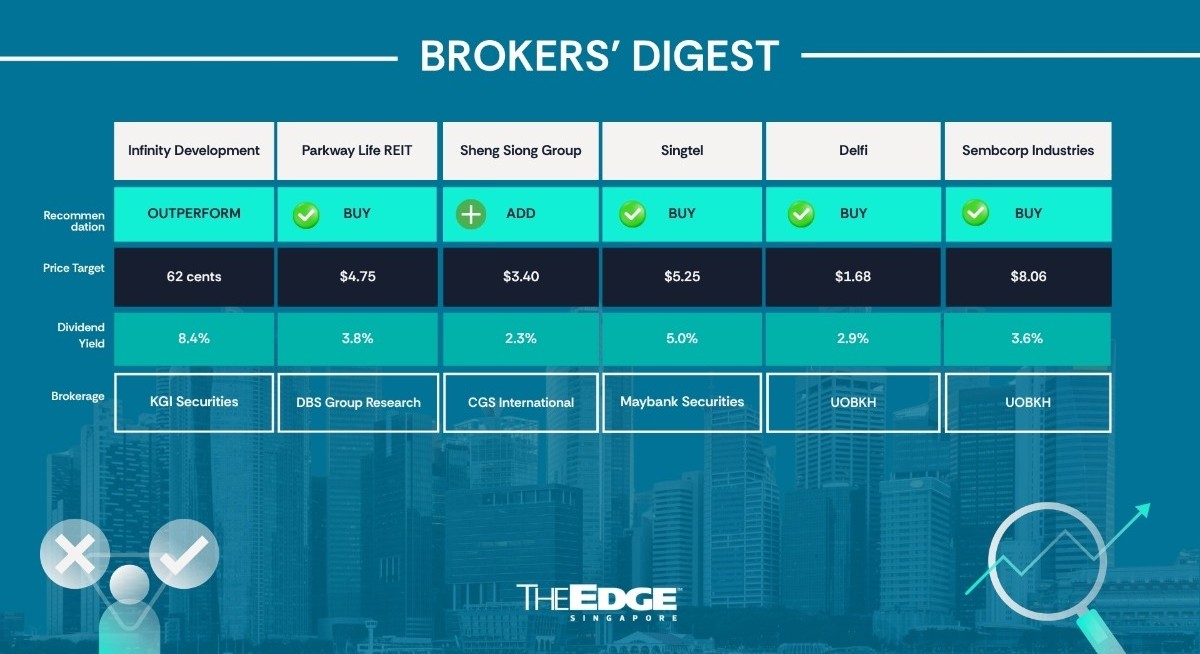

KGI Securities ‘outperform’ 62 cents

Sticky and resilient business

Alyssa Tee of KGI Securities has initiated coverage on newly listed Infinity Development Holdings (SGX:ZBA![]() ) with an “outperform” call and 62 cents target price. The Hong Kong-based but Singapore-listed glue maker is seen as having a business model “stickier than any adhesive”. Its business model is “structurally defensive” and as an upstream input supplier, its business is “relatively insulated” from direct consumer-facing tariffs.

) with an “outperform” call and 62 cents target price. The Hong Kong-based but Singapore-listed glue maker is seen as having a business model “stickier than any adhesive”. Its business model is “structurally defensive” and as an upstream input supplier, its business is “relatively insulated” from direct consumer-facing tariffs.

The company specialises in providing glue and other materials for footwear makers. It operates production facilities in Vietnam, China and Indonesia and its products are used in both product development and mass production, underpinning long-term relationships with its customers, says Tee.

See also: UOBKH maintains 'buy' and 71 cents target price on LHN

In the most recent FY2025, the company reported earnings of HK$122 million ($19.8 million), up 21.9% on the back of a 13.4% gain in revenue to HK$835 million. The bulk, or 88% of the sales, were made within Asean, with Vietnam accounting for 59%. The remaining 12% was from China. Tee observes that revenue has remained stable across cycles, reflecting production-linked demand rather than discretionary retail.

Tee describes the company’s balance sheet as “stable” with net cash of HK$288.5 million and cash accounting for around 35% of total assets, with only lease-related liabilities outstanding. In line with the higher earnings, the company paid total dividends of 20.5 HK cents for FY2025, up from 18 HK cents in the preceding year.

From Tee’s perspective, Infinity Development’s business is structurally defensive but may see some margin pressure in the current FY2026, no thanks to higher input costs of its own due to fighting in the Middle East. The company’s main market is Vietnam, but India has more growth potential. “While currently around 1 % of revenue and with no manufacturing investments announced, it represents a potential option for future footprint expansion as customer demand visibility scales,” says Tee.

See also: CGS International maintains 'add' call on Sembcorp with target price of $7.68

The ongoing war in the Middle East may have raised costs in the near term, but Infinity Development is seen as benefiting from structural tailwinds. Tee notes that the global footwear market is projected to grow from US$495 billion in 2025 to approximately US$790 billion by 2032, driven by emerging-market consumption, sportswear penetration and lifestyle shifts. “Rising labour costs, tariffs and supply-chain diversification continue to shift production from China into Vietnam and Indonesia, benefiting regionally embedded suppliers such as Infinity,” she says.

Tee’s 62 cents target price is just a forward multiple of 4.3 times, which is to reflect “a conservative risk assessment amid heightened macro uncertainty and near-term cost pressure across Asia”. — The Edge Singapore

Parkway Life REIT

Price target:

DBS Group Research ‘buy’ $4.75

Better entry point with pullback

Derek Tan of DBS Group Research has maintained his upbeat call on Parkway Life REIT (SGX:C2PU![]() ) , citing prospects for higher inflation, which will result in higher income given how the REIT’s income is structured.

) , citing prospects for higher inflation, which will result in higher income given how the REIT’s income is structured.

For more stories about where money flows, click here for Capital Section

On April 14, the Monetary Authority of Singapore raised its inflation forecast to 1.5%–2.5%, from 1%–2%, to reflect mounting price pressures driven in part by volatility in energy prices and supply disruptions linked to the Middle East conflict.

This marks the second upward revision this year, following an earlier increase in January, and a considerable shift from the 0.5%–1.5% outlook projected in October last year.

From Tan’s perspective, rising inflation is a clear tailwind for PREIT. Under its lease agreement, 65% of its revenue is derived from Singapore hospitals under an inflation-linked rental structure based on the Consumer Price Index + 1% formula, which embeds structural upside in a higher-inflation environment.

“While a shift to base-plus-variable rent, which is contingent on stronger post-AEI performance at Mount Elizabeth Orchard, remains a potential kicker, we await clearer data points before revising assumptions sometime in the middle of 2026,” says Tan.

This hospital, the REIT’s flagship property, recently completed an extensive multi-year refurbishment which means it can now resume operating at full capacity.

Tan believes that the higher 2026 inflation outlook should feed directly into stronger FY2027 rent growth, implying potential upside to his estimates of around 0.4%–1.6%.

“Parkway Life REIT stands out as the only Singapore REIT with income visibility to 2042, offering a rare combination of certainty and inflation-plus growth. Recent share price weakness presents an attractive entry point,” says Tan, noting that this stock now trades at around 1.5 times forward P/B with a 4.5% forward yield. Tan’s call remains “buy” with a target price of $4.75. — The Edge Singapore

Sheng Siong Group

Price target:

CGS International ‘add’ $3.40

More cost-of-living support

Citing the expected boost from government measures to help citizens deal with the higher cost of living, CGS International (CGSI) has raised its target price for Sheng Siong Group (SGX:OV8![]() ) from $2.97 to $3.40.

) from $2.97 to $3.40.

On April 7, the government announced that $500 in CDC vouchers per household, originally planned for January 2027, will now be distributed in June, along with other support measures worth some $1 billion.

“With the government now expecting inflation in 2026 to exceed its earlier 1%–2% forecast, we believe consumers will increasingly gravitate to value-for-money options, benefitting Sheng Siong Group,” state analysts Meghana Kande and Lim Siew Khee in their April 7 note.

Sheng Siong, a leading supermarket chain in Singapore, is known for its value offerings.

In the first two months of the year, supermarket sales in Singapore were up 6% y-o-y, versus 4% y-o-y for the whole of 2025.

Sheng Siong outpaced overall industry growth by six percentage points in 2025. Kande and Lim expect this momentum to continue if the company expands its network rapidly, with 16 new stores open since the second half of 2024. “Coupled with sustained demand for value offerings, we see Sheng Siong’s strong revenue momentum extending into FY2026,” they reason.

In addition, they expect the company to benefit from improved operating leverage and economies of scale, which can help offset some cost pressures.

Kande and Lim are standing by their earlier forecast of a 50-basis-point expansion in gross profit margin from FY2026 to FY2027. “We reiterate ‘add’ on Sheng Siong for its resilient demand profile and continued market share gains,” state Kande and Lim, who have raised their FY2026 to FY2028 earnings estimates by 1% on the premise that per-store sales will increase.

Their new target price of $3.40 is based on a 28 times FY2027 earnings multiple, up from an earlier 25 times, which is three standard deviations above Sheng Siong’s 10-year average.

The analysts believe this higher multiple is justified, given that Sheng Siong is in a structurally stronger position, with a larger store network and rising market share compared to a decade ago.

“We think the market will continue to ascribe a premium to its defensive positioning amid expectations for prolonged macroeconomic weakness,” they reason.

Re-rating catalysts include faster store openings and stronger margins. On the other hand, downside risks: higher staff costs and stiffer price competition. — The Edge Singapore

Singapore Telecommunications

Price target:

Maybank Securities ‘buy’ $5.25

Investment thesis delayed, not derailed

Bharti Airtel’s share price, whose gains over the past two years have helped nudge along those of Singapore Telecommunications (SGX:Z74![]() ) (Singtel), has corrected by just over 10% year to date, as tariff hikes may be delayed by around six months due to woes in the Middle East.

) (Singtel), has corrected by just over 10% year to date, as tariff hikes may be delayed by around six months due to woes in the Middle East.

Yet, Hussaini Saifee of Maybank Securities has maintained his “buy” call and $5.25 target price on Singtel, whose own share price is slightly off its recent high, as an opportunity to “accumulate” as Singtel’s story looks “delayed, not derailed”.

In his April 13 note, Saifee says that the medium-term thesis for Bharti Airtel remains intact. In India, with essentially two strong players, rational competition remains the order of the day.

“Mobile spend as a percentage of GDP at 0.8% still among the lower end of Asian emerging market peers, and data consumption among the highest globally — all of which support further monetisation over time,” he says.

In addition, Jio, controlled by rival conglomerate Reliance, is targeting an IPO at a 13 times EV/Ebitda multiple, a 34% premium to what Bharti Airtel now fetches.

Outside India, Singtel’s other businesses are largely resilient. In Australia, the market is seeing its own round of mobile price hikes, with market leader Telstra up by 5% to 15%, while Singtel’s unit Optus managed 5% to 6%.

Such a trend, according to Saifee, reinforces a rational market backdrop and should support monetisation, even as Optus invests more heavily to get its house in order following the recent high-profile outages. Other Asean associates also remain broadly stable, with Thailand’s AIS growing its earnings at 9%.

Here in Singapore, industry consolidation appears to be delayed, with regulators yet to approve Tuas’s acquisition of M1 from Keppel. “We see it as postponed rather than derailed,” says Saifee.

Meanwhile, data centres for Singtel remain a smaller but fast-growing bright spot, with ebitda expected to grow at a CAGR of 29% over FY2025 to FY2028.

According to Saifee, with the recent correction in Bharti Airtel’s share price, concerns have emerged about whether Singtel will still partially divest its stake in Bharti to meet its capital management targets.

Singtel has in place an asset monetisation strategy whose most regular feature thus far has been the periodic trimming of its stake in Airtel, often at $1 billion a pop.

Saifee reasons that Singtel still has ample buffer from past capital recycling to support payouts. He notes that Singtel’s Net debt/Ebitda is just 1.0 times and would rise only to 1.3 times by FY2028, even after elevated dividends and ongoing buybacks under a $2 billion programme.

Even if Singtel pauses the sale of its stake in Bharti Airtel, Saifee believes that Singtel could then sell its 7.7% stake in Thailand’s Gulf Development valued at $2.8 billion, which “looks increasingly monetisable after the stock’s sharp 42% year to date re-rating.” — The Edge Singapore

Delfi

Price target:

UOB Kay Hian ‘buy’ $1.68

Better margins with lower cocoa prices

Heidi Mo and John Cheong of UOB Kay Hian have raised their target price for Delfi (SGX:P34![]() ) from $1.12 to $1.68, on the premise that cocoa prices, down by some 60% from the 2024 peak, will mean lower cost pressures on the chocolate maker.

) from $1.12 to $1.68, on the premise that cocoa prices, down by some 60% from the 2024 peak, will mean lower cost pressures on the chocolate maker.

In their April 14 note, Mo and Cheong point out that from up to US$12,900 ($16,425) per tonne, cocoa prices are now as low as US$3,200 per tonne, thereby marking a “clear turning point” where Delfi’s gross margin was compressed to 26.5% in 2025 from 27.4% in 2024. Back in 2018, the company was making gross margins of around 35%.

Last year, margins were further weighed down by a weaker rupiah against the reporting currency, the US dollar, and higher promotion spending.

“With costs now correcting sharply, we expect a lagged but meaningful recovery in gross margins in 2026–2027, supporting improved operating leverage and earnings recovery,” state Mo and Cheong. Although listed in Singapore, Delfi commands half of Indonesia’s chocolate market share.

However, the analysts point out that the benefits of lower cocoa prices will not be felt immediately, as the company buys up to 18 months in advance.

Also, the rupiah may remain weak, offsetting lower raw material costs, which are largely denominated in the greenback. As an indication, a 3.9% depreciation of the rupiah in 2024 contributed to a decline of 1.1 percentage points in gross margin. “Hence, while the direction of margins is improving, we expect the pace to be gradual rather than immediate,” say Mo and Cheong.

They believe that Delfi operates on a shorter product cycle, meaning it can pass through cost differences more quickly than larger multinationals in the same space. Delfi can manage too by making tweaks to pricing and product sizes, and by focusing more on its own premium brands, which fetch better margins.

Delfi’s own-brand products are seen to continue to generate the bulk of its earnings, posting 4.9% growth last year, helping offset declines in production for other brands.

“This reflects strong brand equity and pricing power, particularly in key products such as SilverQueen and Cha Cha. Given that Delfi’s own brands typically carry higher margins and allow for greater control over pricing and product mix, this stable revenue base positions Delfi well to capture upside as cocoa prices normalise,” reason Mo and Cheong.

Their higher target price of $1.68, up from $1.12, is based on raising their valuation multiple from the historical mean of 18 times to 25.5 times FY2027 earnings, which is 0.5 standard deviation above the historical mean.

“With 2025 marking a margin trough, we see Delfi entering an earnings recovery cycle supported by improving gross margins and operating leverage. Delfi currently trades at 18 times 2027 P/E, or a 25% discount to global peers,” the analysts say. — The Edge Singapore

Sembcorp Industries

Price target:

UOB Kay Hian ‘buy’ $8.06

Alinta’s coal: from liability to asset

With the Middle East conflict ongoing, countries have been scrambling to find alternative energy sources. One alternative fuel is coal. Despite being polluting, coal is relatively cheap and reliable, suitable for supporting nations as they seek to mitigate the energy crisis.

Against this backdrop, UOB Kay Hian (UOBKH) analyst Adrian Loh is reinforcing his confidence in Sembcorp Industries (SGX:U96![]() ) . In his report dated April 15, Loh maintains his “buy” call, raising the target price from $7.10 to $8.06.

) . In his report dated April 15, Loh maintains his “buy” call, raising the target price from $7.10 to $8.06.

The analyst’s optimism is fuelled by the imminent completion of Sembcorp’s acquisition of Alinta Energy, an Australian electricity generator and gas retailer. To recap, Sembcorp announced in December 2025 that it had agreed to acquire Alinta for an enterprise value of A$6.5 billion ($5.6 billion).

Loh expects the Alinta deal to be completed by the end of 1H2026. He points out that the acquisition is immediately earnings accretive, with pro forma earnings per share for 1HFY2025 ended June 30, 2025 rising by 14% to $0.65 and return on equity rising to 22.5% from 19.7%. Incorporating Alinta’s 3.4GW of installed and contracted generating assets into Sembcorp’s earnings, Loh estimates Sembcorp’s earnings to rise by 16%–25% for FY2026 to FY2028.

The way Loh sees it, the expansion into the Australian market rebalances Sembcorp’s geographic risk profile as Singapore and the UK combined represented just 28% of attributable capacity, with OECD markets increasing to 37% of capacity and 64% of underlying net profit post-acquisition. He believes Australia’s stable regulatory environment, strict rule of law, and transparent energy market structures enhance the resilience and sustainability of the company’s portfolio.

Loh is also upbeat about Alinta’s performance. He points out the company leads its peers with a 2024 ebitda margin at 19% while being structurally long in generation capacity with volumes sold exceeding generation output by 5.5 terawatt-hour in 2025. For him, Alinta is well-positioned for Australia’s energy transition, given its 10.4-gigawatt (GW) development pipeline, which is skewed towards battery energy storage solutions (BESS) and wind.

In the near term, this development pipeline will add 33% of capacity or 2.2GW of gas, wind and BESS to Sembcorp’s development pipeline of 6.6GW. In the longer term, Alinta will contribute 8GW to Sembcorp’s 69GW pipeline, bringing the total development options to 78GW globally. Given Australia’s energy transition and Alinta’s existing assets, which include transmission and grid proximity, Loh believes the renewable optionality is strategically significant, as it lowers execution risk.

From his perspective, Alinta’s coal-fired Loy Yang B powerplant has transformed from a liability into an asset in light of the energy crisis. With the Strait of Hormuz “blocked”, limiting exports of oil and gas, coal has become the primary bridge fuel, substituting for oil and LNG imports across Asia.

Thus, as one of the lowest-cost coal generators, with a short-run marginal cost of power generation of just A$22 per megawatt-hour, Loy Yang B offers reliable, price-competitive baseload generation and is now seen as a dispatchable baseload asset, presumably a critical component of Sembcorp’s portfolio.

Valuing Sembcorp at 11.8 times P/E or one standard deviation above the company’s three-year average of 8.9 times, UOBKH calculates the counter to be worth $8.06 based on forecasted FY2027 earnings per share. — Lin Daoyi