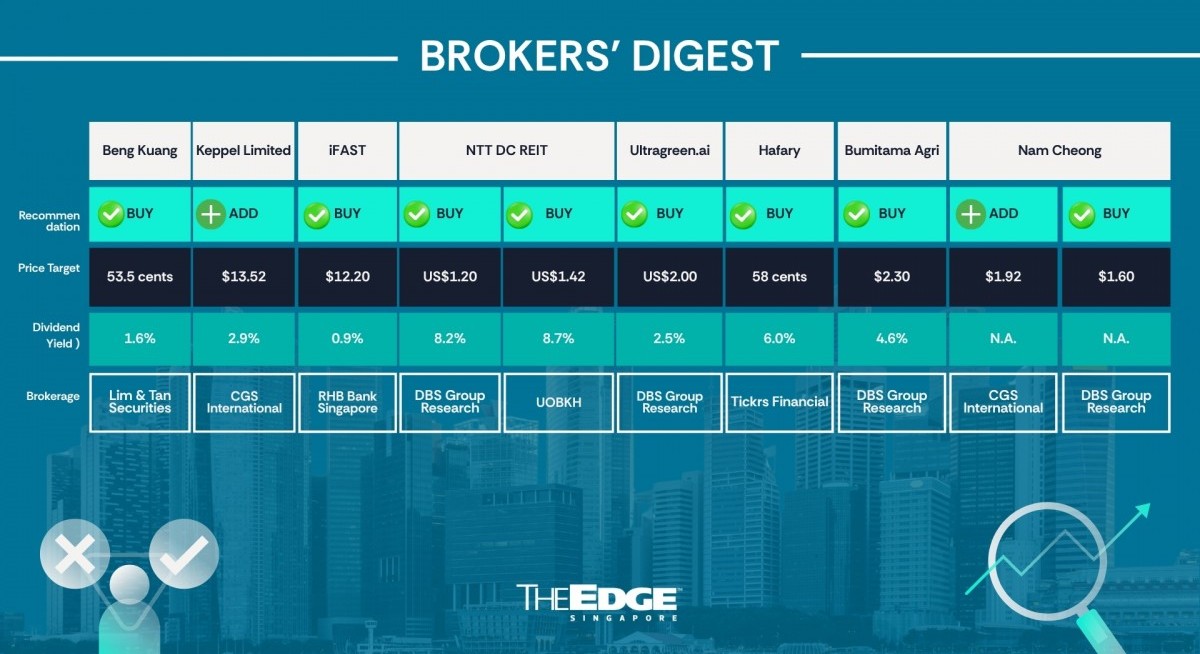

DBS Group Research ‘buy’ $2.30

Support from strong palm oil prices

William Simadiputra of DBS Group Research has raised his target price for Bumitama Agri from $1.90 to $2.30, citing expectations of better earnings this year driven by steady palm oil prices and higher production volumes.

In his April 7 note, Simadiputra, who has kept his “buy” call, points out that crude palm oil prices gained 14% y-o-y in 2025 to US$1,000 ($1,285) per metric tonne, and he expects prices to remain at around US$950 this year.

See also: Info-Tech to benefit from 'structural shift' in government's AI-related push: RHB

Bumitama’s FY2025 earnings beat Simadiputra’s forecast and he expects the company’s bottom line to ease somewhat by 6.1% to 2.6 trillion rupiah this year. “However, with limited export levies and taxes implemented so far, we see upside risk to our selling price and earnings forecasts,” says Simadiputra.

“Earnings should trend higher in 2026, mainly on a decent palm oil price and higher output trend. Bumitama has been paying good dividends; we see room to sustain said dividend and offer a decent yield of 5%–6% to investors,” he adds.

“If Bumitama pursues inorganic growth to expand its production volumes, it may become a key catalyst. As of now, Bumitama can maximise margins through cost efficiencies on its nucleus estates or by increasing mill utilisation to above 75% via external fruit purchases,” he adds.

See also: Mittal of DBS maintains 'buy' on Singtel on sale of Gulf Development stake

From his perspective, Bumitama’s share price, even after gaining 40.74% year to date to $1.90 at the close of April 6, might see further upside given the positive market outlook.

His revised target price of $2.30 is based on 20.4 times FY2026 earnings — a valuation multiple that is above Bumitama’s historical P/E level but is deemed justified due to “persistently high” crude palm oil prices and the company’s capability to maintain margin performance despite its reliance on external fruit purchases. — The Edge Singapore

Nam Cheong

Price targets:

CGS International ‘add’ $1.92

DBS Group Research ‘buy’ $1.60

Better revenue visibility

For more stories about where money flows, click here for Capital Section

CGS International (CGSI) and DBS are maintaining their respective bullish target prices for Nam Cheong after winning its latest charter contracts worth RM102.5 million ($32.7 million).

Ho Pei Hwa of DBS Group Research has kept her “buy” call and $1.60 target price on Nam Cheong.

The two vessels, leased by different customers, are to both support offshore oil and gas activities in the region. From an earlier 62%, Nam Cheong’s proportion of long-term charters has now reached 69%, just a shade below its target of 70%.

The other way to look at it is that 25 out of Nam Cheong’s 36 vessels are on long-term charter, with the remaining 9 vessels available to take advantage of potentially higher-priced spot charters.

Ho is keeping her forecasts for now but sees potential for the stock to re-rate, given how the charter contracts are a “positive reinforcement” of buoyant offshore oil and gas activities in the region.

Nam Cheong now has two workboats idling and if these are taken up as well, that will be further upside. In addition, Nam Cheong has recently won contracts to build new vessels at its yard. If there are more such new contracts, that will be another reason to re-rate this stock, says Ho, whose target price of $1.60 is based on 10 times FY2026 earnings.

Similarly, Meghana Kande and Lim Siew Khee of CGSI have maintained their upbeat “add” call for the stock. Citing the company’s management, they note that demand for offshore service vessels (OSVs) has not changed significantly in the past month despite the Middle East conflict, as spending decisions by national oil companies (NOCs) typically have longer lead times.

“As such, 2026 capex and activity are largely fixed, with uplift from persistent higher oil prices and greater emphasis on energy security likely to be reflected from 2027. Increased offshore activity by oil majors is a key catalyst for OSV demand,” state Kande and Lim, whose target price for this counter is $1.92.

Furthermore, domestic players like Nam Cheong are somewhat shielded from Malaysia’s cabotage policy if vessels are redeployed from the Middle East to this region. Also, Nam Cheong is not seeing any “material risk” to its recent US$64.5 million newbuild contract for a UAE-based customer, although enquiries from the Middle East have slowed.

The company is, however, seeing increased interest for newbuilds from players in West Africa, Vietnam and Thailand. Kande and Lim’s target price of $1.92 is based on 11 times FY2027 earnings, which is roughly in line with most peers.

Re-rating catalysts include higher-than-expected shipbuilding orders, increased capex by oil majors, which is driving higher demand for offshore services, and fleet expansion. On the other hand, downside risks include lower-than-expected fleet utilisation and higher costs, which could impact margins. — The Edge Singapore

UltraGreen.ai

Price target:

DBS Group Research ‘buy’ US$2

Reaction to tariffs a chance to accumulate

Amanda Tan of DBS Group Research has maintained her “buy” call and US$2 ($2.57) target price on UltraGreen.ai, as she believes recent price reactions to US tariffs on pharmaceuticals are unwarranted and that the current weakness is an opportunity for investors to accumulate. From the recent peak of US$1.86 on Feb 23, UltraGreen.ai shares have dipped by more than a fifth.

The Trump Administration has recently issued an executive order imposing a 100% tariff on patented pharmaceutical products imported into the United States unless manufacturers agree to government drug pricing arrangements or commit to producing the drugs domestically.

Generic pharmaceutical products, biosimilars, and associated ingredients are not subject to tariffs at this time, though this will be reassessed in one year, points out Tan in her April 7 note.

“The implications for UltraGreen.ai should be limited as indocyanine green is classified as a generic drug and therefore falls under the current tariff exemption,” says Tan, referring to UltraGreen.ai’s key product.

“Even if the tariff regime were eventually extended to include generics, we believe demand for indocyanine green would remain relatively price inelastic and Ultragreen.ai should be able to pass on any tariff-related cost increases to customers,” she says.

To put things into better perspective, Tan points out that the indocyanine green dye sold by UltraGreen.ai accounts for only a small portion of overall surgical procedure costs, with an average selling price of about US$90 to US$200 per vial. At the same time, its use improves visualisation during surgery and reduces the risk of complications. “As such, surgeons are unlikely to reduce usage even if prices rise materially,” she reasons.

In addition, UltraGreen.ai’s indocyanine green vials and kits sold in the Americas are packaged, serialised and labelled at the Praxis facility in Michigan. They are not imported from other countries, which could provide an additional mitigating factor against potential tariffs.

“In our view, the continued adoption of fluorescence-guided surgery, supported by a growing body of clinical evidence and expanding regulatory approvals across multiple markets, should remain the key driver of demand for UltraGreen.ai’s products,” says Tan. Trading at just 19 times FY2026 and 16 times FY2027 earnings, Tan believes this counter is now trading at an attractive valuation. — The Edge Singapore

Hafary Holdings

Price target:

Tickrs ‘buy’ 58 cents

Better entry point with pullback

Analyst Jaimes Chao of Tickrs Financial has maintained his “buy” recommendation for Singapore’s leading building materials supplier, Hafary Holdings, given that the recent share price pullback presents a better entry point for investors.

In his March 31 report, Chao highlighted that Hafary delivered “a solid set” of FY2025 ended Dec 31, 2025 results, which saw revenue advancing 9.1% y-o-y to $287 million and patmi rising 8.4% y-o-y to $29.9 million.

“Both topline and earnings were marginally below our forecast back in last August initiation report (which projected revenue of $292 million and patmi of $33.6 million), principally reflecting a softer second half in the manufacturing segment and elevated impairment charges on inventories,” says Chao.

Despite the miss, Chao believes that Hafary’s structural thesis of vertical integration driving margin recovery, geographic diversification broadening the revenue base and the balance sheet deleveraging progressively remains fully intact.

“With a share price at 46 cents, Hafary is trading at a trailing P/E ratio of 6.6 times and an EV/Ebitda of around 7.2 times. Those multiples are now slightly lower compared to our previous initiation report when its share price was at 48.5 cents,” Chao adds.

From his perspective, this presents investors with a wider margin of safety relative to a target price supported by an improved earnings trajectory.

“Hence, we are maintaining our ‘buy’ rating and a 12-month target price of 58 cents, based on a P/E ratio of eight times and revised FY2026 EPS of 8.15 cents, cross-checked by a seven times EV/Ebitda approach and a discounted cash flow analysis,” Chao explains.

Based on Chao’s estimate, with an FY2025 dividend yield of approximately 6%, the total shareholder return to his target price is around 32%. — Teo Zheng Long

Beng Kuang Marine

Price target:

Lim & Tan Securities ‘buy’ 53.5 cents

Sector tailwinds

On the back of successful execution of business strategies to enhance shareholder value and sector tailwinds, Lim and Tan Securities has initiated coverage of Beng Kuang Marine with a “buy” rating at a target price of 53.5 cents.

In their March 31 report, Nicholas Yon and Chan En Jie note that CEO Yong Jiunn Run has turned the company around from a loss-making, leveraged shipyard operator into a profitable, asset-light offshore and marine (O&M) service provider. They observe that the company has pivoted from capital-intensive shipyard operations to higher-margin recurring services.

Their confidence in Beng Kuang is driven by a combination of factors. Firstly, at the business level, Beng Kuang has announced a proposal to acquire the remaining 49% stake it does not own in its 51%-owned subsidiary, Asian Sealand Offshore and Marine (ASOM), for $60 million. The subsidiary offers a comprehensive range of services to O&M assets, including maintenance, repair and inspection.

For the last few years, ASOM has accounted for the bulk of Beng Kuang’s revenue in the infrastructure engineering segment, which, in the latest financial year, contributed 90% of operating profit. With the acquisition, Beng Kuang will consolidate 100% of ASOM’s earnings and cash flows. Yon and Chan project earnings per share to increase from 2.6 cents to 3.6 cents for FY2026. They also highlight improved quality of earnings, with a higher share derived from recurring offshore lifecycle income.

In addition, Yon and Chan believe that the ASOM transaction is a “good” deal that “pays for itself”, noting that cash is paid to ASOM, which Beng Kuang will own. They also point out that ASOM’s current management will take a 20% stake in Beng Kuang and will continue to manage ASOM post-transaction, ensuring business continuity.

The second factor influencing Yon and Chan’s report is the sustained demand for O&M support services. They see structural tailwinds, such as higher oil prices and a tight supply of floating production, storage, and offloading (FPSO) vessels, that will drive demand for Beng Kuang’s services to maintain, repair, inspect and extend the lifespans of offshore assets.

Another demand factor supporting Beng Kuang is the growth of the corrosion-prevention market. Citing market intelligence, the global offshore wind corrosion protection market could grow from US$3.8 trillion ($4.9 trillion) to more than US$10 trillion by 2033, representing a huge opportunity for Beng Kuang’s corrosion prevention division. They also note value-unlocking and asset monetisation initiatives, new contracts in deck equipment and shipbuilding worth $22 million, secured in FY2025, and land sales over the last few years.

Yon and Chan project Beng Kuang’s FY2026 and FY2027 net profit after tax at $12.1 million and $18.1 million, respectively. Their target price of 53.5 cents is based on 12 times forecasted blended FY2026 and FY2027 earnings, which represents a small discount to peers and reflects the timing of earnings consolidation, as full contribution from ASOM will only be reflected from the second half of FY2026. — Lin Daoyi

Keppel

Price target:

CGS International ‘add’ $13.52

M1 sale won’t be aborted despite delay

The closing of the sale of M1 by Keppel to Tuas has been extended for regulatory reasons, but Lim Siew Khee and Meghana Kande of CGS International do not expect it to be called off. The long-stop date for the sale, announced last August, has been extended to May 21, rather than the original six-month timeline.

The Infocomm Media Development Authority (IMDA) is “weighing all matters in light of the industry consolidation and the critical national infrastructure involved,” the analysts note. To recap, Tuas, which owns Simba, is listed on the Australian stock exchange.

Lim and Kande, in their March 27 note, suggest that a possible issue is that M1 and Simba use different network vendors. M1 operates an existing joint venture with StarHub that uses Nokia equipment, while Simba uses Huawei equipment for certain portions of its network.

Even so, Lim and Kande think it is unlikely that the deal will be spiked. They note that Tuas has already raised A$430 million in proceeds from an equity share issuance from August to October 2025 to fund the M1 acquisition partially.

Drawing back from Keppel’s comments at its FY2025 briefing, the company has guided that it will disburse 10%–15% of the gross value of its asset monetisation completed over 2025–2030.

Lim and Kande estimate this could translate into a special dividend per share of between 5 cents and 11 cents for the M1 deal upon completion.

Citing Keppel’s recurring income and dividend upside, they have kept their “add” call and $13.52 target price, which values the so-called “New Keppel” at 18 times FY2027 earnings and its non-core assets at book value.

For them, re-rating catalysts include completion of M1 divestment and further asset monetisation. On the other hand, downside risks include delays, unfavourable adjustments to deal terms to accommodate concerns raised by IMDA and a slower pace of monetisation. — The Edge Singapore

iFast Corp

Price target:

RHB Bank Singapore ‘buy’ $12.20

Tapping growing Asian wealth

Syahril Hanafiah of RHB Bank Singapore has initiated coverage of iFast Corp with a “buy” call and a $12.20 target price, noting that the company is a key beneficiary of the growing Asia-Pacific wealth management market.

“Earnings growth is braced by the scaling up of iFast Global Bank (iGB), stable recurring income from the ePension division, and its well-established wealth management platform business,” says Hanafiah.

Citing Mordor Intelligence, Apac’s wealth management market, valued at US$27.6 trillion ($35.5 trillion) in assets under management in 2025, is seen to grow to US$41.8 trillion by 2031.

iFast, on its part, may see its asset under administration grow at a CAGR of 22% over the coming three years. “Considering iFast’s asset-light model, we believe the group’s profit before tax margins will further expand as business scales up, which we estimate at between 39-42% over the forecast horizon,” says Hanafiah.

There is another growth angle: iFast’s UK-based digital banking arm, which is enjoying a jump in deposits — a trend likely to continue. “This deposit base expansion is translating into higher net revenue, thanks to the group’s strategy to redeploy deposits into short-duration sovereign bonds and investment-grade corporate bonds,” says Hanafiah.

The company’s ePension business in Hong Kong is expected to deliver slightly better profit before tax margins of 43% to 45% over FY2026 to FY2028.

With better operating leverage, iFast is seen to grow its net core earnings at a CAGR of 19% over the FY2026 to FY2028 period. Key risks include earnings dependence on assets under administration, regulatory risks and exposure to foreign exchange currencies. — The Edge Singapore

NTT DC REIT

Price targets:

DBS Group Research ‘buy’ US$1.20

UOB Kay Hian ‘buy’ US$1.42

Positive lease renewal

Dale Lai of DBS Group Research has maintained his “buy” rating and US$1.20 ($1.54) target price on NTT DC REIT following the lease renewal of its SG1 data centre at a higher rate.

While the contracted capacity has been modestly reduced by around 10%, from 3MW to 2.7MW, this has been more than offset by a significant uplift in rental rates, up by “an impressive” 23% to $474 per kW.

As a result, the REIT is expected to enjoy an estimated $1.5 million increase in rental income in the first year alone, translating to a 1.5% upside to distributable income for FY2025 to FY2026.

Lai views this as another key milestone delivered by NTT DC REIT since listing, following the successful backfilling of capacity at the CA1 and CA3 assets and the introduction of a new leasing incentive scheme to drive stronger leasing outcomes across the portfolio.

“Together, these initiatives highlight management’s proactive approach and consistent ability to execute on its stated strategies, further strengthening our confidence in the REIT’s ability to deliver on its commitments,” he adds.

Lai expects the next key catalyst to be the anticipated enhancement to the management fee structure, which is targeted for implementation over the next two quarters.

In his April 8 note, Jonathan Koh of UOB Kay Hian has similarly kept his “buy” call, but with a more upbeat target price of US$1.42 versus Lai’s. Koh likes the stock because it has no near-term financing risk, a stable cost of debt and a longer, bigger potential acquisition pipeline, thanks to the sponsor, including data centres in Frankfurt and Tokyo in FY2027.

Koh also points out that NTT DC REIT’s projected FY2027 yield of 8.7% beats Digital Core REIT’s 7%, Keppel DC REIT’s 4.8% and Mapletree Industrial Trust’s 6.4%. — The Edge Singapore