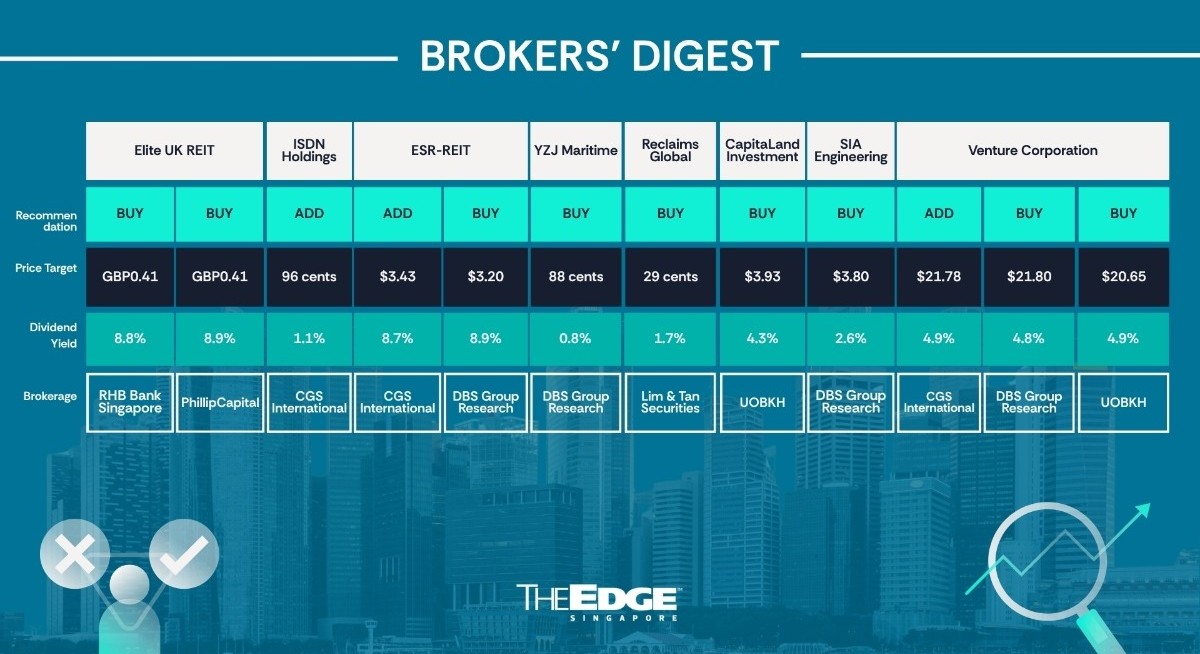

RHB Bank Singapore ‘buy’ GBP0.41

PhillipCapital ‘buy’ GBP0.41

Elite UK REIT kept at ‘buy’ on refinancing talks

RHB Bank Singapore and PhillipCapital are keeping their respective “buy” calls on Elite UK REIT (SGX:MXNU![]() ) following the recent 1QFY2026 business updates.

) following the recent 1QFY2026 business updates.

See also: Broker's Digest: Centurion Corp, Sembcorp, LHN, ThaiBev, Wee Hur, UI Boustead REIT, Lincotrade

In his April 27 report, RHB Bank Singapore’s Vijay Natarajan notes that Elite UK REIT is in talks to refinance its debt due for renewal next year, with plans to stagger loan maturities and reduce debt margins. “We expect interest costs to be relatively flat at current levels due to a slightly more hawkish inflationary outlook in the UK on the back of the Middle East war,” says Natarajan.

Meanwhile, the latest re-gearing exercise, which saw about 64% of the income-expiring leases in April 2028 extended by seven to 10 years, beats Natarajan’s expectations.

“This also reflects further valuation growth potential if Elite UK REIT secures lease extensions for the remaining 32% of leases, which are set to expire in April 2028. The valuation increase has also brought down net gearing to a comfortable 37.4% from 40.7% and an 13% increase in NAV to GBP0.45 per unit,” Natarajan adds.

See also: Maybank reiterates ‘buy’ call for Olam at unchanged $1.60

For the potential divestment of Peel Park, Natarajan mentions that Elite UK REIT’s management team has set a target to complete the divestment by the end of this year. “We expect such a sale to possibly net GBP20 million ($34.6 million) to GBP30 million in gains, further reducing Elite UK REIT’s gearing and providing debt headroom for accretive acquisitions,” the analyst predicts.

At the same time, the conversion of Lindsay House in Dundee into a 170-bed purpose-built student accommodation (PBSA) facility is on track, with targeted student intake slated for the 2027 academic year.

“Elite UK REIT expects yield-on-cost of around 7% on its GBP15 million to GBP17 million capex and ROI of about 20%. Plans are currently underway to convert Cambria House, Cardiff, into a 348-bed PBSA,” the analyst adds.

As such, Natarajan tweaks his distribution per unit (DPU) forecast for FY2026, FY2027 and FY2028 by 0%, –1% and +1%, respectively, factoring in divestments and lower vacancy costs. “Our target price of GBP0.41 includes a 0% ESG premium/discount, given Elite UK REIT’s 3.1 score is on par with the country median,” he concludes.

Meanwhile, in his April 27 report, PhillipCapital analyst Hashim Osman states that Elite UK REIT’s 1QFY2026 revenue and adjusted net property income rose 1.2% and 4%, respectively, to GBP9.4 million and GBP9.1 million, which represent 25% and 27% of his FY2026 forecast.

“Distributable income increased 9.8% y-o-y to GBP5.3 million. The increase was driven by positive rental reversions, contributions from three acquisitions (Priory Court, Custom House, Merlin House) in FY2025, and falling financing costs through debt repayment,” the analyst states. According to Hashim, Elite UK REIT’s borrowing costs are stable at 4.7%, with 92% of debt at fixed rates.

As such, he maintains a “buy” call with an unchanged dividend discount model-based target price of GBP0.41 for Elite UK REIT. His estimate of FY2026 DPU is GBP0.0306, reflecting lower rental income from assets that may not be re-geared with the UK’s Department for Work and Pensions (DWP).

For more stories about where money flows, click here for Capital Section

Approximately 20% of the remaining 30% of DWP’s leases are expected to be re-geared, with the remaining assets likely to be repositioned or divested. Elite UK REIT is trading at a 9.0% FY2026 dividend yield and a P/NAV of 0.87 times. — Teo Zheng Long

ISDN Holdings

Price target:

CGS International ‘add’ 96 cents

Resilient industrial automation business

William Tng of CGS International has more than doubled his target price for ISDN Holdings (SGX:I07![]() ) from 44 cents to 96 cents, on the premise that the company’s resilient industrial automation business will see further growth, therefore justifying a higher earnings multiple.

) from 44 cents to 96 cents, on the premise that the company’s resilient industrial automation business will see further growth, therefore justifying a higher earnings multiple.

In February, ISDN reported FY2025 revenue of $440 million, an 18% y-o-y increase, driven largely by its industrial automation business in China. Gross margin for this business segment was relatively stable at 24.3% in FY2025, up from 24.2% in FY2024.

Earnings for the year were $7 million, down 21% y-o-y, dragged down by $4.5 million in unrealised, non-cash foreign-exchange revaluation losses from its hydropower business in Indonesia. Excluding this, core profit for the year was up 26% y-o-y. Even so, ISDN wants to expand its renewable energy business, with two additional mini-hydropower plants scheduled for completion in 2026.

According to Tng, ISDN continues to see broad-based demand for its IA business as factories enhance their capabilities through advanced AI solutions. The company has also expanded its presence across Asia to capture emerging opportunities from Malaysia and Taiwan amid ongoing global supply chain diversification, he says.

Tng’s higher target price of 96 cents is based on 24 times FY2027 earnings, which is one standard deviation above its 10-year average from FY2017 to FY2026. His earlier target price was based on an earnings multiple of 13.5 times, the company’s 10-year average between FY2016 and FY2025. Besides earnings growth expected to resume from FY2026 to FY2028, Tng believes this counter will also attract buying interest from the Equity Market Development Programme (EQDP) funds.

Re-rating catalysts include higher-than-expected net profit contribution from its hydropower business segment, faster economic growth in China as it stimulates its economy, and a stronger global semiconductor recovery. On the other hand, downside risks include weak customer demand if the global economy continues to slow, and potential bad debts as economic conditions worsen. — The Edge Singapore

ESR-REIT

Price targets:

CGS International ‘add’ $3.43

DBS Group Research ‘buy’ $3.20

‘Resilient’ 1QFY2026

Analysts from DBS Group Research and CGS International have reiterated their bullish calls on ESR-REIT (SGX:9A4U![]() ) following a “resilient” 1QFY2026.

) following a “resilient” 1QFY2026.

For the quarter, gross revenue fell 0.4% y-o-y to $110.1 million, while net property income fell 2.3% y-o-y to $80.6 million.

The REIT secured positive rental reversions and paid lower funding costs. However, income was weighed down by higher operating costs and the divestment of a hotel that the REIT previously owned at Changi Business Park.

On a “same-store” basis, ESR-REIT’s revenue rose 1.4% y-o-y, helped by positive rental reversions and higher rents on new leases, while NPI was broadly flat at –0.1% y-o-y due to higher utilities and property taxes. Distributable income rose 1.4% y-o-y to $44.8 million, supported by lower borrowing and perpetual securities costs.

The REIT’s gearing was 44.3% but will be reduced to 39.5% on a pro forma basis after non-core divestments and debt repayments. Overall borrowing costs stayed fairly stable q-o-q at 3.34%.

Dale Lai of DBS Group Research calls 1QFY26 a “transition” quarter with operations remaining largely steady, but strategically more important for the balance sheet. He points out that the $439.1 million divestment of non-core assets should reduce leverage and improve land-lease quality, but the market will likely watch whether proceeds can be quickly recycled into asset enhancement initiatives (AEIs), redevelopments or acquisitions to protect DPU.

Down the road, the REIT’s AEI at 29 Tai Seng Street is 97% completed, with total completion by July; the redevelopment of 2 Fishery Port Road, to start in 4QFY2026, offers a potential 7.0% stabilised yield on cost, says Lai, who is keeping his “buy” call and $3.20 target price.

Separately, Li Jialin and Lock Mun Yee of CGS International note that the REIT is supported by its stable operations and stabilising core earnings. Citing the 8.7% FY2026 yield, they maintain their “add” call and target price of $3.43. Potential re-rating catalysts include accretive acquisitions and earlier completion of AEI and projects. On the other hand, downside risks include unexpected lease non-renewals, delay in AEI completion, and unfavourable exchange rates. — The Edge Singapore

Yangzijiang Maritime Development

Price target:

DBS Group Research ‘buy’ 88 cents

Fleet expansion enhances earnings visibility

Ho Pei Hwa of DBS Group Research has reiterated her “buy” call and 88-cent target price for Yangzijiang Maritime Development (SGX:8YZ![]() ) , following news that the company is expanding its fleet with a recent order.

) , following news that the company is expanding its fleet with a recent order.

On April 27, the company announced it had signed orders for 10 new eco-compliant vessels, including tankers and bulk carriers. The vessels, to be built by third-party Chinese yards, can run on methanol.

The vessels will be financed through a mix of equity co-investments and debt, in line with its established capital deployment framework. Deliveries of these vessels are scheduled from 2027 to 2029.

With this latest order, the company’s fleet will expand to 105 vessels, including 53 under construction. The latest order reinforces the group’s growth trajectory and enhances earnings visibility, says Ho, referring to the expanding fleet.

“The diversified vessel mix and eco-compliant designs position the fleet to capture charter demand amid tightening environmental regulations, while supporting premium asset values,” says Ho.

“The expansion aligns with Yangzijiang Maritime’s capital-cycling strategy, providing flexibility to monetise assets via chartering, leasing, or pre-delivery resale, sustaining returns and mitigating cyclicality across shipping markets,” she adds.

The company did not disclose the cost of the 10 new orders, but Ho estimates the total at around US$550 million ($700 million). Assuming an average of 85% stake and 40% equity, YZJ Maritime might need to pay around US$45 million per year in 2026–2029. Even so, net gearing should still be manageable at 0.1–0.2 times.

She estimates the company can realise potential earnings accretions of US$20 to US$30 million per year from charter income or divestment gains for these 10 vessels. If the vessels can be resold before delivery, that will be a key re-rating catalyst to watch, says Ho. — The Edge Singapore

Reclaims Global

Price target:

Lim & Tan Securities ‘buy’ 29 cents

Rising fuel costs, but industry prospects bright

Linus Loo and Chan En Jie of Lim & Tan Securities have maintained their “buy” call on Reclaims Global (SGX:NEX![]() ) following its FY2026 earnings, which largely met their expectations.

) following its FY2026 earnings, which largely met their expectations.

Revenue for the year was up 5% y-o-y to $46.5 million, driven by stronger market demand for its excavation services and logistics & leasing segments.

Net profit for FY2026 came in at $6.8 million, up 23% y-o-y, including a one-off gain of $0.7 million from the sale of its former headquarters.

The company plans to pay 0.5 cent per share in final and special dividends, bringing its FY2026 total to 1.25 cents per share, adjusted for a one-for-one bonus issue. This gives a payout ratio of 54% and an “attractive” 6.3% yield.

According to Loo and Chan in their April 30 note, Reclaims Global remains a beneficiary of the construction upcycle in Singapore over the next few years.

The company’s role is to transform a raw or occupied site into a “build-ready” foundation. “This is the unglamorous but critical period before a single brick is laid or a crane is erected,” state Loo and Chan.

Ongoing and upcoming major projects may include the $100 billion coastal protection works, which Reclaims Global could capture in the future.

As the company operates at the early stages of the construction process, it enjoys demand and secure cash flow at an earlier rather than later stage of these big projects, the analysts point out.

They also note that institutional interest in Reclaims Global has grown in recent months, with 63.2 million new and vendor shares transacted at a bonus-adjusted price between 19.5 cents and 20.5 cents.

However, amid a favourable industry outlook, Loo and Chan have trimmed their FY2027 earnings forecast by 3.9% to account for potential margin pressures.

This has led to a slightly lower target price of 29 cents from 30 cents, based on 12.2 times FY2027 earnings, the same valuation multiple as the industry average. — The Edge Singapore

CapitaLand Investment

Price target:

UOB Kay Hian ‘buy’ $3.93

China and lodging drag remains

Adrian Loh of UOB Kay Hian has kept his “buy” call on CapitaLand Investment (SGX:9CI![]() ) (CLI) but has lowered his target price from $4.05 to $3.93 to account for slightly lower real estate investment business (REIB) margins, due to the competitive leasing environment in China as well as mixed leasing conditions across CLI’s developed markets.

) (CLI) but has lowered his target price from $4.05 to $3.93 to account for slightly lower real estate investment business (REIB) margins, due to the competitive leasing environment in China as well as mixed leasing conditions across CLI’s developed markets.

In 1QFY2026, CLI’s fee-related revenue was up 10% y-o-y to $310 million, driven by 58% and 14% y-o-y growth in private funds management and listed funds management, respectively.

CLI’s real estate investment banking (REIB) revenue was down 14% y-o-y to $207 million, driven by the exit of its US corporate housing platform last August.

CLI’s management, according to Loh, is aiming for double-digit fee revenue growth in 2026 and single-digit operating earnings growth, with 2Q26 fundraising as the key risk, as the $4.9 billion raised in 2025 will be hard to beat in a volatile market.

According to Loh, Singapore remains CLI’s one bright spot, anchoring its conviction as fund deployment has been selectively paused globally, except in Singapore. Also, CLI’s lodging business and its China assets continue to weigh down overall results due to softer occupancy and rental revisions.

For one, CLI experienced negative rental reversion across its retail, office, logistics and industrial park assets in China. Of note was office occupancy, which was only 81% in 1QFY2026, while shopper traffic growth of 1.3% y-o-y was the weakest within CLI’s retail assets.

Loh points out that despite its strong share price performance over the past three months, CLI has been a major laggard in the Straits Times Index and relative to its comparable companies in the property or asset management sectors. One reason is that $22.9 billion of CLI’s $50 billion in private funds under management (FUM) is concentrated in China.

With the country’s property-sector headwinds showing no near- or medium-term signs of abating, this overhang will limit CLI’s re-rating potential, says Loh. “Thus, a Temasek-led re-rating-focused combination with Mapletree Investments could make it more compelling for all stakeholders involved,” he suggests. — The Edge Singapore

SIA Engineering

Price target:

DBS Group Research ‘buy’ $3.80

Favourable risk/reward ratio

DBS Group Research analyst Jason Sum has upgraded SIA Engineering Co (SGX:S59![]() ) (SIAEC) to “buy”, citing the stock’s value at this point.

) (SIAEC) to “buy”, citing the stock’s value at this point.

“After the 15% correction since our downgrade in January, valuations at –1 standard deviation (s.d.) and resilient aftermarket-driven earnings support a more favourable risk/reward,” he writes.

Sum had downgraded his call on SIAEC to “hold” on Jan 14 due to limited upside and “execution risks” in achieving profitability in its engine and components segment. Shares in SIAEC closed at $3.64 on Jan 14, compared with its last traded price of $3.13 as at Sum’s latest report dated April 30.

In his report, the analyst highlights several factors in SIAEC’s favour, including its technological edge and a strong captive business thanks to its link with Singapore Airlines (SIA). The airline contributes about 70%–80% to the group’s top line. The maintenance cycle of SIA’s fleet “strongly impacts” SIAEC’s core business, notes Sum.

“SIA’s strategy to maintain a young, technologically advanced fleet of aeroplanes provides SIAEC with opportunities to gain expertise in maintaining new aircraft types and win third-party maintenance contracts,” he adds.

SIAEC is also likely to enjoy long-term demand growth from its maintenance, repair and operations (MRO) business, given its partnerships with leading original equipment manufacturers (OEMs) such as GE, Rolls-Royce and P&W.

Over the next two years, the analyst estimates that the group’s core net profit will grow at a 13% CAGR, driven mainly by new engine and component capabilities. The growth is also likely to come from the ramp-up of SIAEC’s Subang base maintenance from 4QFY2025, as well as new MRO and line maintenance joint ventures (JVs) in Cambodia and Malaysia.

In addition, Sum believes the group should see improved momentum as IT and gestation costs taper, its engine and components segment turns profitable, and capacity expands at Singapore Aero Engine Services.

“Near-term operating indicators remain supportive, with steady traffic growth at Changi and continued strength in engine aftermarket,” says the analyst.

Finally, SIAEC, which has $485 million in net cash and enjoys “solid” cash generation, has the flexibility to either enhance shareholder returns, pursue selective mergers and acquisitions (M&As) and deepen its collaboration with Air India as it scales its in-house MRO capabilities.

Despite the upgrade, Sum has lowered his target price to $3.80 from $4, based on a lower P/E multiple of 21 times from 24 times previously. The lowered P/E peg reflects a sector-wide multiple compression, he says.

For FY2026 ended March 31, Sum estimates SIAEC’s revenue and net profit at $1.48 billion and $172.6 million, respectively. The group will announce its full-year results after trading hours on May 11. — Felicia Tan

Venture Corporation

Price targets:

CGS International ‘add’ $21.78

DBS Group Research ‘buy’ $21.80

UOB Kay Hian ‘buy’ $20.65

An important turnaround quarter

Analysts have become more bullish on Venture Corporation (SGX:V03![]() ) , as following three years of lower earnings, the manufacturing services provider has turned the trend with higher y-o-y 1QFY2026 earnings. For the three months ended March, Venture’s earnings increased by 0.7% y-o-y to $56.3 million, and revenue rose by 1.9% to $628.5 million.

) , as following three years of lower earnings, the manufacturing services provider has turned the trend with higher y-o-y 1QFY2026 earnings. For the three months ended March, Venture’s earnings increased by 0.7% y-o-y to $56.3 million, and revenue rose by 1.9% to $628.5 million.

Before the results announcement on May 5, William Tng of CGS International had on April 30 raised his target price to $21.78 from $17.04, citing 8% earnings growth from FY2026 to FY2028. Following the results, which slightly beat his expectations, Tng on May 5 reiterated his call and target price, based on 23 times FY2027 earnings.

Ling Lee Keng of DBS Group Research has upgraded her call from “hold” to “buy”, along with a higher target price of $21.80 from $17.90, as she expects growth momentum to pick up through the year. Her revised target price is based on 24 times FY2027 earnings, up from 21 times.

Venture’s so-called Portfolio B, which includes the test and measurement, semiconductor and data centre domains, enjoyed 11.2% y-o-y growth in revenue to $417 million and remains the company’s principal expansion pillar.

On the other hand, Portfolio A — comprising life science, medtech and lifestyle consumer — saw sales drop by 12.4% to $212 million. Even so, Ling expects recovery in the consumer lifestyle segment to emerge in the latter half of this year, thanks to new product introductions.

For Ling, 1QFY2026 marks an “important turnaround” and the company “remains an attractive value play, underpinned by a strong balance sheet with over $1 billion in net cash and zero debt”.

UOB Kay Hian’s John Cheong and Heidi Mo note that Venture managed to hold its net margin at 9%, indicating its focus on high-value-add solutions and cost discipline. They have similarly raised their target price to $20.65 from $18.64 to reflect “stronger conviction” in earnings visibility, the balance sheet, and upcoming growth drivers. This valuation is pegged to 23.7 times FY2027 earnings, 2.5 standard deviations above the long-term historical mean.

In the future, they see growth in business segments including data centre and life science, while Venture’s R&D programme will help capture new opportunities beyond product/system design and development. — Lin Daoyi