OCBC Group Research ‘hold’ 40 cents

Awaiting operational improvements

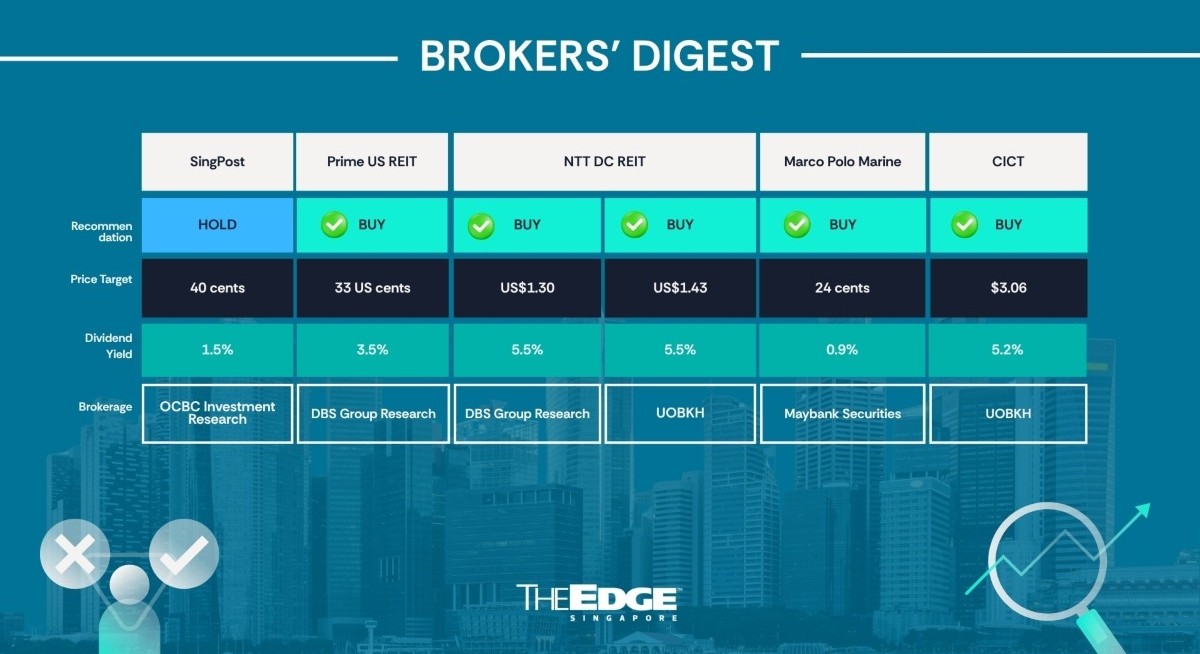

Ada Lim of OCBC Group Research has maintained her “hold” rating and fair value of 40 cents on Singapore Post (SGX:S08![]() ) , following lower FY2026 numbers that suggest the company’s turnaround towards commercial sustainability will take time to unfold.

) , following lower FY2026 numbers that suggest the company’s turnaround towards commercial sustainability will take time to unfold.

In FY2026 ended March 31, SingPost reported a 23.1% y-o-y drop in revenue to $376.1 million, while operating profit was down 68.9% to $11.8 million, as the logistics and letters segment posted an operating loss of $6.1 million due to lower volumes, swinging into the red from an operating profit of $35.8 million in FY2025.

See also: OCBC's Lim maintains Parkway Life REIT at 'add' following nursing home divestment

SingPost’s only bright spot, if any, was its property segment, where a higher occupancy rate at SingPost Centre helped post operating profit for the year at $45.2 million, up 0.5% y-o-y.

Together with significantly lower exceptional items, FY2026 earnings was 75.2% lower at $60.9 million, while underlying net profit was down 57% to $10.7 million.

SingPost plans to pay a final dividend of 0.06 cent and a so-called supplemental dividend of 0.41 cent, following 0.08 cent already paid for the interim.

See also: RHB's Yeo raises target price for Sheng Siong to $3.59 on new store openings

In the future, Lim sees the company aiming to reduce costs by at least 10% through optimising its operations and network.

SingPost is also seen to leverage its competitive advantage in access to the letterbox network to diversify beyond e-commerce by expanding across markets, services, and customer segments, including healthcare-related applications.

To this end, SingPost on May 14 announced an MOU with clinic chain Fullerton Healthcare Group to explore the co-development of a robust, integrated healthcare delivery system.

With SingPost Centre no longer slated for divestment and instead deemed a “crucial” part of the company’s portfolio, Lim believes the focus will be on potential yield-enhancement moves, including redevelopment to take advantage of lifted height restrictions upon the relocation of the nearby Paya Lebar air base.

“We see this as a doubling down on its core business rather than a major shift in tone versus what management has been working on since the divestment of its Australia business,” says Lim.

Following the results announcement, Lim observes that SingPost’s share price has reacted negatively, as investors were likely disappointed by the “lack of a bazooka development”.

“A turnaround towards commercial sustainability will take time and upfront investments, supported by financial discipline, and management’s ability to execute will be key. All things considered, we roll forward our forecasts.

For more stories about where money flows, click here for Capital Section

“With management categorically stating that SingPost is not looking to inject its properties into a REIT nor transform into a property player, we think its days of streamlining its asset base are over,” says Lim. — The Edge Singapore

Prime US REIT

Price target:

DBS Group Research ‘buy’ 33 US cents

Ongoing operational improvements

Derek Tan of DBS Group Research has kept his “buy” call and 33 US cents target price on Prime US REIT (SGX:OXMU![]() ) , noting continued operating recovery, with occupancy improving for the fourth consecutive quarter and leasing momentum remaining healthy despite a still-challenging US office backdrop.

) , noting continued operating recovery, with occupancy improving for the fourth consecutive quarter and leasing momentum remaining healthy despite a still-challenging US office backdrop.

“The manager is seeing good leasing velocity and momentum and is optimistic that take-up rates will continue,” says Tan.

As reported, Prime US REIT’s 1QFY2026 portfolio committed occupancy rose to 83.1%, up 0.4 percentage points (ppt) q-o-q and 4.2 ppt y-o-y, thanks to higher rental reversion of 4% and with 99,000 sq ft of space leased, including 40,000 sq ft at Village Center Station I leased for 11 years to S&P Global.

In the quarter, net property income improved by 3.3% q-o-q to US$17.2 million, while distributable income was up 12.1% q-o-q to US$6.5 million.

“With sequential improvement in overall performance, we remain attracted to Prime US REIT’s valuation at 0.3 times P/B and a FY2026–FY2027 yield of 8.8% and 9.9%, respectively, based on an assumed 65% payout ratio, which is reaffirmed by management,” says Tan.

“We believe the key near-term catalyst remains the execution of the sizeable embedded leasing pipeline, with 463,000 sq ft of committed leases, equivalent to 11% of committed occupancy, which is expected to commence rental contribution progressively from 3QFY2026 onwards.

Following which, the REIT will likely enjoy a gradual step-up in cash flow recovery into FY2027, adds Tan.

However, he warns that the REIT’s balance sheet metrics remain the key investor overhang, with aggregate leverage at 45.2%, an all-in borrowing cost of 5.4% and an interest coverage ratio of 1.6 times.

“While leasing traction and positive rental reversions suggest that the REIT’s portfolio is stabilising, the pace of earnings recovery and refinancing execution will likely remain central to investor focus amid structurally softer US office demand and elevated interest rates,” says Tan.

Nonetheless, from his perspective, one of the strongest attributes of the REIT’s initial portfolio is that average lease rents are below market by around 8%.

“As Prime US REIT renews its leases over the next two years, there is potential for positive rental reversions which would help drive near-term earnings and distributable income,” he adds. — The Edge Singapore

NTT DC REIT

Price targets:

DBS Group Research ‘buy’ US$1.30

UOB Kay Hian ‘buy’ US$1.43

Better than forecasts at IPO

Analysts have raised their target prices for NTT DC REIT (SGX:NTDU![]() ) after it reported higher-than-expected results for FY2026, driven by higher tenant fit-out income, higher co-location revenue, lower taxes and favourable forex.

) after it reported higher-than-expected results for FY2026, driven by higher tenant fit-out income, higher co-location revenue, lower taxes and favourable forex.

In FY2026 ended March, revenue hit US$164.8 million ($210.97 million), up 2.5% above the forecast provided at the time of its IPO last July, while net property income (NPI) rose 2.3% to US$74.9 million.

Distribution per unit (DPU) for the July 14 to March 31 period was 5.56 US cents, 2.6% above forecast, partly due to lower borrowing costs. On an annualised basis, DPU would have been 7.81 US cents.

As at March 31, portfolio occupancy improved 0.5 percentage points (ppts) to 95.1% from the previous quarter, while committed occupancy was higher at 98.5%.

In addition, rental reversion was up 8.5% in FY2026, while portfolio valuation rose 11.3% to US$1.67 billion. Gearing was down 29.2 ppt from 32.5% q-o-q, while total debt fell to US$517 million from US$523 million.

In his May 14 note, Dale Lai of DBS Group Research has not only kept his “buy” call on this stock but also raised his target price from US$1.20 to US$1.30, following a 2.5% increase in his FY2027 DPU estimates to reflect better-than-expected operational results.

“Forward earnings visibility remains well supported by NTT DC REIT’s high committed occupancy, positive rental reversions, and strong tenant retention rates across its portfolio,” says Lai.

“Based on our understanding, management is already in advanced renewal discussions with the respective tenants and remains confident of securing renewals at healthy positive rental reversions, underpinned by continued robust demand for high-quality data centre capacity,” adds Lai.

Lai sees several potential near-term catalysts that could further support a re-rating of the stock. These include a potential revision to the management fee structure, targeted for implementation sometime in 3QFY2027; the possible inclusion of an index in June following the publication of its first annual report; and the announcement of a maiden accretive acquisition.

Jonathan Koh of UOB Kay Hian has similarly stayed bullish on this stock. From an initial target price of US$1.42, he figures NTT DC REIT is worth US$1.43, with an “attractive” FY2027 DPU yield of 7.7% and 8.0% in FY2028, the highest among data centre REITs.

Koh maintains his “buy” call on NTT DC REIT. According to Koh, the REIT is exploring various acquisitions, including a hyperscale 24MW data centre in Frankfurt in 1HFY2027. Valued at between US$450 million and US$500 million, the centre is expected to provide an NPI yield of above 6%.

The REIT is also in talks with other entities within the NTT Group to acquire stabilised data centres within Japan, including a 20MW data centre in Tokyo, which is expected to provide an NPI yield of above 5%. — The Edge Singapore

Marco Polo Marine

Price target:

Maybank Securities ‘buy’ 24 cents

RTO of yard business

Jarick Seet of Maybank Securities has raised his target price for Marco Polo Marine (SGX:5LY![]() ) to 24 cents from 20 cents after plans to spin off its shipyard business for a separate listing via a $139 million reverse takeover deal of Fuji Offset Plates Manufacturing.

) to 24 cents from 20 cents after plans to spin off its shipyard business for a separate listing via a $139 million reverse takeover deal of Fuji Offset Plates Manufacturing.

Under the terms of this deal, Fuji Offset, controlled by the Teo family, which is also a substantial shareholder of Marco Polo Marine, will issue new shares at 70.1 cents each. Upon completion of the transaction, Marco Polo Marine will hold up to 76.8% of the enlarged entity, which will be renamed Marco Polo Shipyard Engineering.

“We view the transaction positively, as it should accelerate Marco Polo Marine’s growth by providing a separate listed platform to raise funding, while the $120 to $139 million valuation represents a substantial premium to the shipyard business’s book value within Marco Polo Marine,” says Seet.

“We also believe the shipyard operations are poised for expansion and potentially new vessel types in construction and repair, which should further support medium-term growth,” he adds. Separately, Marco Polo Marine reported 1HFY2026 adjusted patmi of $13.8 million, which is in line with Seet’s estimates, while revenue in the same period was up 40% y-o-y to $74 million.

According to Seet, the current 3Q is typically the strongest for the company, suggesting that numbers for the current 2HFY2026 will be “stronger” than those for the preceding 1HFY2026.

In future, Seet expects the fleet expansion to significantly enhance the company’s earnings in FY2027 and FY2028.

As such, he is maintaining his “buy” call, given that Marco Polo Marine is in a rapid growth phase and will benefit from diversifying away from Oil & Gas into offshore wind farms, which will support energy security concerns underscored by the Iran–US conflict.

His revised target price of 24 cents is based on a higher valuation multiple of 24 times FY2026 earnings, up from 20 times. — The Edge Singapore

CapitaLand Integrated Commercial Trust

Price target:

UOB Kay Hian ‘buy’ $3.06

Paragon deal to help lift DPU

Jonathan Koh of UOB Kay Hian has raised his target price for CapitaLand Integrated Commercial Trust (CICT) (SGX:C38U![]() ) from $2.95 to $3.06, following the largest S-REIT’s acquisition of the Paragon mall along Orchard Road for an agreed-upon property value of $3.9 billion, which yields 3.9%. “The acquisition strengthens CICT’s Singapore-centric portfolio by adding a sizeable freehold upscale mall in the tightly held Orchard Road shopping corridor,” says Koh.

) from $2.95 to $3.06, following the largest S-REIT’s acquisition of the Paragon mall along Orchard Road for an agreed-upon property value of $3.9 billion, which yields 3.9%. “The acquisition strengthens CICT’s Singapore-centric portfolio by adding a sizeable freehold upscale mall in the tightly held Orchard Road shopping corridor,” says Koh.

CICT will partially fund this acquisition by selling Asia Square Tower 2 to IOI Properties for $2.5 billion, yielding the REIT a divestment gain of $199.9 million. CICT has raised another $750 million to fund the deal by issuing new units at $2.30 each via a private placement.

Koh estimates that these two transactions will be DPU-accretive by 1.7% while keeping aggregate leverage at a prudent 38.7%. “The capital redeployment enhances income resilience by shifting from a leasehold office asset into a freehold, mixed-use development with stable cash flows and defensive medical exposure,” he adds.

CICT is assessing its own study on the types of asset enhancements to be made with Paragon. Unitholders were persuaded to accept Paragon REIT’s privatisation after being told that up to $600 million was needed to fund enhancement works to make the mall more competitive.

“CICT’s management views Paragon’s strong tenant demand, prime location and exposure to medical tourism as key factors supporting sustainable long-term income growth,” says Koh.

According to Koh, management has guided to mid-single-digit rental reversion for both its retail and office portfolios in 2026. The REIT will benefit from a full year’s contribution from its 50% stake in ION Orchard in 2025, which was completed in October 2024, while CapitaSpring has been contributing at 100% interest since last August.

By the end of this year, more upside and contribution should come from a later phase of another property, Galileo and newly enhanced space at Tampines Mall. Down the road, CICT, says Koh, is expected to focus on expansion in Singapore, including Changi Jewel from its sponsor pipeline, while also exploring divestment of overseas assets.

For now, Koh has raised his DPU estimates by 2.4% for FY2024 and 2.1% for FY2028, mainly from the acquisition of Paragon and a lower cost of debt, leading to a higher target price of $3.06. — The Edge Singapore