Volatile rupiah

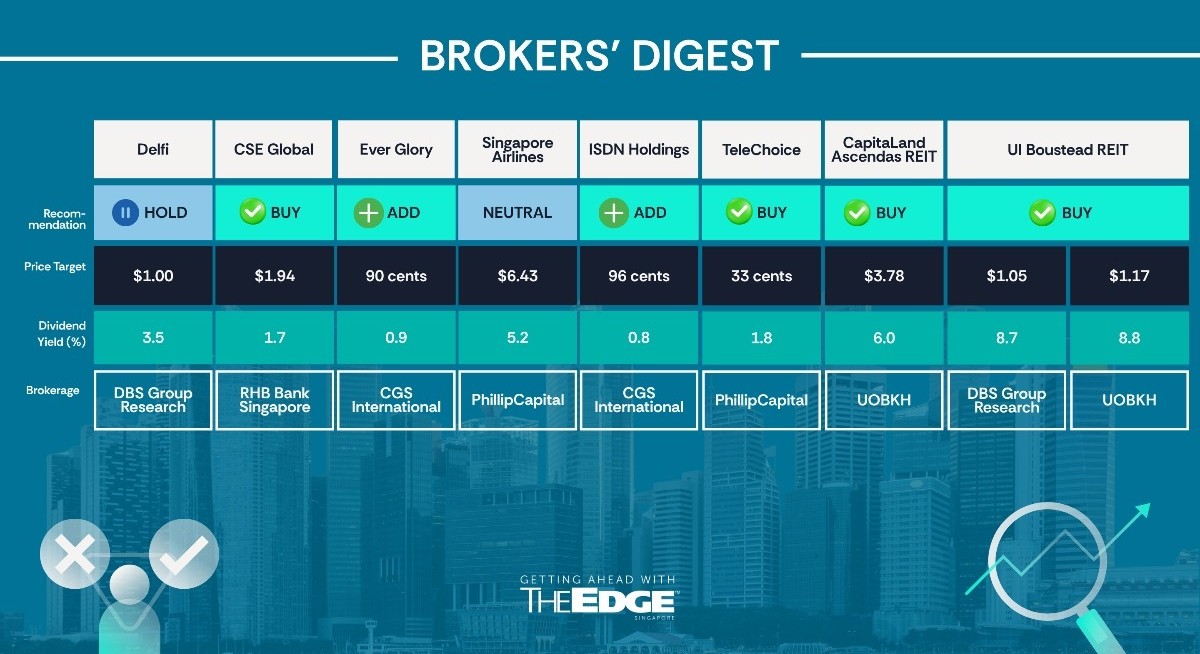

Chee Zheng Feng of DBS Group Research has maintained his “hold” call and $1 target price on Delfi (SGX:P34![]() ) following the chocolate maker’s 1QFY2026 update.

) following the chocolate maker’s 1QFY2026 update.

For the three months to March, Delfi reported 1QFY2026 net revenue of US$159 million ($203 million), up 6.2% y-o-y, driven by strong growth in Delfi’s proprietary brand segment, which was up 19.6%.

Thanks to the continued strength of core premium brands and deep retail relationships, Indonesia, the key market, posted the strongest growth with 20.5%, followed by Malaysia and the Philippines.

See also: CGSI maintains positive view on Ever Glory on order book wins

On the other hand, Delfi saw a decline in its agency brands segment after the “strategic” termination of a major account. Excluding this impact from 3QFY2025, the agency brands segment would have grown 30.4% y-o-y.

In the quarter, Delfi’s gross profit margin declined by 140 basis points y-o-y from 28% in 1QFY2025 to 26.6% in 1QFY2026, mainly due to a weaker rupiah and the absorption of higher cocoa costs from forward contracts.

As a result, Delfi’s 1QFY2026 ebitda eased slightly to US$16.8 million, down 0.8% y-o-y, reflecting lower gross profit and marginally higher operating costs. Despite this, Delfi maintains a strong balance sheet, with a net cash position of US$77 million.

See also: UBS lowers cost of equity and raises price targets for the local banks

Chee believes that, unlike a major competitor, Delfi has prioritised volume and market share growth by maintaining stable pricing, resulting in margin compression.

“We view this as a potential near-term positive, as increased market share could position Delfi to deliver a meaningful earnings uplift when lower cocoa prices start to flow through in the upcoming quarters,” he reasons.

Chee further notes that Delfi remains on track to deliver his flattish y-o-y FY2026 earnings forecast. “While lower cocoa costs could provide some uplift in the coming quarters, this could be largely offset by significant depreciation of the rupiah by more than 7% y-o-y as of mid-May, with no clear signs of stabilisation.”

“Accordingly, we prefer to remain on the sidelines and await clearer signs of an earnings turnaround before turning positive,” says Chee. — The Edge Singapore

CSE Global

Price target:

RHB Bank Singapore ‘buy’ $1.94

Multi-year data centre-led growth

For more stories about where money flows, click here for Capital Section

Alfie Yeo of RHB Bank Singapore, citing CSE Global’s (SGX:544![]() ) multi-year growth underpinned by US$1.5 billion ($1.9 billion) in orders from Amazon over the next five years, has raised his target price to $1.94 from $1.48.

) multi-year growth underpinned by US$1.5 billion ($1.9 billion) in orders from Amazon over the next five years, has raised his target price to $1.94 from $1.48.

At its recent 1QFY2026 business update, CSE Global reported revenue that was up 29% y-o-y to $265 million, which came in within Yeo’s expectations.

The strong driver came from its electrification segment, which was up 50% y-o-y to $146 million, with further growth ahead thanks to major data centre contracts in the Americas, which together account for $178 million in new order intake, which is two-thirds of the company’s total of $271 million. As at March 31, its order book was $716 million.

Revenue growth was also supported by the communications segment, which rose 19% y-o-y to $69 million, driven by contributions from Australia and New Zealand.

Yeo expects the company to book stronger revenue in the second half of the year as execution ramps up. “CSE continues to grow its electrification segment by strengthening its position in data centres through adding new industrial space, the purchase of new property, and the construction of buildings,” he says.

Yeo warns that start-up costs for new facilities are expected to impact profitability in the near term, leading to a weaker 1HFY2026. “However, we believe that this will be temporary, as a ramp-up in execution and revenue recognition can be expected from 2HFY2026,” he says.

Yeo has applied a higher valuation multiple of 26 times FY2027 to FY2028, up from 22 times FY2026, to be in line with the company’s international peers, resulting in a higher target price of $1.94.

“We believe CSE’s re-rating is a combination of the strong data centre outlook in the US, buoyed by stronger sentiment for artificial intelligence and cloud computing, as well as stronger anticipated fund flows into the Singapore market,” he says.

“We believe CSE’s recently announced strategic review could enhance shareholder value over the longer term,” he adds. — The Edge Singapore

Ever Glory United Holdings

Price target:

CGS International ‘add’ 90 cents

Closing in on the $1 bil mark

CGS International’s Then Wan Lin and Lim Siew Khee have maintained their bullish view on Ever Glory United Holdings (SGX:ZKX![]() ) following the company’s latest contract wins announcement, which brings the M&E contractor’s total order book closer to the landmark $1 billion level.

) following the company’s latest contract wins announcement, which brings the M&E contractor’s total order book closer to the landmark $1 billion level.

On May 18, the company announced it had won contracts worth $230 million from various clients, including the Land Transport Authority, to build a charging system for electric buses and to undertake mechanical and electrical works for a new hospital office building at Macalister Road and for the Tengah General Hospital. In addition, Ever Glory won a contract from Resorts World Sentosa. With that, its order book has reached $950 million.

In their May 20 note, the CGSI analysts estimate that earnings contribution from these contracts should be minimal in FY2026 and that meaningful earnings contribution would only materialise from FY2027 onwards.

Then and Lim note that several more projects are under evaluation as the tender applications closed just quite recently in the first quarter. They remain confident that Ever Glory will announce more order wins in 2HFY2026.

“Any successful bids would serve as potential re-rating catalysts for Ever Glory,” state Then and Lim, who have maintained their assumption that Ever Glory will win some $650 million worth of orders this year. They figure that every $150 million in incremental contract wins will increase their FY2027 earnings per share forecast by 4% to 6 cents.

Ever Glory recently completed a one-for-four bonus share issuance and while Then and Lim keep their “add” call, they have adjusted their target price to 90 cents from $1.13, which is still based on 15 times FY2027 earnings, which is 1.5 standard deviations above its historical three-year mean, in line with the average of regional peers.

“Our thesis remains intact, underpinned by Ever Glory’s more-than-$4 billion tender pipeline and 22% FY2025–FY2028 core EPS CAGR,” the analysts state. Downside risks include sharper cost escalation and delays in project awards or execution. — The Edge Singapore

Singapore Airlines

Price target:

PhillipCapital ‘neutral’ $6.43

Higher fuel costs

Hashim Osman of PhillipCapital has maintained his “neutral” call on Singapore Airlines (SIA) (SGX:C6L![]() ) , but citing volatile fuel costs, he has lowered his target price from $7 to $6.43.

) , but citing volatile fuel costs, he has lowered his target price from $7 to $6.43.

SIA, for its 2HFY2026, reported patmi that was down 53.6% y-o-y to $945 million, bringing full-year patmi to $1.18 billion, down 57.4%.

The bottom line was clearly weighed down by its associate, Air India, which accounted for $828.5 million in losses. Excluding this, SIA’s operating profit for 2HFY2026 was up 72% y-o-y to $1.57 billion, due to stronger passenger yield and traffic growth.

Issues at Air India will continue to impact. In April, after the full-year period ended in March, Pakistan’s closure of its airspace to Indian carriers has forced route diversions.

Also, the US-Iran conflict, which began in February, has largely affected Air India, given the Middle East’s importance as a transit hub for Indian aviation.

“Air India also operates without a fuel hedging programme, leaving it fully exposed to changes in jet fuel prices. Management has guided losses to remain elevated near term,” warns Hashim.

He notes that SIA’s carrying value of Air India associate is at around $1.1 billion as of March. “Once SIA’s investment in Air India is fully written down, Air India’s share of losses will no longer be recognised on SIA’s books. This would allow SIA’s underlying operational performance to reflect more in its earnings,” he says.

Meanwhile, in response to the US-Iran fighting, SIA has raised fares across its network. “However, it will not be sufficient to offset the rise in jet fuel prices and will function as a partial pass-through. With uncertainty about when the conflict will conclude, we expect margin compression from higher fuel costs once SIA’s cheaper hedges expire,” says Hashim.

He now values the stock using a P/B multiple of 1.1 times, down from 1.3 times, to reflect heightened sector risk following the US-Iran conflict, and is assuming higher fuel costs for FY2027 to account for cheaper hedges rolling off.

“SIA’s strong balance sheet and its special dividend policy through FY28 provide downside support,” he adds. — The Edge Singapore

ISDN Holdings

Price target:

CGS International ‘add’ 96 cents

Strong industrial automation demand

William Tng, the only analyst with active coverage on ISDN Holdings (SGX:I07![]() ) , has maintained a 96-cent target price, following 1QFY2026 earnings that were in line with his full-year projections. Given that Tng sees ISDN continuing to gain market share through its competitive strength across the full range of industrial automation technologies, he has kept his “add” call.

) , has maintained a 96-cent target price, following 1QFY2026 earnings that were in line with his full-year projections. Given that Tng sees ISDN continuing to gain market share through its competitive strength across the full range of industrial automation technologies, he has kept his “add” call.

In 1QFY2026 ended March, earnings surged 31 times y-o-y to $3.7 million, on the back of a 24.2% jump in revenue to $113.7 million, driven by its industrial automation segment. “The group saw strong demand in the form of semiconductors and industrial robots. ISDN is benefitting indirectly from the global growth in AI, data centres, semiconductors and energy storage, as it supplies a broad range of components and solutions to these sectors,” says Tng.

ISDN says its order intake will continue to grow in the current financial year, underpinned by strong demand for industrial automation. In addition, its renewable energy segment grew 39.3% y-o-y to $6.7 million in 1QFY2026, driven by construction income from its two new mini-hydropower plants in Indonesia, which are on track for completion this year.

However, three of its existing plants generated 39% lower revenue due to “highly unusual” weather variations. ISDN says that the weather has since “normalised” and fluctuations of such magnitude are not seen to recur.

Tng continues to value this counter at 24 times FY2027 earnings, which is 1 sd above its FY2017 to FY2026 average. He expects the company’s earnings growth to resume over FY2026 to FY2028 at a CAGR of 45.6%. “We think the stock could also attract buying interest from Equity Market Development Programme (EQDP) funds,” he says.

For Tng, re-rating catalysts include: a higher-than-expected earnings contribution from its hydropower business segment, a faster pace of economic growth in China as it stimulates its economy, and a stronger global semiconductor recovery.

On the other hand, downside risks include weak customer demand if the global economy continues to slow, and potential bad debts as economic conditions worsen. — The Edge Singapore

TeleChoice International

Price target:

PhillipCapital ‘buy’ 33 cents

Potential data centre venture upside

Paul Chew of PhillipCapital has maintained his “buy” call on TeleChoice International (SGX:T41![]() ) following its 1QFY2026 results, which were within expectations. Now, citing the recent re-rating of SGX-listed proxies in the systems integration sector, Chew has applied a higher valuation multiple, raising his target price to 33 cents from 27.5 cents. This marks his second price target increase in two months, following a March increase from 21.5 cents.

) following its 1QFY2026 results, which were within expectations. Now, citing the recent re-rating of SGX-listed proxies in the systems integration sector, Chew has applied a higher valuation multiple, raising his target price to 33 cents from 27.5 cents. This marks his second price target increase in two months, following a March increase from 21.5 cents.

For its 1QFY2026, TeleChoice reported profit before tax of $2.3 million, an increase of 78% y-o-y, driven mainly by a big jump in its business of managing logistics of mobile devices on behalf of its key customer in Malaysia, U-Mobile, which won over more subscribers, leading to a bigger volume of mobile devices in demand. However, in Singapore, TeleChoice’s mobile retail business incurred losses due to longer replacement cycles.

On the other hand, TeleChoice’s other business segment, ICT, is barely profitable in the quarter with profit before tax of just $60,000, up just $10,000 from the year-earlier 1QFY2025.

The company is focused on the rollout of digital infrastructure, namely, storage solutions, and plans to move toward AI solutions. “The sales cycle is longer for such projects,” says Chew.

This current year, the mobile devices segment is seen to remain the main growth driver. TeleChoice’s contract with U-Mobile has been extended for another year and Chew expects further extension upon further negotiations. The company has another business segment in network installation, and Chew notes that its entry into installing coolant systems for data centres in Indonesia is another area of growth.

In what might be another significant growth driver, TeleChoice announced in March that it was participating in a tender to design and build a data centre project in Malaysia. The tender results will be known within months. “Award of the Malaysia design-and-build data centre project will provide Telechoice with a significant pivot into a new, faster-growth segment,” says Chew.

For now, he has kept his FY2026 earnings estimates but raised his valuation multiple from 15 times to 18 times FY2026 earnings, in line with the recent re-rating of SGX-listed proxies in the systems integration sector.

Chew expects stable growth for the mobile devices segment but warns that a weak rupiah will weigh on growth for the network engineering segment, while the ICT segment is still seeking new growth verticals amid a competitive environment. Another positive aspect is that Chew observes that Telechoice has been undertaking share buybacks at up to 26.38 cents. — The Edge Singapore

CapitaLand Ascendas REIT

Price target:

UOB Kay Hian ‘buy’ $3.78

Higher DPU with three acquisitions

Jonathan Koh of UOB Kay Hian has maintained his “buy” call on Capitaland Ascendas REIT (CLAR) (SGX:A17U![]() ) along with a slightly higher target price of $3.78 from $3.70 after the REIT’s recent acquisition of three assets for $1.4 billion in total that will lift its DPU by 1.7% for this coming FY2027 and 2.3% for FY2028, with NAV per unit seen to increase by 3.1% to $2.36.

) along with a slightly higher target price of $3.78 from $3.70 after the REIT’s recent acquisition of three assets for $1.4 billion in total that will lift its DPU by 1.7% for this coming FY2027 and 2.3% for FY2028, with NAV per unit seen to increase by 3.1% to $2.36.

First, CLAR is buying 25 Loyang Crescent for $504 million, a modern four-storey ramp-up logistics facility comprising 13 standalone industrial buildings. This property, just a 15-minute drive from Changi Airport, will be leased back to Toll Offshore Petroleum Services under a triple-net lease with a weighted-average lease expiry (WALE) of 13.4 years and a built-in annual rent escalation of 2.5%. This property has a current plot ratio of 0.52, below the maximum 1.0, suggesting redevelopment potential of up to 1.6 million sq ft.

Next, CLAR is investing $245 million for a 50% stake in Ascent, which will give CLAR greater exposure to the Singapore Science Park precinct and add tenants such as Dyson and Merck.

Lastly, CLAR is taking a 49% interest in a 40.5MW Tier III hyperscale data centre in Greater Osaka for $621 million.

These acquisitions will nudge CLAR’s aggregate leverage higher by 0.7 percentage points to 39.7%. These three properties, taken together with six earlier additions, will result in total DPU accretion of 4.1%.

To fund the latest acquisitions, CLAR has issued 249.4 million new units at $2.406 each and 129.1 million new units via a preferential offering at $2.35 each.

Citing the management, Koh says CLAR plans to recycle assets in Singapore and reposition toward technology, logistics and biomedical science. It will pursue redevelopment and asset enhancement initiatives (AEI) locally.

Demand for logistics properties in Australia has softened, with recent completions giving tenants more choices and extending decision timelines. CLAR intends to expand its logistics presence in the US. Occupancy in US business parks could decline due to the entrenched work-from-home culture.

For Koh, possible share price catalysts for CLAR include resilient growth across the business parks, hi-tech buildings, life sciences, logistics and data centre segments, as well as contributions from development projects, redevelopment projects and AEIs. — The Edge Singapore

UI Boustead REIT

Price targets:

DBS Group Research ‘buy’ $1.05

UOB Kay Hian ‘buy’ $1.17

Another development project

Dale Lai of DBS Group Research has maintained his “buy” call and $1.05 target price on UI Boustead REIT (SGX:UIBU![]() ) after news that it is taking a 51% stake in a $104 million build-to-suit aerospace facility in conjunction with Boustead Singapore.

) after news that it is taking a 51% stake in a $104 million build-to-suit aerospace facility in conjunction with Boustead Singapore.

The facility, to be sited within the Seletar Aerospace Park, is backed by a long 22.5-year master lease with an unnamed global aerospace tenant and will be at an attractive 8.6% yield-on-cost.

The deal will improve UIB REIT’s portfolio weighted average lease expiry (WALE) from 5.8 years to 6.4 years. Furthermore, the structure of this deal is such that the REIT, which was listed only in March, can choose to fully own this asset over time, thereby providing an additional medium-term acquisition pipeline, says Lai. DPU accretion, meanwhile, is estimated at 2.5%-2.9%, assuming a debt-funded strategy.

“Strategically, the acquisition deepens UIB REIT’s exposure towards specialised aerospace and high-spec industrial assets with higher barriers to entry, while showcasing the sponsor’s ability to originate proprietary development opportunities,” says Lai.

“We view the transaction positively as it demonstrates UIB REIT’s continued ability to originate proprietary build-to-suit opportunities alongside supportive sponsors, allowing the REIT to capture positive spreads from development of around 8.6% vs 7.4% portfolio yield for Singapore — securing long-term income streams,” says Lai.

“The transaction also reinforces management’s strategy of increasing exposure towards specialised industrial segments with higher barriers to entry and stronger tenant stickiness,” he adds. “With this development, we see an improvement in portfolio quality, driving a re-rating over time,” says Lai.

Separately, Jonathan Koh of UOB Kay Hian notes that this aerospace park development and UIB Konan Phase 3, which was announced earlier, will begin contributions from 1QFY2028 and 1QFY2028, respectively.

Koh estimates that these two development projects will contribute earnings of $3.4 million in FY2029 and has therefore raised his DPU forecast by 3% to 7.3 cents for FY2029.

Koh has maintained his “buy” call and raised his target price for this counter to $1.17, up from $1.13. — The Edge Singapore