$3.35 BUY (Maybank Kim Eng Research)

$2.90 BUY (Jefferies Research)

$3.25 ACCUMULATE (Phillip Securities Research)

$3.04 OVERWEIGHT (Morgan Stanley Research)

$2.70 NEUTRAL (Macquarie Research)

Maybank Kim Eng Research is keeping Ascendas Real Estate Investment Trust (Ascendas REIT) as its top pick among Singapore REITs after unitholders supported its proposed acquisition of a portfolio of 30 business park properties.

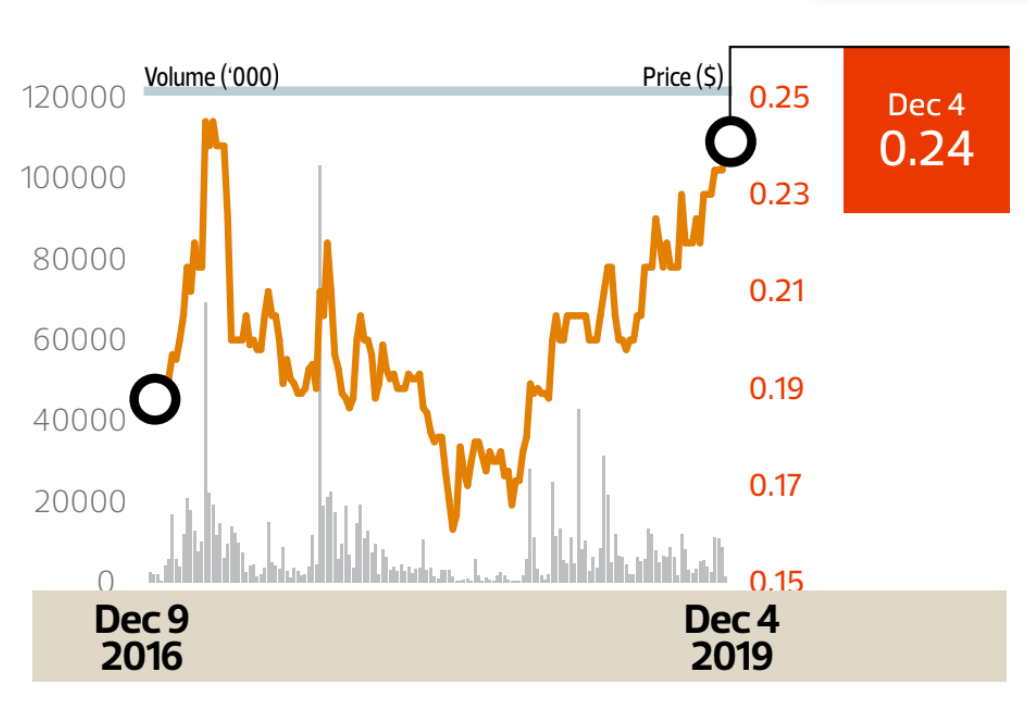

The manager of Ascendas REIT had on Nov 1 announced the proposed acquisition, which would see the REIT buy 28 properties located in the US and two properties in Singapore from CapitaLand for a whopping $1.66 billion.

At an extraordinary general meeting on Nov 27, unitholders voted overwhelmingly in support of the proposed acquisition, with some 93.2% voting for the resolution.

To help fund the proposed acquisition, the manager also proposed to undertake an underwritten and renounceable rights issue of some 498 million new units in Ascendas REIT at an issue price of $2.63 per unit to raise gross proceeds of around $1.31 billion.

Since the announcements, units in Ascendas REIT have retreated 5.7% from $3.17 on Nov 1 to close at $2.99 on Dec 4.

In a report on Dec 2, analyst Chua Su Tye notes that while Ascendas REIT’s share price has fallen, its growth fundamentals are looking up. He estimates that the REIT will see its revenue, net property income (NPI) and assets under management increase by 14%, 15% and 15% respectively.

Maybank is keeping its “buy” call on Ascendas REIT with an unchanged price target of $3.35.

“We see near-term catalysts from its Singapore recovery, rising overseas contributions and further acquisition opportunities,” Chua says. “Valuations at 5.5% DPU yield and 4.0% CAGR (compound annual growth rate) are compelling for this largest, most liquid industrial S-REIT name.” The proposed acquisition of two Singapore properties — Nucleos at Biopolis and FM Global Centre at Singapore Science Park 2 — comes as Singapore’s industrial sector recovery looks to gain traction in 2020 on easing supply-side pressures.

Meanwhile, the 28 US properties should lift Ascendas REIT’s overseas NPI contribution, Chua adds.

The analyst also notes that Ascendas REIT’s gearimg has improved to 34.6%, from 36.3% as at end-September. “We estimate debt headroom of $800 million to $1.8 billion to support further accretive deals, with Ascendas REIT likely to explore further bolt-on opportunities in key overseas markets, [in the] near term,” Chua says.

Fu Yu Corp

Price targets:

29.5 cents BUY (UOB Kay Hian Research)

24 cents BUY (RHB Group Research)

UOB Kay Hian is keeping its “buy” recommendation on Fu Yu Corp with a slightly higher price target despite the precision plastic components manufacturer’s reporting an 11.1% drop in its 3QFY2019 earnings.

Fu Yu saw its earnings fall to $3.9 million during the latest quarter, from $4.4 million a year ago. 3QFY2019 revenue slipped 2.2% to $51.3 million, even as operations in Singapore, Malaysia and China registered relatively stable sales.

Gross profit dived 17.8% to $8.7 million in 3QFY2019, as cost of sales rose 1.7% to $42.6 million despite the lower revenue. Gross profit margin fell 3.2 percentage points (ppt) to 17.0% in 3QFY2019.

Fu Yu says the decline was mainly due to the recognition of one-time expenses in relation to the closure of the group’s subsidiary in Shanghai, which will cease manufacturing operations by end-2019.

Excluding these one-time expenses totalling around $4 million, which was recognised in the cost of sales, the group would have registered a higher gross profit margin.

“Management has actively taken steps to achieve cost efficiencies, including its strategic decision to shift operations in Shanghai to its Suzhou factory, which should help lower overheads and improve utilisation,” says analyst John Cheong in a Nov 29 report. “Excluding a one-off expense from the shift, 3Q2019 results were good.”

Cheong notes that excluding the one-off, gross margin would have expanded 4.6 ppt y-o-y.

Among other things, Cheong favours Fu Yu for its attractive dividend yield. The group declared a second interim dividend of 0.25 cent per share in 3QFY2019, bringing total dividends for 9MFY2019 to 0.60 cent, representing a dividend payout of 50.4%.

“We estimate full-year dividend of 1.7 cents, translating into an attractive yield of 7.2%,” Cheong says.

The analyst also sees Fu Yu as a potential takeover target, on the back of its attractive valuation at 3.2 times 2020F EV/ Ebitda. “Note that its peers have been privatised at EV/Ebitda of 5.0 to 25.7 times in the past,” Cheong adds.

Semiconductor Industry

UMS Holdings

Price targets:

$1.13 INITIATE BUY (Maybank Kim Eng Research)

$1.08 BUY (DBS Group Research)

AEM Holdings

Price targets:

$2.38 INITIATE BUY (DBS Group Research)

$1.80 OUTPERFORM (KGI Securities Research)

$2.12 BUY (Maybank Kim Eng Research)

$2.12 ADD (CGS-CIMB Research)

As 5G and new technologies such as artificial intelligence and big data continue to drive the demand for semiconductors, market watchers remain sanguine on an industry that has been plagued by a slump over the past two years.

According to the World Semiconductor Trade Statistics (WSTS), a non-profit organisation that produces monthly industry shipment statistics, the global semiconductor market is expected to return to growth in 2020.

DBS Group Research analyst Ling Lee Keng notes that historically, the industry has staged a strong rebound after each major crisis, including the Asian financial crisis in 1997 and the global financial crisis in 2008. In the face of an escalating trade war, the analyst believes the sector is poised to mount another strong recovery.

Ling sees that all the signs are pointing to a bottoming out of the industry, with an improvement in shipping, billing and inventory trends; new growth drivers from new technologies; and semiconductor shipment recovering to a normalised longterm growth trend.

For one, precision engineering services firm AEM Holdings is flying high. Year to date, its share price has more than doubled to close at $1.92 on Dec 4, climbing from 82.5 cents at the start of the year. Yet, market watchers believe the counter is poised to soar even higher.

DBS is initiating coverage on AEM with a “buy” recommendation and a price target of $2.38, representing a potential upside of 24%.

“Our price target is pegged to 12.1 times FY2020F PER, and is well below its industry peers’ FY2020F PER of 17.8 times,” says Ling. “The share price trades closely to the semiconductor cycle, and we believe there will be a further rerating of its valuation multiple as the cycle begins to pick up, driven by demand for new technology.”

AEM provides handling and test solutions to some of the most advanced manufacturers who operate in the 5G economy. Its clients include manufacturers of microprocessors, high-speed communications, Internet of Things devices, and solar cells.

For 9MFY2019 ended September, the group saw its earnings jump 23.8% to $36 million, as revenue climbed 5.2% to $234.5 million.

“As technology nodes shrink, longer test times are required to perform more complex tests. In addition, systems and devices used in safety-critical marketswill require more stringent system-level tests. These would lead to higher demand for test handlers,” Ling says.

Notably, the analyst says AEM can expect to see growth driven by its key customer, Intel.

“Intel has guided for a record-high capex of US$16 billion ($21.8 billion) in FY2019 on the back of developments in new technology,” Ling says. “This should drive demand for test handlers, where AEM is believed to be the sole supplier.” Another counter that market watchers believe is poised to thrive on the semiconductor industry upturn is UMS Holdings.

Maybank Kim Eng Research is initiating coverage on UMS Holdings with a “buy” recommendation and a price target of $1.13, representing a total upside of 22% for the stock.

“UMS is in the early innings of an earnings upcycle, and has traded at such levels or higher in previous similar episodes,” analyst Lai Gene Lih says in a Dec 4 report.

In particular, the brokerage views the company’s key customer, Applied Materials, as a key determinant in the company’s ability to ride the market recovery. Noting that AMAT alone accounts for some 90% of the group’s revenue, Lai highlights that benefits are in the pipelines.

“[AMAT] sees semiconductor equipment spending recovery in FY2020E. This is driven by sustained investments from logic and foundry customers, followed by a recovery of equipment spending from memory customers in 2020 — led first by NAND, and subsequently DRAM,” says Lai.

In addition to being a strategic partner to a market leader, UMS is also poised to reap handsome rewards from its diversification strategy. The group has recently raised its stake in precision engineering firm JEP Holdings to 39%, which Lai calls “most promising”.

The company is also exposed to chemical engineering solutions via a 51% stake in Kalf Engineering, and has integrated part of its upstream process with a 70% stake in Starke Singapore.

Singapore banks

United Overseas Bank

Price targets:

$29.50 BUY (RHB Group Research)

$27.80 ACCUMULATE (Phillip Securities Research)

$29.20 BUY (DBS Group Research)

$29.10 ADD (CGS-CIMB Research)

$30.50 BUY (Maybank Kim Eng Research)

DBS Group Holdings

Price targets:

$27.30 ACCUMULATE (Phillip Securities Research)

$28.29 HOLD (CGS-CIMB Research)

$25.80 NEUTRAL (Macquarie Research)

$29.92 BUY (Maybank Kim Eng Research)

$28.50 EQUAL WEIGHT (Morgan Stanley Research)

Oversea-Chinese Banking Corp

Price targets:

$11.26 HOLD (Maybank Kim Eng Research)

$11.70 ACCUMULATE (Phillip Securities Research)

$11.50 HOLD (DBS Group Research)

$11.94 HOLD (CGS-CIMB Research)

$12.40 OUTPERFORM (Macquarie Research)

Singapore banks could see weaker margins ahead from falling interest rates, but analysts say growth could be lifted by overall positive momentum.

According to the latest data published by the Monetary Authority of Singapore, loan growth has moderated to 4.4% y-o-y in October.

“Momentum softened after peaking at 5.1% in August, though we think the pace remained respectable against a backdrop of slowing macro readings,” says Maybank Kim Eng Research analyst Thilan Wickramasinghe in a Nov 29 report.

“Interestingly, domestic loans increased 2.6% y-o-y — their fastest pace since February 2019. This suggests a pick-up in economic activity,” he adds.

Domestic business loans grew 5.2% y-o-y, which Wickramasinghe believes “may signal a pickup in SME (small and medium-sized enterprises) activity”. However, this was partially offset by continued weakness in domestic consumer loans, which fell 1.2% y-o-y in October, led by a decline in mortgages.

“Loan resilience should provide some respite to banks from a weakening rate cycle. Also, rising overseas mortgages may herald positive spillover for other private-banking operations, spelling upside for fee income,” Wickramasinghe says.

Maybank’s top pick for the sector is United Overseas Bank. The brokerage has a “buy” call on UOB with a price target of $30.50.

Wickramasinghe says. “Given its strong positioning, rising domestic SME loan demand should be positive for UOB,” Meanwhile, Fitch Ratings believes moderate asset-quality stresses could be a drag on Singapore banks’ earnings, with worsening trends seen to continue.

“Singapore banks experienced net interest margin (NIM) compression, asset-quality deterioration and slowing loan growth in 3Q2019. We expect these trends to continue and believe that earnings may have peaked in this cycle,” say Fitch Ratings’ Priscilla Tjitra and Ng Wee Siang in a Nov 25 note.

“Singapore’s short-term interest rates have declined in response to rate cuts in the US, as reflected in the q-o-q narrowing in NIM. Fitch views this NIM trend as likely to continue, owing to the lagged effect of lower rates and continued competitive pricing,” they add.

Singapore Telecommunications

Price targets:

$3.72 HOLD (Maybank Kim Eng Research)

$3.70 ADD (CGS-CIMB Research)

$4.05 BUY (HSBC Global Research)

$3.60 UPGRADE BUY (DBS Group Research)

$3.30 NEUTRAL (JPMorgan Research)

Maybank Kim Eng Research is raising its price target for Singapore Telecommunications (Singtel) by 8% to $3.72, after its Indian associate Bharti Airtel announced tariff increases.

“A return of pricing power to India’s market is a key positive for one of Singtel’s major businesses,” says analyst Luis Hilado in a Dec 2 report. “This leaves the Singapore wireless market as its remaining major overhang.” According to Hilado, this tariff increase, which was announced by all three major telcos in India, should result in a positive impact for Singtel. This is despite $6.5 billion in spectrum fees and penalties potentially levied against Bharti Airtel in a recent Indian Supreme Court ruling.

As a result of the Indian telco’s short-to-medium-term balance sheet pressure, Hilado is cutting his forecasts for Singtel’s core profits for FY2020 and FY2021 by 2%.

However, the analyst opines that the recent industry-wide wireless tariff increases in India should create positive Ebitda momentum for Bharti Airtel. “[This] should translate into a 1% increase in Singtel’s FY2022E core profit,” says Hilado.

While Bharti Airtel might be providing a lift, the Singapore market remains a challenge for Singtel.

Hilado notes that Singtel’s management remains guarded about the state of mobile competition in Singapore.

Singtel has seen q-o-q mobile revenues stabilising. But with more mobile virtual network operators entering the market, along with Australia’s TPG Telecom’s commercial launch in Singapore, the analyst sees more hurdles ahead for Singtel to overcome.

“Meanwhile, cash-flow pressure from prospective 5G investments without a clear mass-market price recovery remains a risk,” says Hilado.

Despite the Singapore market overhang, Hilado is keeping his “hold” call on Singtel.

“By nature of its diversified country and business exposure, Singtel’s profits can and have been pulled in several directions,” Hilado says. “Competition direction in India should provide positive momentum after several quarters of hits. Stability in other parts combined with a more constructive outlook for Singapore would improve the picture, in our view.”