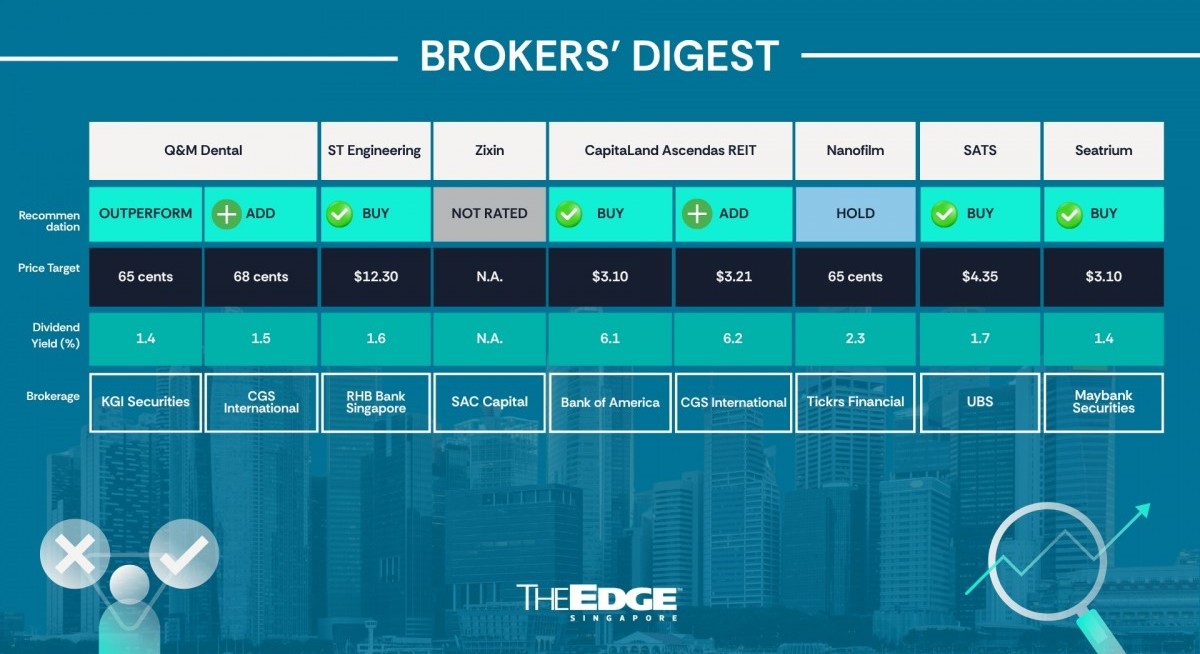

Bank of America ‘buy’ $3.10

CGS International ‘add’ $3.21

Accretive acquisition at $1.4 bil

Analysts are remaining positive on CapitaLand Ascendas REIT (CLAR) following its $1.4 billion plan to acquire three assets — including a data centre in Japan — which is expected to be accretive to its distribution per unit. To help fund the acquisition, CLAR will raise about $900 million from other investors and existing shareholders.

See also: Broker's Digest: OUE REIT, HPH Trust, JustCo, CapitaLand Investment, Addvalue, CICT

“Overall, we like this acquisition and see several positives from this move,” state Bank of America (BofA) analysts Donald Chua and Kylie Wan. First, these assets have occupancy rates between 90% and 100% and rent escalations of 1% to 2.5%. Tenants are mostly multinational corporations with “solid” credit profiles, such as Toll Offshore Petroleum Services, J&J, Dyson and Merck.

Also, the acquisitions will increase the share of data centres in CLAR’s portfolio to 13%. The Osaka data centre, to be bought from Mitsui, was completed in 2023, is deemed efficient, and has a built-in rent escalation of 1%.

Meanwhile, CLAR’s Singapore-based assets remain the clear majority, at 66% of the REIT’s AUM. “We think this move will sit well with investors,” state Chua and Wan.

See also: Citing defensive yield, Beansprout initiates coverage on United Hampshire US REIT

The analysts note that these deals will be accretive to CLAR’s distribution per unit (DPU), with pro forma accretion of 2.1% — a level that will rise to 4.2% if an earlier round of acquisitions and future acquisitions are taken into account. On the other hand, pro forma gearing remains “healthy” at about 40%.

In addition, there’s growth potential. Specifically, the Osaka data centre has a power capacity of 40.5 megawatts (MW), with a potential expansion capacity of 5.4MW, possibly by 2030, thereby increasing rental income then. “We see more potential partnerships in the future between CLAR and the vendor, Mitsui, with the latter said to have more data centre developments in the pipeline,” state Chua and Wan, who kept their “buy” call and $3.10 target price.

“We see sustained positive reversions, and uplift from acquisitions and asset enhancements to drive a DPU CAGR of +3.3% in FY2025 to FY2027,” state Chua and Wan, perceive the valuation “attractive at 1.1 times P/NAV, which is below its mean, and also FY2026 DPU yield of more than 6.1%.

Lock Mun Yee and Li Jialin of CGS International (CGSI) have also kept their “add” rating, but set a more bullish target price of $3.21. “We continue to like CLAR for its diversified and resilient portfolio.”

For them, potential re-rating catalysts for this REIT include completion of ongoing asset enhancement initiatives or redevelopment projects, which should boost contributions when completed between 1HFY2026 and 2HFY2028, as well as accretive new acquisitions.

On the other hand, downside risks include a protracted economic downturn that could adversely affect its ability to price rents to achieve positive reversions.

Based on their existing forecasts, BofA and CGSI estimate the FY2026 dividend yield for CLAR at 6.08% and 6.23%, respectively. — The Edge Singapore

For more stories about where money flows, click here for Capital Section

Nanofilm Technologies International

Price target:

Tickrs Financial ‘hold’ 65 cents

Re-rating story not over

Jaimes Chao of Tickrs Financial Singapore has downgraded his call on Nanofilm Technologies International from “buy” to “hold,” and lowered his target price from 75 cents to 65 cents.

In his March 26 note, Chao notes that the company, which provides coating services for consumer electronics and other products, has delivered a “solid operational performance” for its most recent FY2025, with adjusted ebitda up 21.3% to $62.8 million on the back of $244.6 million in revenue, an increase of 19.7% y-o-y, “modestly” ahead of his estimates.

However, patmi of $11.8 million, while up 52.4% y-o-y, was short of Chao’s estimates, no thanks to higher-than-expected write-off and depreciation as the company moved into a new capex cycle.

Nonetheless, Chao is pleasantly surprised by the final dividend of 0.87 cents, bringing FY2025’s total to 1.2 cents, an 81.8% y-o-y increase over FY2024’s total of 0.66 cents.

“This decisive uplift in shareholder returns signals that management views the earnings recovery as durable and is confident that the concluded major capex cycle will translate into materially stronger free cash flow from FY2026 onwards,” he says.

However, to reflect the earnings miss and a more “cautious” near-term earnings trajectory, even though structural growth remains intact, Chao has lowered his projections.

Even so, he is of the view that valuation remains undemanding at 0.86 times P/B and 6.1 times EV/Ebitda — a discount to the peer median and the company’s own historical low — and that the forward dividend yield, estimated at 2.3%, provides partial downside support.

For Chao, the path to re-upgrading this stock to “buy” runs through consistent EPS delivery against FY2026 expectations, Sydrogen’s first material commercial orders, and confirmation that the capex cycle reduction is translating into the projected free cash flow improvement.

“Nanofilm remains a compelling advanced materials platform — diversified, technologically differentiated, financially sound, and strategically positioned across multiple secular growth themes including automotive electrification, clean energy, and precision optics. “The re-rating story is not over; it is simply proceeding at a measured pace, one earnings cycle at a time,” says Chao. — The Edge Singapore

Sats

Price target:

UBS ‘buy’ $4.35

Resilient cargo network; upside from expanded food production volume

UBS has kept its “buy” call on Sats, but raised its target price from $3.85 to $4.35, citing a view that its global air cargo network business will remain resilient amid economic and trade uncertainties.

“While near-term macro and geopolitical uncertainties persist, we believe Sats’ diversified footprint provides an effective buffer against trade flow disruptions, allowing volumes to be rerouted across regions, even as airspace and supply chains adjust,” state analysts Melissa Leong and Rachel Tan.

The Middle East conflict is seen to have limited impact, given that Sats’ direct exposure is capped at 2%–3%, although the analysts acknowledge that indirect effects are harder to quantify.

Europe, Middle East and Asia routes, the market segment bearing the exposure, accounts for around 40% of the company’s cargo volumes and UBS estimates that every 1% decline will reduce the company’s patmi by 2%.

“Over the medium to long term, we think scaling specialised cargo handling should support margin expansion,” state Leong and Tan, referring to offerings such as temperature controlled handling,” state Leong and Tan.

There’s another reason to be bullish about Sats — the company’s much-expanded central kitchen space in Thailand, which can not just drive revenue growth but do so more efficiently. Due for completion soon, production capacity will increase five times to 108,000 meals daily.

“We believe higher utilisation and a shift to lower-cost fresh frozen meals should deliver cost savings versus Singapore operations, supporting earnings via operating leverage and reduced wastage,” suggest Leong and Tan.

They are projecting overall food-related revenue to increase by 6% in the current FY2026, 6% in the following FY2027, and 10% in FY2028, reaching $1.7 billion.

With a projected payout ratio of 30%, Sats is expected to yield 1.7% in FY2026. Their new target price of $4.35 is based on a one-year forward P/E of 20 times. — The Edge Singapore

Seatrium

Price target:

Maybank Securities ‘buy’ $3.10

Structural demand tailwinds for energy

As the Middle East conflict drags on and affects global oil and gas supply, reports have emerged of nations implementing measures to curb energy use, including work-from-home mandates and curtailments of aviation activity. Amid fuel shortages, countries are increasingly focusing on securing reliable energy supplies.

In times of crisis, there is also opportunity. In this vein, Maybank has initiated coverage of global offshore and marine player Seatrium with a “buy” rating and a target price of $3.10, a 38% premium to the counter’s March 26 closing price of $2.29.

In his March 27 initiation report, Maybank analyst Hussaini Saifee expects structural demand tailwinds and strengthening margins to support Seatrium’s earnings per share, which he expects to grow at a 27% compound annual rate from FY2025 to FY2028.

At the heart of his investment thesis are sustained geopolitical tensions and conflict, which reinforce energy security and supply diversification through new fossil fuel sources and renewable energy.

Observing that with breakeven prices of US$37 to US$43 ($47 to $55) per barrel, offshore is one of the lowest-cost sources of new oil supply. As such, he expects this to drive demand for the production of newbuild floating production, storage, and offloading (FPSO) vessels and cites industry estimates of a 40–50 FPSO pipeline up to 2030.

For offshore wind, for which Seatrium has won a contract recently, Hussaini believes the sector will grow at a CAGR of around 15% up to 2035.

Noting that Seatrium has an order pipeline of more than $32 billion, Hussaini projects that the Mainboard-listed company will secure $10-11 billion in contracts over the next three years. The way he sees it, profit margins are at an “upcycle” as the company pursues higher-margin projects and achieves operational efficiencies.

In his report, Hussaini forecasts that Seatrium will earn gross margins of 9%–11% from FY2026 to FY2028, up from 7.4% in FY2025. The stronger margins will be supported by a “cleaner execution base”, with low-margin non-FPSO legacy work accounting for less than 1% of the order book, or $220 million. In comparison, 95% of the backlog comprises repeatable series-build projects.

He also points out that Seatrium is pivoting from lower-value repair work to higher-margin conversions, with a $2 billion pipeline in floating, storage and regasification units, floating storage units, and powerships.

From the cost control perspective, Hussaini believes cost tailwinds “remain meaningful”, pointing out that Seatrium has achieved more than $150 million in annualised cost savings post-combination of Sembcorp Marine and Keppel Offshore and Marine as well as more than $200 million of divestments targeted by FY2028. The company has also decreased debt with net leverage at 0.8 times.

Based on the discounted cash flow model, Maybank values Seatrium at $3.10 per share, using an 8.4% weighted average cost of capital and 1% terminal growth. — Lin Daoyi

Q&M Dental Group

Price targets:

KGI Securities ‘outperform’ 65 cents

CGS International ‘add’ 68 cents

On the M&A path

Both KGI Securities and CGS International are keeping their respective “outperform” and “add” calls on Q&M Dental Group following its recent FY2025 results and updates on its M&A progress.

In a March 20 report, Chong Ting Shuo of KGI Securities says that the recent $130 million note issuance at 3.95% will help Q&M raise a larger cash balance and expand its capacity for organic rollout and tuck-in M&A, but will also increase the hurdle for capital deployment.

On the result front, Chong sees Q&M’s reported profit for FY2025 was mainly distorted by “accounting noise”. “FY2025 patmi fell 35% y-o-y to $9.3 million, but this mainly reflected consolidation-related losses and financing-related charges. Profit excluding other gains/losses and Medium-Term Note and Performance Share Plan expenses was broadly flat at $17.0 million,” Chong says.

On the M&A front, Chong says that Q&M’s regional pipelines are now more concrete given active M&A progress across Australia, Thailand, Singapore and China.

“The proposed Australian platform alone would add more than 40 clinics and 120 dentists, while the broader pipeline suggests FY2026 could mark the start of a more visible regional build-out,” says Chong.

As such, Chong is reiterating “outperform” and raises Q&M’s 12-month target price to 65 cents. He is keeping terminal growth at 2% while raising the weighted average cost of capital to 8% from 6%, reflecting a more conservative cost-of-capital framework around deployment risk and terminal-value sensitivity.

On the other hand, Tay Wee Kuang of CGS International, in his March 13 report, believes that the potential M&A is a significant milestone for Q&M, as it allows the dental group to expand into two new geographies (Australia and Thailand).

“In addition, the acquirers have provided Q&M with a profit guarantee of five to eight years, with key personnel of the various MOUs entering a 15-year service agreement with Q&M that we believe paves the way for sustainability of earnings growth upon completion of the acquisitions,” Tay adds.

Meanwhile, the analyst notes that, given the non-binding nature of the MOU, Q&M’s due diligence on the acquirers and uncertainty about the potential completion dates of the respective acquisitions, he has not reflected the potential EPS impact in his forecasts.

“However, we reduce our FY2026 and FY2027 EPS by 34.9% and 39.7% respectively due to recurring higher finance costs from Q&M’s $130 million MTN issuance last July to support its M&A plans,” says Tay.

Hence, Tay is reiterating his “add” call on Q&M, with a higher target price of 68 cents, reflecting a 126.7% premium over his FY2027 P/E target of 20 times, given the potential impact of its M&A plans. — Teo Zheng Long

Singapore Technologies Engineering

Price target:

RHB Bank Singapore ‘buy’ $12.30

Deserves further re-rating

Shekhar Jaiswal of RHB Bank Singapore has joined the wave of analysts upgrading their target prices for Singapore Technologies Engineering (ST Engineering), with expectations that this counter, poised for steady earnings growth, deserves further re-rating to be in line with regional defence peers.

In his March 25 note, Jaiswal maintains his “buy” call and raises the target price to $12.30 from $11.70.

“ST Engineering’s near-term catalysts include sizeable international defence awards, commercial aerospace capacity ramp-up translating into margin expansion, and clearer strategic direction for Satcom,” says Jaiswal, noting that the company has built up an order book of $33.2 billion.

“As international defence scales, we believe it merits a re-rating towards regional defence players vs a Singapore industrial holding,” he adds.

ST Engineering is winning new businesses in other key segments outside of defence and public security as well.

Recently, EFW, ST Engineering’s freighter-conversion joint venture with Airbus, has secured an A330-300 passenger-to-freighter contract from Hong Kong-based APAL, which is betting on rising China cargo-market demand.

“The news reinforces STE’s aerospace adjacencies and China cargo exposure. We view the impact on ST Engineering as strategically positive, enhancing workload visibility and franchise strength. However, near-term earnings contribution should be modest given the single-aircraft scope,” says Jaiswal.

In Singapore, ST Engineering, under a government contract, is rolling out a next-generation intelligent transport system to improve traffic control.

Its US-based unit, TransCore, has successfully deployed the dynamic tolling system for Kansas’ first express lane facility, with a seven-year base maintenance and image-review contract.

“Both announcements reinforce ST Engineering’s credentials in software-led, mission-critical road infrastructure. We view these as building stronger franchise credibility, better Smart City order book quality and greater visibility of longer-tail recurring service revenues,” says Jaiswal.

To reflect the orders and earnings momentum, he has raised his FY2026 earnings estimates by 2.5% and his FY2028 estimates by 7.2%, reflecting stronger medium-term execution assumptions.

Jaiswal notes that even with this upgrade, his forecasts remain conservative relative to those of other analysts. — The Edge Singapore

Zixin Group

Price target:

SAC Capital ‘unrated’

Circular economy prospects

SAC Capital has issued a non-rated report on Zixin Group, touting its “circular economy” business model that can help insulate the sweet potato-based foodstuffs company from the intense price wars plaguing downstream Chinese retail competitors.

Besides its home base in Liancheng County, Fujian, the company is setting up a similar sweet potato cultivation and processing ecosystem in Hainan, which has a landmass five times larger.

With the initial phases of land preparation already completed across multiple villages, this Hainan project is anticipated to begin contributing substantially to Zixin’s bottom line by FY2027 ending March 2027 and to double the company’s overall profitability eventually, state SAC analysts Matthias Chan and Liu Maorong.

In addition, Zixin has established a trading entity located within the Hainan Free Trade Port. By doing so, Zixin can tap into highly advantageous” zero-tariff policies, significantly reducing tax liabilities on the import of raw materials and the export of processed goods. Given that sales have been largely domestic thus far, Zixin is actively expanding into new markets such as Indonesia and the US.

Meanwhile, at its home base in Liancheng, the company is prepping the first phase of its new 86,000-sqm high-tech manufacturing facility, which can eventually increase processing capacity by 2.6 times, to 35,000 tonnes per year.

This capacity is specifically dedicated to the production of advanced functional ingredients, not lower-value sweet potato-based snacks. “By targeting the lucrative, high-barrier business-to-business (B2B) functional food, bakery, and nutraceutical markets, Zixin is structurally elevating its gross profit margins far beyond the natural limitations of the competitive traditional consumer snack food sector,” note Chan and Liu.

Zixin has been developing an animal feedstock business that uses sweet potato skins and other food-processing by-products. This means Zixin can build a circular economy. This means Zixin can build a circular economy.

It has secured key supply agreements and is well-positioned to secure additional orders for the animal feed. In its most recent FY2026, earnings jumped 105.5% y-o-y to RMB16.1 million ($3 million) in 1HFY2026 ended Sept 30, 2025, on the back of a 40.8% gain in revenue to RMB220.6 million.

As a rough gauge, Chan and Liu note that Zixin is trading at a P/E of 5.3 times. In contrast, the mean valuation of the Catalist board is 15.8 times. — The Edge Singapore