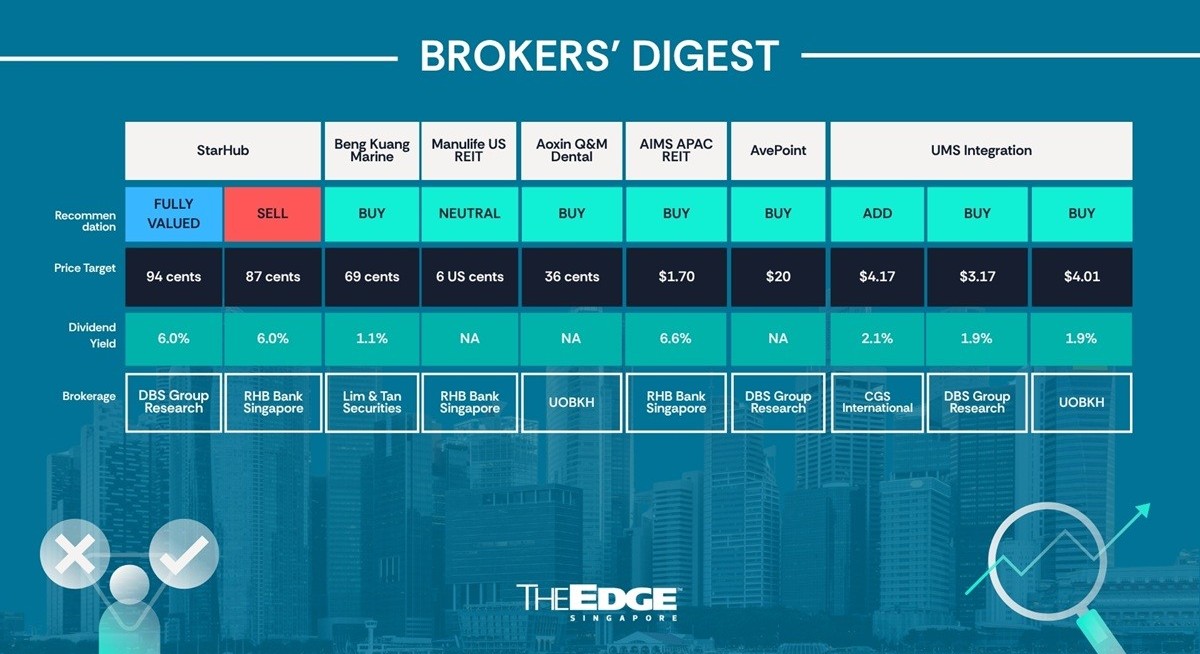

RHB Bank Singapore ‘buy’ $1.70

NAV boost ahead

Vijay Natarajan of RHB Bank Singapore has maintained his “buy” rating on AIMS APAC REIT (AA REIT) and raised his target price to $1.70 from $1.62. Natarajan has also increased his FY2028 distribution per unit (DPU) estimate by 3%, reflecting savings from the refinancing of perpetual securities.

Natarajan says AA REIT’s results for the FY2026 ended March 31 stood in line with expectations, with total distributable income rising to $81.6 million from $77.5 million in FY2025.

See also: RHB's Natarajan raises target price for CICT to $2.75

He expands that portfolio committed occupancy remains robust at 96.8%, and same-store portfolio valuation grew approximately 3% y-o-y, driven by higher valuations for its Singapore properties, with Australian dollar appreciation partly offsetting slightly higher capitalisation rates in Australia.

The more exciting medium-term catalyst, comments Natarajan, lies in AA REIT’s Australian assets. Its Macquarie Park and Bella Vista properties were recently endorsed by authorities as part of 15 data centre projects, and management is undertaking feasibility studies into the potential development of hyperscale data centres.

“The projects — if they materialise — could boost net asset value (NAV) by approximately 10%–20%,” says Natarajan, though he expects the process is likely to take two to three years. AA REIT is currently in preliminary talks with potential joint venture partners to explore these value-unlocking opportunities.

See also: OCBC's Lim downgrades Sats to 'hold' following recent gains

According to Natarajan, one key earnings driver over FY2027–FY2029 will be savings from refinancing perpetual securities, with the REIT issuing $250 million in new perpetual securities to redeem $250 million of higher-coupon perpetuals in September, generating approximately $3 million in annual savings.

Combined with positive rent reversions, which are expected to moderate to 3%–5% in FY2027 from 7.7% in FY2026, Natarajan forecasts a FY2027–FY2029 DPU compound annual growth rate of approximately 4%, with DPU rising from 10 cents in FY2026 to 11 cents in FY2028 and FY2029.

Natarajan also lifted AA REIT’s ESG premium to 6% from 4%, citing a 40% increase in solar power capacity to 15.5 MWp in FY2026 and over 60% of new and renewed leases being classified as green leases. — Belle Neo

Aoxin Q&M Dental Group

Price target:

UOB Kay Hian ’buy’ 36 cents

Sustained earnings momentum

For more stories about where money flows, click here for Capital Section

Tang Kai Jie of UOB Kay Hian has initiated coverage on Aoxin Q&M Dental with a “buy” call and a target price of 36 cents. Tang’s target price is pegged to an FY2027 P/E of 52.5 times and 2.5 standard deviations (s.d.) above historical averages, based on parent company Q&M Dental Group’s P/E band.

In its FY2025 ended Dec 31, 2025, Aoxin delivered a significant earnings turnaround, swinging from a net loss of RMB8 million ($1.5 million) in FY2024 to a net profit of RMB7 million, driven primarily by a sharp narrowing of losses from its associate Acumen Diagnostics. Core net profit also grew 11.6% y-o-y to RMB7 million despite a 3.6% decline in revenue to RMB171 million, supported by improved cost discipline.

On the revenue front, weakness in the primary healthcare segment was partially offset by stronger dental equipment distribution sales to government hospitals and higher laboratory services revenue from Singapore.

“Primary healthcare remains the core earnings driver, and recurring demand from preventive and restorative treatments underpins strong revenue visibility over time,” says Tang.

Aoxin’s management is pursuing an aggressive acquisition-led expansion strategy into Central and Southern China, with two non-binding MOUs announced in 2026. The Central China target operates 30 clinics with around 80 dentists and is valued at RMB150 million. In contrast, the Southern China target operates 15 clinics with around 60 dentists and is valued at RMB376 million, with consideration split evenly between cash and shares.

If completed, the deals would nearly triple Aoxin’s current network to 59 clinics and add around 140 dentists, with Tang forecasting the acquisitions could contribute RMB32 million in profit in FY2027, lifting net profit nearly six-fold from RMB7 million to RMB40 million.

According to Tang, Aoxin’s balance sheet is well-positioned to fund this growth, with net cash doubling to RMB255 million following a proposed $20 million placement of 134 million shares, of which the parent company, Q&M Dental, subscribed for 50 million shares.

Tang notes that China’s dental market remains highly fragmented and is estimated at RMB160 billion to RMB200 billion, growing at 15%–20% annually, with organised dental chains expanding even faster at a CAGR of around 18%.

This fragmentation creates a compelling runway for Aoxin’s consolidation, a well-capitalised, institutionally-backed operator, says Tang.

Tang flags that despite the strong share price performance (up over 660% in the past three months), the near-term earnings contribution from acquisitions will take time to flow through, limiting upside in FY2026, where net profit is forecast at only RMB7.6 million on a 214 times FY2026 P/E before the step-change in 2027.

Despite the remaining completion risk, Tang still views the company’s risk-reward profile as “favourable, with sustained earnings momentum likely to catalyse a valuation re-rating over the next 12 months.” — Belle Neo

AvePoint

Price target:

DBS Group Research ‘buy’ $20

Steady quarter

DBS Group Research analyst Sachin Mittal has kept his “buy” call and $20 target price on AvePoint, after what he calls “a steady quarter” for the data management and governance software provider.

AvePoint’s 1QFY2026 results were broadly in line, supported by demand for AI governance and resiliency solutions. Total revenue rose 26% y-o-y and 2% q-o-q to US$117.2 million ($148.7 million), about 1% above consensus estimates and at the higher end of management’s guidance.

Software-as-a-Service (SaaS) remained AvePoint’s largest revenue driver, growing 35% y-o-y and 5% q-o-q to US$93.4 million. This lifted its share of total revenue to a record 80%.

Annual recurring revenue (ARR) rose 26% y-o-y and 4% q-o-q to US$435.2 million, in line with consensus. Net new ARR recorded its 12th consecutive quarter of double-digit organic growth.

One reason for Mittal’s positive view is AvePoint’s growing exposure to AI governance. Governance now accounts for about 40% of the company’s pipeline, up from less than a third last year, helped by the bundling of AI governance tools.

During the quarter, AvePoint launched AgentPulse Command Center, which enables unified monitoring and control of AI agents across Microsoft 365 and Google Cloud environments.

Non-GAAP operating income rose 53% y-o-y but declined 10% q-o-q to US$20.5 million, about 2% above consensus and at the higher end of management’s guidance. Non-GAAP operating margin came in at 17.5%, up 310 basis points y-o-y, helped by improved sales productivity, growing channel contribution and operating leverage.

AvePoint has trimmed its FY2026 ARR and non-GAAP operating income guidance slightly due to the stronger US dollar. Management now expects FY2026 ARR of US$523.4 million to US$529.4 million, from US$525.1 million to US$531.1 million previously. The midpoint remains in line with consensus.

FY2026 non-GAAP operating income guidance was also lowered to US$91.5 million to US$94.5 million, from US$92.6 million to US$96.6 million previously.

Still, Mittal does not see the softer guidance as a major concern. “AvePoint has a track record of delivering above its quarterly guidance for revenue and non-GAAP operating income, as we have seen in the past four quarters,” he writes in his May 8 note.

The company is continuing to invest in sales, marketing, AI governance capabilities and go-to-market expansion as it works towards its US$1 billion ARR target by 2029.

Mittal expects AvePoint’s FY2026 performance to benefit from a recovery in US public-sector spending, rising demand for resiliency solutions in the Middle East and AI governance-driven ARR growth.

AvePoint’s longer-term ARR target is expected to be driven by multi-cloud growth, led by a sharper rise in Google-related demand, and by AI governance.

Management also reiterated expectations for FY2026 free cash flow exceeding US$100 million, while continuing share repurchases and retaining flexibility for strategic acquisitions. — Nurdianah Md Nur

Beng Kuang Marine

Price target:

Lim & Tan Securities ‘buy’ 69 cents

Greater interest, management raises stake

Nicholas Yon of Lim and Tan Securities has reinforced his “buy” call on Beng Kuang Marine by raising his valuation to 69 cents per share in his May 8 report. In his previous initiation report on March 31, Yon valued Beng Kuang at 53.5 cents per share.

His confidence comes on the back of Beng Kuang’s results for 1QFY2026 ended March 31, being “in line” with expectations. For the period, Beng Kuang reported $2.8 million in net profit, representing a 12.7% y-o-y decrease but 9% q-o-q increase. Meanwhile, revenue rose y-o-y by 20.3% to $25.7 million.

Yon believes Beng Kuang’s first-quarter performance reflects healthy operational activity, suggesting the y-o-y profit decline is likely due to spillover delays from 4QFY2026. He does not expect further delays moving forward.

Noting that gross profit margin dropped by 9.9 percentage points y-o-y to 26.5%, he suggests that this is not due to a weakening of fundamentals, but more of a feature of the offshore and marine (O&M) sector where O&M engineering businesses often experience quarterly earnings volatility depending on project stages, customer delivery schedules and work composition.

Yon, presumably heartened by Beng Kuang’s orderbook and its soon-to-be wholly-owned subsidiary Asian Sealand Offshore and Marine (ASOM), states that revenue visibility is “healthy” and he expects earnings momentum to strengthen in the second half of the year.

He points to three sources for his optimism about his order book. Firstly, Beng Kuang has secured around $56 million in contracts as at 1QFY2026, of which around $51 million is to be recognised in 2026. This is augmented by ASOM’s $27.6 million in floating production, storage, and offloading (FPSO) and floating storage and offloading (FSO) contracts, of which around 80% were FPSO-related and recurring.

In addition, subsidiaries PT Nexus Engineering Indonesia and International Offshore Equipment are providing long-term earnings visibility through fabrication, shipbuilding and offshore projects extending into FY2027 and FY2028.

Another point reinforcing Yon’s confidence is the institutional interest and insider accumulation of shares in the company. Institutional investors Amova Asset Management and Tokio Marine Life Insurance Singapore have acquired shares from executive director Chua Meng Hua, while executive chairman Chua Beng Yong and CEO Yong Jiunn Run have increased their stakes in the company to 4.92% and 5.30%, respectively.

To Yon, this signals management’s confidence in the company. “More importantly, the transaction strengthens Beng Kuang Marine’s institutional shareholder base at a time when offshore and FPSO-related activity continues to improve globally,” he adds.

On the backdrop of increased institutional participation, Yon values the counter at 13 times the forward FY2027 P/E or 69 cents. — Lin Daoyi

Manulife US REIT

Price target:

RHB Bank Singapore ‘neutral’ 6 US cents

Outlook remains cloudy

RHB Bank Singapore analyst Vijay Natarajan maintains his “neutral” call with an unchanged target price of 6 US cents (7.6 cents) on Manulife US REIT (MUST) following the REIT’s 1QFY2026 operating update.

The May 6 report by RHB follows MUST’s report of stable portfolio occupancy q-o-q at 67.6% and continued progress on its proposed divestment of the Figueroa office tower in Los Angeles.

The property is set to be sold to a municipal entity for a gross consideration of US$92.5 million, around 6% below its end-2025 valuation.

Natarajan says the proposed sale of the Figueroa will mark a “major milestone” in the REIT’s efforts to exit its lenders’ master restructuring agreement (MRA). Net proceeds from the transaction are expected to be used to fully repay debt due in July 2026 and partially reduce debt maturing in 2027, thereby lowering gearing to 55.4% from the current 58%.

However, Natarajan says the REIT’s growth outlook has turned “cloudy”, with volatile interest rates likely to dampen transaction activity even as plans are in motion to divest two more office assets. This move is to reduce leverage before gradually resuming distributions, while exploring acquisitions of up to US$600 million ($760.4 million) across the industrial, living and retail sectors.

While the REIT intends to eventually resume distributions after stabilising its balance sheet, RHB does not expect dividends to return in the near term.

Still, Natarajan notes that leasing demand remained resilient, supported by a “flight to quality” trend and limited office supply in the US market. Assuming the Figueroa sale is completed, portfolio occupancy would improve to 73.2%, while only 4% of leases are due for expiry in FY2026.

RHB has lowered its FY2026 and FY2027 distributable income forecasts by 10% and 11%, respectively, to account for completed divestments, saying that they “do not expect a dividend resumption for now, as MUST’s focus remains on reducing leverage.” Its target price remains pegged at 0.3 times the FY2026 forecast book value. — Belle Neo

StarHub

Price targets:

DBS Group Research ‘fully valued’ 94 cents

RHB Bank Singapore ‘sell’ 87 cents

Weak 1Q as price competition bites

DBS Group Research and RHB Bank are staying cautious on StarHub after the telco’s 1QFY2026 earnings missed expectations, with both research houses warning that price competition in mobile and broadband will continue to weigh on margins.

For the three months ended March, StarHub’s net profit after tax (NPAT) attributable to shareholders fell 81.3% y-o-y to $5.9 million, while ebitda declined 22.5% y-o-y to $77.7 million. Service revenue fell 3.9% y-o-y to $445.7 million, due mainly to lower revenue from its consumer segments.

DBS analyst Sachin Mittal says StarHub’s 1QFY2026 normalised earnings of $5.9 million came in below consensus expectations of $10.6 million, while service revenue was 4% below consensus expectations of $466.1 million. The miss was “mainly due to ebitda decline alongside higher depreciation and amortisation and higher net finance costs”, he writes in his May 7 note.

Mittal maintains his “fully valued” call on StarHub with an unchanged target of 94 cents.

Meanwhile, RHB has kept its “sell” call, lowering its target price to 87 cents from $1 previously, implying a downside of 13.9%. “We expect the earnings malaise to continue with price competition having intensified in recent weeks, while strategic cost management initiatives will take time to yield results,” says the research house.

The pressure was most visible in StarHub’s consumer business. Mobile service revenue fell 10.9% y-o-y to $124 million, while broadband revenue dropped 8.7% y-o-y to $58.8 million. Entertainment revenue declined 9.1% y-o-y to $45.8 million. StarHub says mobile revenue was lower mainly due to softer roaming, value-added services, and SMS usage, while broadband revenue fell mainly due to lower subscription revenue.

Both research houses flag competition as the main concern. DBS says StarHub highlighted that Singtel has been “overly aggressive” in both mobile and broadband. Similarly, RHB says management pointed to the incumbent undercutting prices across the board, with some price points falling below mobile virtual network operators and value brands. That pressure is showing up in StarHub’s margins. Its service ebitda margin narrowed to 16.5% from 20.6% a year ago, while RHB says higher staff and marketing costs added to the ebitda drag.

StarHub has maintained its FY2026 ebitda guidance at 75% to 80% of FY2025 levels, which Mittal notes is below consensus expectations of about 83%. The company is also targeting $70 million in savings through FY2028 under its Strategic Cost Pillars programme, which includes legacy decommissioning, network optimisation, systems re-architecture, and business simplification.

However, Mittal expects the bulk of the savings to kick in only from FY2027 onwards, while RHB says the benefits are likely to be back-loaded to FY2028. RHB has cut its FY2026 and FY2027 core net profit forecasts by 10.7% and 8%, respectively, while raising its FY2028 forecast by 13%.

StarHub and Temasek agreed after the quarter ended to terminate an assigned rights arrangement relating to part of StarHub’s economic and equity interest in Ensign InfoSecurity for total cash proceeds of $121 million. StarHub expects to recognise a fair value gain of about $244 million, strengthening FY2026 NPAT, while its remaining 38.92% stake in Ensign will be accounted for as an associate.

The dividend remains one source of support. DBS says StarHub’s management remains committed to paying at least 6 cents per share for FY2026, while RHB forecasts a dividend yield of 6% from FY2026 to FY2028.

RHB says downside risks include weaker-than-expected earnings and margins, competition and regulatory setbacks. Upside risks include easing competition from industry consolidation and stronger-than-expected earnings, though the research house says such upside risks are receding as price competition intensifies. — Nurdianah Md Nur

UMS Integration

Price targets:

DBS Group Research ‘buy’ $3.17

CGS International ‘add’ $4.17

UOB Kay Hian ‘buy’ $4.01

Higher target prices on AI-led growth

UMS Integration has seen strong upgrades from various analysts following better 1QFY2026 ended March results, with expectations that AI-led growth will continue to drive further improvements.

In 1QFY2026, the company generated earnings of $14 million, an increase of 42.5% y-o-y. Revenue was up 20.4% y-o-y to $69.4 million in the same period, with growth from AI-led semiconductor demand, including that from new customers. Gross margin remained healthy at 52.6%, while net margin improved to 20.2%, helped by operating leverage and favourable currency movements.

In her May 13 note, Ling Lee Keng of DBS Group Research points out that UMS’s new key customer, already actively placing production orders for new products, has “many” more that are undergoing qualification. “This suggests a healthy pipeline of future production opportunities as these parts are progressively qualified and ramped up,” she reasons. She expects UMS to record double-digit sequential growth in FY2026 and that FY2027 will be better than FY2026.

To capture stronger demand, UMS is speeding up its capacity expansion plans. For now, Ling is keeping her forecasts with expectations of 42% earnings growth this FY2026 and another 25% in FY2027.

She is keeping her “buy” call but has raised her target price from $2.92 to $3.17 after applying a higher valuation multiple of 38 times FY2027 from 35 times previously, to reflect improved earnings visibility and structurally higher AI‑led growth, bringing the stock closer to global peers.

“UMS remains our top pick in the semiconductor space, supported by strong customer‑driven momentum and leveraged exposure to advanced packaging,” says Ling.

Similarly, William Tng of CGS International, citing positive signs from two key customers, has also turned more bullish on this stock. Tng has raised his FY2027 earnings estimates by 6.5% and F2028’s by 13.9%.

In addition, Tng has applied a higher multiple of 37 times P/E, from 26 times FY2027, which is four standard deviations above its five-year FY2022 to FY2026 average, to reflect the stronger profit potential from these two customers building up to FY2028. As such, Tng’s new target price is $4.17, up from $2.23.

For Tng, potential re-rating catalysts include further acceleration in orders for its new Penang plant from its new customer and the return of orders for aircraft components. On the other hand, downside risks include the negative impact of its key customers’ loss of sales in China and slower-than-expected progress in its business with new customers.

John Cheong of UOB Kay Hian has also turned more bullish on UMS. From a previous target price of just $1.80, Cheong now figures this counter is worth $4.01, reflecting the strong semiconductor industry outlook, better earnings quality from new contributions from its new customer, and more projects from its existing key customer.— The Edge Singapore