 1QFY2026 with healthy take-up of retail space led primarily by F&B operators. Leasing demand was also supported by fashion brands and lifestyle concepts, including art galleries. Prime suburban retail rents increased 1.4% y-o-y to $32.80 psf per month in 1Q2026.

“Singapore’s retail sector is expected to remain resilient, underpinned by improving tourism spending, a strong pipeline of Mice events, high-profile concerts, robust office worker footfall, Singapore’s status as a safe haven for capital, and limited new supply,” says Koh.

Citing CBRE, Koh says prime retail rent can maintain its upward trajectory with growth of 1%–2% in 2026.

On the other hand, he warns that the upcoming Rapid Transit System link, with launch on track for early 2027, could result in leakage of consumer spending.

Meanwhile, Causeway Point, the nearest FCT property to Johor Bahru, will have an AEI planned to turn it into a regional mall.

Koh, citing FCT’s management, says there will be new developments in the northern region to mitigate the negative impact of leakage in consumer spending caused by the RTS.

With new housing of some 50,000 units to be built in areas such as Chencharu, Sembawang North, Woodlands North and Kranji Racecourse, the residential population in the northern region is expected to increase 25%–27% over the next 10–15 years.

For more stories about where money flows, click here for Capital Section

Koh says that some 20,000 of these residential units are expected to come on stream in the next six to seven years, while Woodlands Regional Centre would create 100,000 jobs, with 100ha of land earmarked for future development.

An AEI is also underway over two years at another FCT mall, NEX, where carpark space will be converted into an NLA of 44,000 sq ft, increasing the total by 7%.

“Trade mix and rents would be optimised through remixing, resizing and reconfiguration. New office space would be added at level 4, which contributes to growth in shopper traffic,” says Koh. The AEI will cost FCT some $45 million and is expected to generate a 7% return on investment.

For now, Koh has trimmed his FY2027 DPU forecast by 2.5% due to the divestment of White Sands. — The Edge Singapore

Parkway Life REIT

Price target:

OCBC Group Research ‘add’ $4.80

Divestment of nursing home

Ada Lim of OCBC Group Research has maintained her “buy” call on Parkway Life REIT (PLife) (SGX:C2PU![]() ) but with a slightly trimmed fair value of $4.80 from $4.82.

) but with a slightly trimmed fair value of $4.80 from $4.82.

The REIT, which focuses on healthcare properties, announced on June 30 the divestment of a nursing home in Japan to its operator for $9.4 million. This is 38% higher than the asset’s original purchase price and 5% above the property’s latest valuation as at Dec 31, 2025.

The REIT expects to recognise a net gain on disposal of investment property of $600,000.

Net proceeds from the divestment of around $9.2 million will be used to further strengthen PLIFE’s balance sheet in the interim, pending deployment towards higher-growth opportunities.

The divestment is not expected to have a material impact on PLife’s FY26 distribution per unit (DPU), says Lim.

Aside from the divestment, the REIT is set to benefit from operational improvements following the completion of a multi-year refurbishment of its flagship hospital here, Mount Elizabeth.

Dubbed Project Renaissance, Lim calls the works a “strategic transformation rather than a surface-level refurbishment”, providing better flexibility and efficiency.

“Altogether, the visit gave us greater confidence that the performance of the Singapore hospitals may exceed minimum rent going forward, thereby allowing PLife to participate in revenue sharing,” she adds.

Lim, citing the REIT’s management, notes that Mount Elizabeth serves the most medical tourists among hospitals in Singapore, and that international revenue is disproportionately higher relative to volumes due to higher-intensity procedures being performed. The hospital is still in the ramp-up phase post-capex works, and this is expected to last roughly 24 months.

In her updated model, Lim has accounted for the divestment in Japan and trimmed her FY2026 DPU estimates by 0.2% and her FY2027 estimates by 0.3%, resulting in a slightly lower fair value of $4.80.

Based on the June 30 closing price of $4.05, Lim’s estimated FY2026 yield for the REIT is 4.4%, which is lower than most S-REITs. Even so, she is of the view that this yield is “reasonable” given the REIT’s track record and quality of management.

In future, Lim sees “multiple levers” the REIT can pull to grow its DPU. For example, Gleneagles could be another hospital here to be refurbished; Mount Elizabeth Novena may be acquired — although if so, it will be over several tranches given the asset’s size in the billions. The REIT can continue to recycle and optimise its portfolio in Japan and grow further in Europe. — The Edge Singapore

Sembcorp Industries

Price target:

CGS International ‘add’ $7.15

Softer renewable energy portfolio

Lim Siew Khee and Meghana Kande of CGS International have trimmed their target price for Sembcorp Industries (SGX:U96![]() ) to $7.15 from $7.68, on the expectation that 1HFY2026 earnings will be softer.

) to $7.15 from $7.68, on the expectation that 1HFY2026 earnings will be softer.

Specifically, Sembcorp will likely report lower performance in renewable energy (RE) in two of its key markets, India and China.

For one, in India, solar plant load factors declined in the first four months of the year, likely due to low resource availability and ongoing capacity additions. On the other hand, China continued to see elevated RE curtailment.

For context, China and India accounted for 47% and 38% of Sembcorp’s 20.3 gigawatt (GW) RE portfolio at end-FY2025, respectively, with around 4.2 GW scheduled to come online from FY2027 to FY2028.

“We believe the combination of these factors, along with Sembcorp’s limited planned RE capacity additions in 1HFY2026, likely led to weaker profitability for its RE segment,” state Lim and Kande, who have projected a 55% y-o-y drop in RE 1HFY2026 to $59 million.

Also, with weaker operations in the UK and lower spark spreads in Singapore, Sembcorp’s earnings from gas and related services will likely drop 17% y-o-y to $275 million.

For now, with the company’s 600 megawatt (MW) Sakra plant commencing operations in 4QFY2026, Lim and Kande are “still comfortable” with their FY2026 earnings forecast of $645 million for this segment, down 8% y-o-y.

All in, they have cut their FY2026 earnings by 6.5%, and their FY2027 and FY2028 earnings by 7% and 4%, respectively, to reflect a more cautious outlook for RE.

By applying the same FY2027 earnings multiple of 12 times, they have derived a lower target price of $7.15, a discount to the multiple of 16 times for faster-growing peers.

Given the headwinds from renewable energy, the CGSI analysts have removed Sembcorp from their list of top Singapore stock picks.

Nonetheless, they have maintained “add” given several key re-rating catalysts. The first of which is value-unlocking from Sembcorp’s India RE business IPO. This corporate action could materialise earlier than expected, late in the current FY2026 or early FY2027, thanks to improving valuations of Indian peers trading at 12 times FY2026 EV/Ebitda versus Sembcorp’s 10 times.

Also, Sembcorp may see another catalyst from stronger-than-expected earnings contribution from the Sakra plant and new power purchase agreements. For one, it could be a strong contender for incremental contracts from Micron, which is in the midst of a $30 billion capacity expansion here in Singapore.

On the other hand, downside risks include prolonged power plant shutdowns and unfavourable regulatory changes impacting operations. — The Edge Singapore

DFI Retail Group Holdings

Price target:

DBS Group Research ‘buy’ US$5

Acquisition of advertising platform

Chee Zheng Feng of DBS Group Research has kept his “buy” call and US$5 ($6.46) target price on DFI Retail Group Holdings (SGX:D01![]() ) after its US$3.8 million acquisition of Cody HK, a leading Hong Kong out-of-home advertising operator with assets spanning buses, taxis, trams and other outdoor media formats, from Australia-listed ARN Media (ARN).

) after its US$3.8 million acquisition of Cody HK, a leading Hong Kong out-of-home advertising operator with assets spanning buses, taxis, trams and other outdoor media formats, from Australia-listed ARN Media (ARN).

The acquisition strengthens DFI’s retail media platform by expanding its advertising reach beyond in-store and digital channels, supporting the growth of DFIQ Media and its broader omnichannel strategy.

Based on ARN’s FY25 disclosure, Cody HK reported negative net assets of US$17 million, largely due to significant provisions, compared with positive net assets of US$0.4 million in 1H2025.

The business also recorded a loss before tax of US$27 million in FY2025, compared with US$9 million in FY2024. Despite the reported losses, Cody HK remained slightly cash flow positive, generating net cash of approximately US$0.5 million.

Chee says that at first glance, the acquisition appears immaterial given its modest purchase price. Given the recent correction in DFI’s share price, Chee believes investor concerns could be centred on Cody HK’s reported US$27 million pre-tax loss, which, if it continues, could be a drag on DFI’s earnings momentum in the medium term.

Chee believes that the FY2025 losses were likely inflated by one-off expenses, given the substantially better FY2024 performance. Using FY2024’s US$9 million pre-tax loss as a more representative earnings base, Chee estimates the acquisition would result in a US$2 million drag on FY2026 earnings on a pro-rated basis, representing less than 1% of his FY2026 net profit forecast of US$293 million.

On a fully annualised basis, the impact would be around US7 million in FY2027, equivalent to roughly 2% of his FY2027 earnings forecast of US$316 million, which remains relatively immaterial. “More importantly, we view the acquisition as a strategic step in scaling DFI’s retail media business into a meaningful and potentially high-margin growth engine,” says Chee.

He points out that Cody’s extensive outdoor media network significantly expands DFI’s media footprint and complements its existing in-store and digital advertising assets.

According to Chee, retailers are generally willing to commit meaningful advertising budgets only when media platforms achieve sufficient scale, particularly in physical advertising formats.

“A broader network allows brands to achieve greater visibility and consumer reach, rather than being limited to smaller in-store screens.

Looking beyond the near-term earnings impact, Chee expects this acquisition to be a sensible move that strengthens DFI’s retail media proposition. However, building a scaled and highly profitable media platform will likely be a multiyear journey. — The Edge Singapore

Sheng Siong Group

Price target:

RHB Bank Singapore ‘buy’ $3.59

New stores drive earnings growth

Alfie Yeo of RHB Bank Singapore has maintained his “buy” call and raised his target price for Sheng Siong Group (SGX:OV8![]() ) from $3.45 to $3.59, on expectations that earnings are growing from contributions from newly opened stores.

) from $3.45 to $3.59, on expectations that earnings are growing from contributions from newly opened stores.

The supermarket chain operator opened 12 new stores in FY2025, and earnings from these new stores will manifest meaningfully in the current FY2026.

Also, with at least seven new stores to open this year, this will bode well for the coming FY2027 earnings.

To support the growing network of stores, Sheng Siong is conducting the ground-breaking for its new distribution centre later this month.

To be completed by late 2029, the centre will help support the company’s eventual target of 120 stores. As of 1QFY2026, the company runs 87 stores in Singapore.

Yeo figures that in the meantime, construction costs for the centre will peak in FY2027 and FY2028. “With store openings having exceeded our expectations, we raise FY2027 earnings by a marginal 2% to factor in a stronger store and revenue base going into FY2027,” he says.

Yeo notes that key downside risks to his earnings estimates include slower-than-expected store openings, lower sales demand and per-sq-ft traction, and the inability to maintain gross profit margin at current levels.

“However, we expect Sheng Siong’s performance to remain resilient, as it targets the mass market value segment, which will enjoy the effects of downtrading in a soft consumption environment.

“Risks related to El Niño are low as energy cost is a small component of its operating expenses, and its diversified sourcing network for substitute products and presence in alternative markets can help mitigate risks of higher input costs,” says Yeo. — The Edge Singapore

HRnetGroup

Price target:

CGS International ‘hold’ 78 cents

Subdued Singapore job market

Tan Jie Hui and Lim Siew Khee of CGS International have kept their “hold” call on HRnetGroup (SGX:CHZ![]() ) , along with the same target price of 78 cents, given how earnings growth should remain subdued for the employment agency amid a soft hiring environment.

) , along with the same target price of 78 cents, given how earnings growth should remain subdued for the employment agency amid a soft hiring environment.

Singapore’s job market has shown signs of cooling. According to the Ministry of Manpower, total employment growth in 1Q2026 is moderating, led by weaker non-resident hiring; the Ministry of Trade and Industry (MTI) has warned that the US–Israel–Iran conflict could weigh on activity ahead, layering geopolitical risk onto an already softening backdrop.

ManpowerGroup’s Singapore 3Q26 survey confirms the trend, with the seasonally adjusted net employment outlook set to fall both q-o-q and y-o-y, dragged by large organisations and the information sector, even as manufacturing, construction, real estate, and SMEs hold up better.

“We believe this domestic softness could be partly offset by resilience elsewhere in the region: China, Taiwan and Vietnam continue to post robust hiring intentions, according to ManpowerGroup’s APME survey,” state Tan and Lim.

Nonetheless, HRnet, according to the analysts, offers a “compelling” defensive dividend profile with a yield of between 5% and 6%.

The company maintains a cash moat of $336 million, comprising a $263 million net cash position plus short-term investments such as T-bills and gold, against working capital needs of $130 million per year.

From the perspective of Tan and Lim, capital returns remain a “clear management priority”, with payout ratios near 80% over the past two years and FY2025 dividends raised to 4.2 cents, up from four cents each paid in the previous four years.

“We believe this balance sheet strength matters more as Singapore’s hiring cycle softens: it underpins the resilient and largely recurring flexible staffing business and should let HRnetGroup continue to outpace peers on profit growth during challenging economic cycles.

“Cyclical softness in permanent recruitment may cap near-term growth, but the strong balance sheet and resilient earnings mix should provide meaningful downside protection, in our view,” add the analysts.

Given how Singapore, which contributes just over half of HRnetGroup’s gross profit, will remain “subdued”, the analysts have maintained their 14.5 times P/E valuation, which is in line with the company’s historical average between FY2017 and FY2025, thereby deriving the target price of 78 cents.

“That said, valuation will likely be supported by HRnetGroup’s strong net cash position, resilient flexible staffing franchise, and steady dividend profile,” add Tan and Lim, noting that it now trades at an “undemanding” ex-cash FY2027 P/E of nine times, offering downside support.

For them, upside risks include a rebound in executive hiring and strategic M&As. On the other hand, downside risks include weakening macroeconomic conditions that impact professional recruitment volumes and margins, as well as competition. — The Edge Singapore

China Sunsine Chemical Holdings

Price target:

KGI Securities ‘outperform’ $1.145

Mission-critical within tyre input chain

Chong Ting Shuo of KGI Securities has initiated coverage on China Sunsine Chemical Holdings (SGX:QES![]() ) with an “outperform” call and target price of $1.145.

) with an “outperform” call and target price of $1.145.

Chong describes China Sunsine as a company whose products are “embedded in a mission-critical tyre input chain”.

The company supplies accelerators, insoluble sulphur and anti-oxidants used in compounding and vulcanisation. Rubber chemicals account for a small share of tyre costs, but they affect cure speed, durability and production reliability; qualified suppliers therefore have stronger retention than a generic commodity label would imply, says Chong.

As the world’s largest rubber accelerator producer, Chong says the company can leverage this position to drive market share gains across industry cycles.

Chong expects capacity to rise to 272,000 tonnes in FY2026, up from 254,000 tonnes at end-FY2025, thereby supporting volume-led growth as weaker producers face utilisation, environmental and working-capital pressure.

For the coming FY2027 to FY2030, Chong expects the company to enjoy an uplift in its average selling price as margins normalise, which will keep the analyst’s earnings case “grounded”.

Chong values the company using a DCF methodology using 12% weighted average cost of capital and 2% terminal growth, thereby deriving a target price of $1.145.

Key downside risks include pressure on the average selling price of rubber chemicals and industry overcapacity; volatility in raw material and energy costs; weaker tyre demand or customer utilisation; expansion and utilisation execution risk; and, last but not least, forex and capital allocation risk. — The Edge Singapore