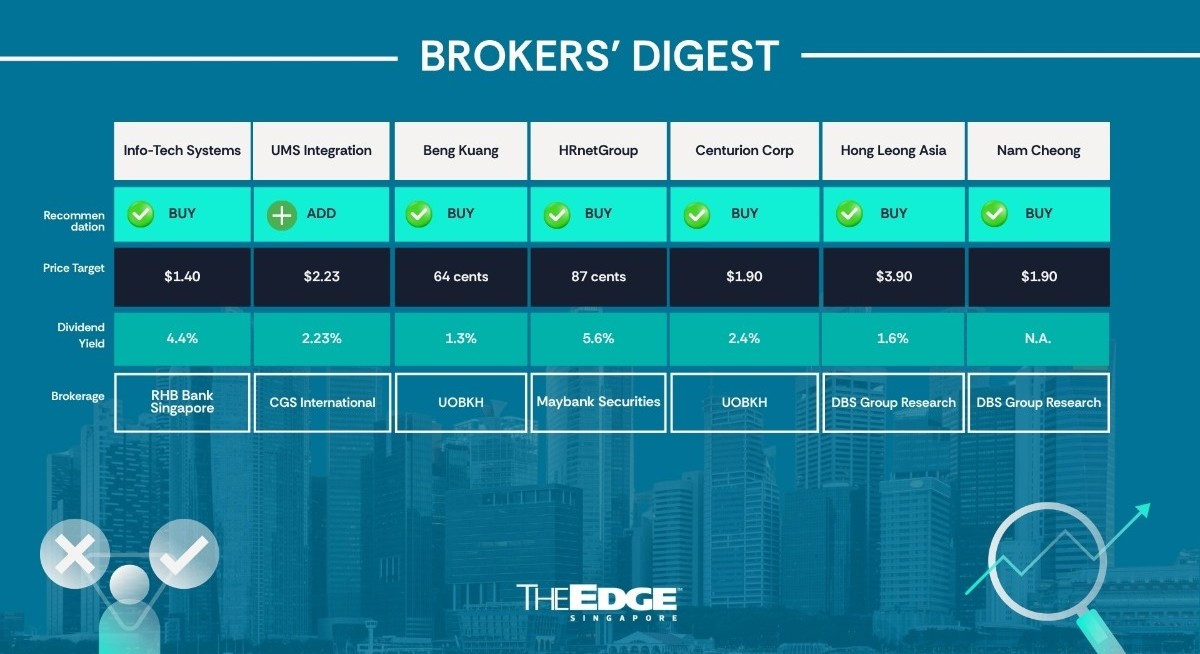

RHB Bank Singapore ‘buy’ $1.40

Capitalising on policies

RHB’s Syahril Hanafiah has initiated coverage on Info-Tech Systems (SGX:ITS![]() ) (ITSL) with a “buy” call and a target price of $1.40. The Singapore-headquartered company provides a human resource management system (HRMS) and accounting software for SMEs and made its trading debut on July 4, 2025.

) (ITSL) with a “buy” call and a target price of $1.40. The Singapore-headquartered company provides a human resource management system (HRMS) and accounting software for SMEs and made its trading debut on July 4, 2025.

“We believe Info-Tech Systems is well positioned to capitalise on the policy-driven shift for SMEs to digitalise core functions, given ITSL’s local native and SME-centric platforms, on top of the huge, yet underserved software as a service (SaaS) SME market,” writes Syahril in a report on April 16.

See also: UOB Kay Hian maintains 'buy' call on Food Empire with $3.49 target price

Syahril’s target price is pegged at a forward P/E multiple of 15.5 times on estimated FY2027 earnings. The valuation also reflects a 15% discount relative to regional peers, given Info-Tech Systems’ relatively small size.

“ITSL’s key strength lies in its ability to build and maintain a locally compliant, integrated payroll engine across four markets,” writes Syahril, referencing the company’s operating markets of Singapore, Malaysia, Hong Kong and India.

According to forecasts cited by RHB, the addressable market in these four countries is expected to grow by 8% CAGR to US$4.65 billion in 2028, up from US$3.69 billion. RHB expects ITSL to outperform the forecast, delivering a higher revenue CAGR of 10.5%.

See also: Goldman Sachs says Chinese cross-border curbs, effective July 1, had limited impact “so far”

Compared with its competitors, ITSL products offer relatively affordable pricing for SMEs, given the breadth of its software offerings. “While not the cheapest option, we view ITSL’s pricing as highly attractive given the breadth of its HRMS and payroll suite,” Syahril writes.

In addition, Syahril believes Info-Tech Systems will enjoy favourable policy support for its software products. Specifically, changes in regulatory requirements will create a “recurring compliance burden” for SMEs that must rely on regularly updated software. “We believe ITSL is well positioned to capture sustained growth given its localisation expertise, compliance‑first platform, and established regional presence.”

Overall, RHB is forecasting a core profit CAGR for 12.3% for FY2025 to FY2028. This is driven by Info-Tech Systems’ growing user base for its existing HRMS and accounting software products across its operating markets. Syahril is forecasting higher core profit margins of 32.4%, 32.7%, and 33.4% for FY2026 to FY2028, up from 31.9% in FY2025, reflecting the asset-light nature of Info-Tech Systems’ business. — Kwan Wei Kevin Tan

UMS Integration

Price target:

CGS International ‘add’ $2.23

Riding the ‘giga cycle’

For more stories about where money flows, click here for Capital Section

Among the stocks to outperform the Straits Times Index (STI) this year is semiconductor equipment manufacturer UMS Integration (SGX:558![]() ) . Closing at $1.79 on April 15 and accounting for the one-for-four bonus share issue, the counter has risen by around 57% since the start of 2026, compared to the STI’s 8% gain.

) . Closing at $1.79 on April 15 and accounting for the one-for-four bonus share issue, the counter has risen by around 57% since the start of 2026, compared to the STI’s 8% gain.

CGS International (CGSI) analyst William Tng believes that the counter, listed on both SGX and Bursa Malaysia, has not yet reached its ceiling. In his April 15 report issued after trading hours, Tng is reinforcing his “add” call with a higher target price of $2.23, up from the previous $1.88 issued on March 2.

Tng not only expects UMS to report a stronger 2HFY2026 as customer orders skew towards the second half of the year, but also thinks there is a possibility of UMS reporting a 1QFY2026 net profit of around $12.2 million, representing a 10% q-o-q and 24% y-o-y increase.

The way Tng sees it, UMS is likely to enjoy a stronger earnings upcycle in FY2026 to FY2028, driven by AI demand and two customers. He notes that, according to the company’s FY2025 annual report, released on April 13, UMS has renewed a three-year integrated system contract with major customer “A”. Coupled with new product pipelines from “A” and new customer “L”, management is confident in the company’s FY2026 performance.

UMS’s confidence in its prospects is derived from expected customer demand and industry tailwinds. The company notes that both customers have forecasted “robust” demand growth for 2026 and 2027 due to increasing AI adoption. UMS also points out that both “A” and “L” are major players in the high-bandwidth memory and advanced logic space, which is experiencing “escalating” demand.

In addition, UMS expects the semiconductor industry to enter a record period of growth, surpassing US$1 trillion in revenue for the first time in 2026. The company also cites industry estimates that global sales of semiconductor manufacturing equipment will grow from 2025 to 2027 and reach a record high of U$156 billion, signalling a clear shift away from traditional consumer-driven cycles toward a new “Giga Cycle” in which major tech companies are investing heavily to compete in the AI era.

On the back of expected business growth driven by industry tailwinds and more customer orders, Tng raises his projected revenue for FY2026 to FY2028 by 0.2%–12.7%, leading to a 2.7%–27.6% increase in earnings per share, with earnings per share experiencing a 29.6% CAGR from FY2025 to FY2028. Valuing the company at 26 times of forecast FY2027 EPS, or two standard deviations above the five-year P/E from 2022 to 2026, Tng sets a target price of $2.23. — Lin Daoyi

Beng Kuang Marine

Price target:

UOB Kay Hian ‘buy’ 64 cents

High barriers to entry

UOB Kay Hian analysts Tang Kai Jie and Heidi Mo have initiated coverage on Beng Kuang Marine (SGX:BEZ![]() ) (BKM) with a “buy” call, given the company’s market-leading position providing corrosion prevention, repair and life extension services, a high-barrier segment within offshore asset integrity services, operating across Southeast Asia, the Middle East, and Latin America.

) (BKM) with a “buy” call, given the company’s market-leading position providing corrosion prevention, repair and life extension services, a high-barrier segment within offshore asset integrity services, operating across Southeast Asia, the Middle East, and Latin America.

“With non-discretionary demand driven by safety, regulatory compliance, and asset longevity, BKM enjoys resilient margins and strong pricing power, supported by global industry demand where corrosion costs the maritime sector US$50 to US$80 billion [$63.5 billion to $101.6 billion] annually,” state Tang and Mo in their April 20 note.

Across the industry worldwide, there are roughly 180 floating production, storage, and offloading (FPSO) units in operation, of which over half are more than 30 years old and a quarter exceed 40 years.

“For these ageing vessels, demand for inspection, repair, and corrosion prevention remains strong as high costs and long newbuild backlogs limit replacements, supporting BKM’s services as operators extend asset life,” add Tang and Mo, who have a target price of 64 cents.

Under the company’s BKM 2.0 strategy, it is shifting towards an asset-light, service-led model, focusing on higher-margin, recurring services. “As part of this strategy, the proposed acquisition of the remaining 49% of Asian Sealand Offshore and Marine (ASOM) for $60 million, expected by end of June, will fully consolidate its high-margin earnings and align management interests with BKM,” add the analysts, who expect material earnings accretion where BKM’s earnings could jump fourfold to $20 million in a bull-case scenario in FY2027 vs $5 million in FY2025.

Their target price of 64 cents is based on a 12.1 times FY2027 P/E ratio, which is 1.5 standard deviations above its five-year historical P/E ratio. BKM currently trades at 9.0 times FY2027 P/E. This represents a discount to peers’ average FY2027 P/E ratio of 14.6 times, highlighting BKM’s undervaluation despite its market leadership,” both Tang and Mo conclude. — Teo Zheng Long

HRnetGroup

Price target:

Maybank Securities ‘buy’ 87 cents

Clear valuation disconnect

Maybank analyst Eric Ong has re-initiated coverage on HRnetGroup (SGX:CHZ![]() ) with a “buy” call and a target price of 87 cents. The Mainboard-listed recruitment agency was founded in 1992 and went public in 2017.

) with a “buy” call and a target price of 87 cents. The Mainboard-listed recruitment agency was founded in 1992 and went public in 2017.

“Beyond just being a regional recruiter, we believe HRnet is structurally difficult to replicate,” writes Ong in an April 19 report, noting that the company operates on a co-ownership model involving 47 business leaders holding equity stakes in HRnetGroup.

This model ensures that HRnetGroup’s managers are incentivised to collaborate rather than compete with one another. “This fosters a culture that competitors cannot easily poach or reproduce,” Ong adds, noting that the scalability of the model has been proven by how HRnetGroup was able to expand into new markets like Vietnam and Taiwan.

Unlike most recruitment agencies that focus solely on professional recruitment or flexible staffing, HRnetGroup derives revenue from both.

Ong says this “dual-engine model” has allowed the company to remain profitable since 1993. The flexible staffing business provides a “predominantly recurring base of revenue and gross profit” and helps stabilise the business, he adds.

“While professional recruitment captures upside during periods of economic expansion, flexible staffing delivers steady volumes, consistent cash flow, and strong client retention,” Ong says.

Ong says HRnetGroup’s sizeable cash pile of over $336 million is “more than just a defensive buffer” but also a “clear valuation disconnect.” In FY2025, HRnetGroup held $262.9 million in cash and cash equivalents, $62.7 million in credit-linked notes and $10.7 million in short-term Singapore Government Securities and gold.

In addition, the cash pile enables HRnetGroup to pursue any merger and acquisition opportunities that may arise in the future. “This balance sheet strength also provides flexibility to capture market share from weaker competitors during downturns,” Ong writes.

Although HRnetGroup has no direct comparables listed on the Singapore Exchange, its net margin of roughly 8% to 11% puts it ahead of peers such as Persol and Kelly. This is a reflection of the company’s “disciplined cost management and a strategic focus on professional recruitment over lower-margin temporary staffing,” Ong says.

Ong’s valuation is pegged to a forward P/E multiple of 18 times on estimated FY2026 earnings. The stock continues to trade at an undemanding valuation of less than 9 times its forward P/E based on estimated FY2026 earnings, excluding cash, he adds. “This presents a significant arbitrage opportunity compared to some Japanese and Chinese peers, which trade at multiples of over 20 times.” — Kwan Wei Kevin Tan

Centurion Corp

Price target:

UOB Kay Hian ‘buy’ $1.90

A dorm that is a ‘toll road’

Adrian Loh of UOB Kay Hian has kept his “buy” call and $1.90 target price on Centurion Corp (SGX:OU8![]() ) after the dormitory operator acquired an asset in Karratha, Australia, for A$45 million ($45.5 million).

) after the dormitory operator acquired an asset in Karratha, Australia, for A$45 million ($45.5 million).

“We view this as a strategic opportunity to acquire an operational, income-generating asset at appraised value with zero development risk,” says Loh in his April 20 note.

On a pro forma basis, if the deal were completed on Jan 1, 2025, it would add 5% to its earnings per share — a “modest but meaningful” increase, given its size, which is equivalent to around 3% of the market cap.

“In addition, we view the implied 2025 P/E acquisition multiple of 7.1 times as conservative relative to Centurion’s existing asset base and its 2027 P/E of 10.9 times,” adds Loh.

The asset is in the town of Karratha, where some 46,000 mining workers rotate through monthly. The town has a capacity of 13,000 beds for these so-called “fly-in, fly-out” miners, but a “severe” shortage remains during peak periods.

“Against this backdrop, we view Centurion’s Karratha asset not as a cyclical bet on commodity prices but instead a toll-road on the structural, non-discretionary accommodation needs of a workforce that sustains one of the world’s most irreplaceable resource export corridors,” says Loh.

The way Loh sees it, this acquisition is a “logical extension” of a “strong” business segment. The “structural similarities” are “compelling” as workers’ dormitories in Australia and Singapore are seen as asset-heavy, operationally intensive, and long-duration, demand-driven by institutional rather than retail clients.

Over time, this asset, according to Loh, will likely be injected into Centurion Accommodation REIT, which UOB Kay Hian rates as a “buy” and has a $1.51 target price.

For now, Loh is keeping his earnings forecast for the current FY2026 to FY2028. His target price of $1.90 is based on 12.4 times earnings, which is one standard deviation above Centurion’s long-term average P/E, excluding the Covid-19-affected years of 2019-23.

“We believe that this target P/E multiple is undemanding given the company’s earnings growth over the next two years.

“With expanding bed capacity, structurally undersupplied living sectors and improved leverage metrics, earnings visibility for 2026–2027 appears strong, in our view,” he adds. — The Edge Singapore

Hong Leong Asia

Price targets:

DBS Group Research ‘buy’ $3.90

UOB Kay Hian ‘buy’ $4.90

Acquisition of household shelter maker for $90.7 mil

The growing construction industry has attracted not just the interest of investors, but from companies with a growing appetite to develop a bigger presence too.

On April 21, Dale Lai of DBS Group Research kept his “buy” call and $3.90 target price on Hong Leong Asia (SGX:H22![]() ) (HLA) after its $90.7 million all-cash acquisition of privately-held Yong Tai Loong, which builds bomb shelters, letter boxes, door frames, clothes racks and other residential fittings.

) (HLA) after its $90.7 million all-cash acquisition of privately-held Yong Tai Loong, which builds bomb shelters, letter boxes, door frames, clothes racks and other residential fittings.

The acquisition, says Lai in his April 22 note, is strategically aligned with HLA’s aim of strengthening its building materials segment in Singapore.

YTL, with six decades of operating history, has built an “entrenched” market position and a visible order pipeline tied to residential construction demand. It is one of the five HDB-approved suppliers of household shelters, giving it a “significant” market share in this niche sector.

Lai figures that HLA paid about 2.6 times book value for this acquisition, implying a significant goodwill component. On a pro forma basis, assuming the deal was completed on Jan 1, 2025, it would have lifted HLA’s earnings per share (EPS) from 15.08 cents to 15.79 cents. However, if one-offs at YTL are discarded, EPS would have increased to 17.89 cents instead.

“The key positives are that the deal is strategically coherent, expands HLA’s product offering in Singapore, leverages existing capabilities, and is earnings accretive from the outset, with a P/E multiple of only around 4.5 times,” says Lai.

Even upon completion of this deal, HLA continues to maintain a very healthy net cash position, with a net cash over equity position of 0.65 times.

Adrian Loh of UOB Kay Hian is even more bullish. While keeping his “buy” call, Loh has increased his target price to $4.90 from $4.71, citing the ongoing construction boom. “As one of only five HDB-approved shelter suppliers, we see YTL as being in a privileged position that cannot easily be replicated by new entrants,” says Loh. — The Edge Singapore

Nam Cheong

Price target:

DBS Group Research ‘buy’ $1.90

Rally ‘still has further legs’

Days after announcing it has pared its debt, Mainboard-listed Nam Cheong (SGX:1MZ![]() ) has followed up with another piece of news that investors will presumably find favourable. On April 21, the Sarawak-based shipyard announced that it is selling its first newbuild vessel in over a decade, as well as a 16-year-old vessel, for a combined US$36.7 million ($46.7 million).

) has followed up with another piece of news that investors will presumably find favourable. On April 21, the Sarawak-based shipyard announced that it is selling its first newbuild vessel in over a decade, as well as a 16-year-old vessel, for a combined US$36.7 million ($46.7 million).

According to Nam Cheong’s bourse filing, both vessels were delivered in the second quarter of 2026. Net proceeds will primarily be used to support shipbuilding activities, either for external sales or for fleet expansion to grow the recurring income base.

For DBS analyst Ho Pei Hwa, the transactions have prompted an increase in the target price to $1.90 from $1.60. In her April 22 report, she states that Nam Cheong has made another “breakthrough” with the sale of the newbuild Geotech offshore support vessel (OSV).

The way Ho sees it, while the asset sales likely reduce recurring charter income by 3%–4%, this is more than offset by the potential for newbuild activities as she sees the sales as evidence of an emerging newbuild cycle on the back of improving OSV fundamentals.

She also points out the company’s strengthening balance sheet, noting that its net gearing has “improved dramatically” from 0.6 times in FY2024 to below 0.1 times as of April 2026 and that restructured debt has halved to around RM285 million ($91.7 million) in just over two years.

While Nam Cheong’s stock price has grown more than tenfold over the past two years, Ho is confident that the counter can reach new highs, describing its rally as “still has further legs”. With high oil prices and rising energy security concerns sustaining demand for oil and gas infrastructure, including storage terminals and production-related facilities, she believes Nam Cheong will be able to capitalise on opportunities in this space.

Ho values Nam Cheong at 12 times P/E, up from 10 times previously. Her current forecasts have factored in only four newbuild projects announced earlier this year, and further newbuild wins would prompt earnings upgrades and a share price re-rating. — Lin Daoyi