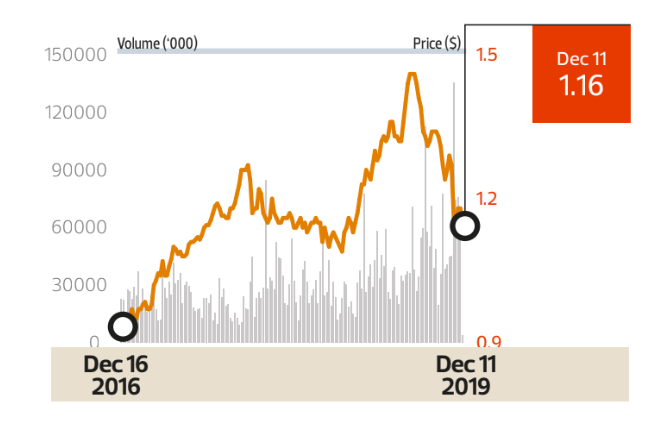

With only two assets under its belt, LendLease Global Commercial REIT (LLGCR) might not appear to be an attractive prospect for investors. But some analysts are keeping a close eye on the recently listed retail REIT.

Describing LLGCR as a “gem in the making”, DBS Group Research is initiating coverage on the REIT with a “buy” recommendation and a price target of $1.05.

Launched by Australia-listed developer Lendlease Group, the REIT’s portfolio currently comprises 313 @ Somerset mall in Singapore and Sky Complex, a Grade-A office development in Milan, Italy. But the way lead analyst Derek Tan sees it, Lendlease Global REIT’s portfolio, while only comprising two properties for now, offers “a good mix of resilience, growth and visibility”.

“LLGCR offers an opportunity to invest in a diversified portfolio of stabilised income-producing real estate assets that cater primarily to retail and/or office purposes,” Tan says in a Dec 5 report.

“Since 2016, the portfolio has enjoyed high occupancy rates of more than 99%, [which rose] to 99.9% as at June,” he notes. “While Sky Complex has enjoyed 100% occupancy over the past few years by virtue of it being a single-tenant lease, we are encouraged by the improvement shown by 313 @ Somerset in the past few years.”

According to Tan, about 92.8% of LLGCR’s leases by gross rental income have in-built rental escalations. He believes there are more good things to come for the two properties.

“313 @ Somerset is located on Orchard Road, which is poised to benefit from its repositioning as a vibrant lifestyle destination, while Sky Complex is located on Santa Giulia, which is being transformed into an innovative business and residential district,” Tan says.

Backed by its strong sponsor Lendlease Group, LLGCR also has a pipeline of accretive acquisition opportunities available to it in the future.

“The Lendlease Group has A$32.5 billion ($30.2 billion) worth of assets under management globally,” Tan says. “While the manager has identified Paya Lebar Quarter as a target, we see Jem or Parkway Parade as potential targets as well.”

With gearing currently standing at close to 35%, the analyst says LLGCR has enough debt headroom to take on opportunistic acquisitions. To be sure, DBS is not the only brokerage that is bullish on LLGCR’s prospects. Daiwa Securities Research in October initiated coverage on LLGCR with an “outperform” rating and a price target of $1.01.

Singapore Telecommunications

Price targets:

$3.32 HOLD (UOB Kay Hian Research)

$3.70 ADD (CGS-CIMB Research)

$3.72 HOLD (Maybank Kim Eng Research)

$4.05 BUY (HSBC Global Research)

$3.60 UPGRADE BUY (DBS Group Research)

UOB Kay Hian appears to have a “cautiously optimistic” stance on Singapore Telecommunications (Singtel), even as the group fights to defend its consumer and enterprise markets.

In a Dec 9 report, lead analyst Chong Lee Len notes that the telco is guiding for stable top-line Ebitda for the upcoming year amid competition in the consumer segment and a weak enterprise business outlook.

“Singtel will focus on defending its market share in both Singapore and Australia, drive digital businesses and keep a tight lid on costs via digitisation of its traditional operating model,” observes Chong.

In particular, Chong hones in on the group’s Indian associate, Bharti Airtel, which now has new prepaid mobile plans with price hikes ranging from 15% to 52%. “This comes on the back of mounting losses by Airtel and [Vodafone] Idea in the recent quarters,” says Chong. She notes that Airtel alone had reported core net loss of INR4.4 billion ($84 million) in 2QFY2020, on the back of provisions for an unfavourable court verdict on adjusted gross revenue, as well as a competitive operating landscape.

But a respite could be on the horizon for Bharti, in the form of the recent tariff hike, which Chong says could potentially lift the group’s FY2020-FY2021 net profits by 2% and 4% respectively. Yet, the near-term outlook remains fairly bleak.

“Near-term sentiment may be dampened by a recent capital-raising exercise of US$3 billion ($4.1 billion) by Bharti,” says Chong, adding that a US$2 billion equity-raising exercise will be carried out to approved shareholders, which could only tentatively include Singtel. The balance US$1 billion will be debt-funded.

On a local front, Singtel is poised to thrive on the upcoming 5G spectrum allocation by the Infocomm Media Development Authority (IMDA). The authority has decided on a two-player nationwide network and an additional two-player localised network framework.

“We expect IMDA to allocate 5G spectrum by June 30, 2020,” says Chong, who attests that Singtel could emerge as a potential beneficiary.

“We believe the two-player nationwide network will include Singtel and a consortium of multiple mobile network operators such as Starhub, M1, TPG Telecom and fibre network provider Netlink Trust,” says Chong.

However, Chong is quick to caution that Singtel’s potential capital expenditure (capex) might amount to the region of $1 billion to $2 billion, which translates into a potential need to raise capital.

In addition, although the brokerage attests that Singtel could benefit from the rising global 5G trend, it stresses that the initial use case will have a reach limited to only smart cities, as well as smart yard-confined and autonomous vehicle applications.

“This implies that meaningful earnings growth from 5G application and ecosystem will only materialise from 2022,” says Chong. “As such, in the near term, share price performance will be capped by higher capex intensity as telcos shift into the next 5G investment cycle.”

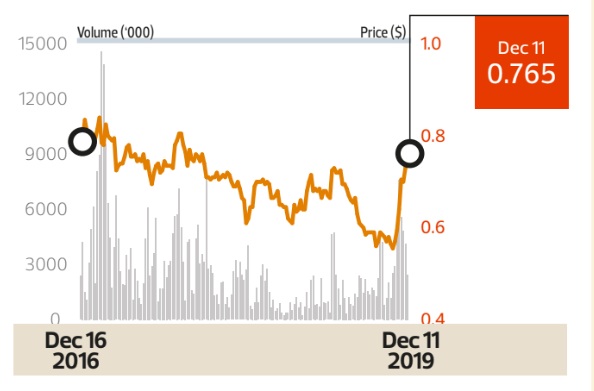

Mapletree North Asia Commercial Trust

Price targets:

$1.30 BUY (DBS Group Research)

$1.45 BUY (HSBC Global Research)

$1.29 ADD (CGS-CIMB Research)

It looks like there will be no magical Christmas for Mapletree North Asia Commercial Trust (MNACT) this year. DBS Group Research is cutting its price target for the REIT by 18.8% to $1.30 on the back of lower rental reversion assumptions for its key asset, Festival Walk.

This comes after the REIT manager on Dec 4 announced that the mall, which accounted for 61.7% of MNACT’s net property income (NPI) in the latest 1HFY2020 ended September, is expected to remain shuttered until 1QCY2020.

The Kowloon Tong property, Hong Kong’s then-largest shopping mall when it first opened in 1998, has been closed since Nov 13, following the spilling over of clashes between Hong Kong protestors and police.

“With its fortunes tied closely to the outlook for its key asset Festival Walk, the closure of the mall for extensive repairs and loss of income during the period will have an impact on its distributions,” says lead analyst Derek Tan in a Dec 6 report.

Meanwhile, to help mitigate the impact of a DPU that is expected to be “significantly lower” as a result of the loss in revenue at Festival Walk, the manager has announced a plan to implement a top-up to the distributable income for the next three quarters up to 1QFY2020/21 ending June 2020.

Tan opines that this distribution top-up, which will be funded by external borrowings that will be repaid once the insurance claims proceeds are received, should be read positively.

“The timely support from a distribution top-up adds clarity to the stock, in our view, stemming further downside risk,” he explains. “Gearing is not expected to rise significantly in the interim period of such distribution payout.”

At the same time, MNACT’s manager has also announced the proposed acquisition of an effective interest of 98.47% in two office properties in Japan from sponsor Mapletree Investments for a total cost of $482.5 million.

Notably, the proposed acquisition, which has an expected NPI yield of 4.5%, will also reduce the income and asset concentration of Festival Walk and accelerate the income diversification of MNACT.

Plantation Recovery

Bumitama Agri

Price targets:

81 cents BUY (DBS Group Research)

80 cents BUY (RHB Group Research)

75 cents BUY (UOB Kay Hian Research)

80 cents BUY (Maybank Kim Eng Research)

First Resources

Price targets:

$2.10 BUY (DBS Group Research)

$1.94 ADD (CGS-CIMB Research)

$2.30 OVERWEIGHT (JP Morgan Research)

$1.85 BUY (UOB Kay Hian Research)

$1.86 DOWNGRADE HOLD (Maybank Kim Eng Research)

$1.95 BUY (RHB Group Research)

Wilmar International

Price targets:

$4.75 BUY (RHB Group Research)

$4.75 BUY (UOB Kay Hian Research)

$4.60 BUY (DBS Group Research)

$4.58 ADD (CGS-CIMB Research)

$5.00 OVERWEIGHT (JP Morgan Research)

$4.21 HOLD (Maybank Kim Eng Research)

$4.09 HOLD (Daiwa Securities Research)

The storm looks to have blown over for palm oil players.

According to DBS Group Research, average crude palm oil (CPO) prices are expected to rebound 19% to US$596 per metric tonne in 2020.

The recovery will be driven by plateauing global palm oil supply, DBS says, alongside reasonable headroom for soybean price, owing to positive developments in the US-China trade war and African swine fever.

In addition, the brokerage also expects demand to remain steady in 2020.

“After weak share prices in 9M2019, CPO stocks rebounded in 4QFY2019 due to the recovery of the CPO price, and this led to stronger y-o-y earnings on higher average selling price,” says lead analyst William Simadiputra in a Dec 9 report.

But even as the plantation counters look poised to leave the dry spell behind them, DBS believes it is important to stay selective on stock picks.

“The plantation universe is currently a mixed bag,” Simadiputra says. “Some companies are better than others in capitalising on the CPO price recovery.”

Despite the hype over the CPO price rally, Simadiputra stresses that it is good to be selective. “Some companies have rallied ahead of their fundamentals,” he says. “We prefer Singapore-listed Bumitama Agri (BAL), First Resources (FR) and Wilmar International (WIL) over Indonesia-listed stocks.”

For one, Simadiputra favours BAL and FR for their undemanding valuations as well as strong yield performance to capitalise on the recovery of CPO prices.

Simadiputra is raising his earnings forecasts for BAL in FY2020F and FY2021F by 12% and 13% respectively to account for better profitability from higher palm oil prices in the year and more conservative fertiliser application next year.

At the same time, he expects FR’s earnings to rebound 72% y-o-y to US$148 million in 2020, driven by higher CPO prices.

“FR remains our [top] pick in the plantation sector, given its strong asset base to capitalise on the edible oil market recovery in 2020,” Simadiputra says.

Meanwhile, the analyst also likes WIL for its integrated upstream-downstream business model, which provides a cushion on profitability when commodity prices are volatile. “We assume that WIL can maintain good profitability amid low edible oil prices, despite the prolonged trade war,” Simadiputra says.

“As we gather more information on Wilmar’s China operations, we are increasingly convinced that [the company’s] potential is far greater than market expectations,” he adds. “A special dividend and 1Q2020 listing of its China business Yihai Kerry Arawana Holdings are further positive catalysts for share price.”

Koufu Group

Price targets:

87 cents BUY (SAC Capital)

95 cents BUY (UOB Kay Hian Research)

88 cents BUY (DBS Group Research)

SAC Capital is initiating a “buy” recommendation on food court and coffee shop manager Koufu, with a price target of 87 cents.

In a Dec 11 report, lead analyst Chow Zheng Jie says, “We like the strong ROE, cash generative and defensive business model. And we expect more new outlets, a new facility and overseas expansion [to] be the impetus for earnings growth.”

Koufu has guided that its new integrated facility at Woodlands will be operational in 1HFY2020. This facility will consolidate and expand its central kitchen capacity, enabling central procurement, food preparation, processing and distribution to the eateries.

The construction of the facility is worth about $40 million and largely funded by IPO proceeds.

Meanwhile, Chow reckons that about 30% of the facility’s space could be leased out to third-party food processors. With the new facility, Koufu also has the potential to extend its business into food catering to institutions and corporate customers.

On the other hand, the group boasts strong net margins of 12% and an ROE of 29%, even with net cash of $93.5 million accounting for 97% of net assets.

In its latest 9MFY2019 results, earnings increased 24.6% y-o-y to $21.2 million, mainly owing to the reopening of the group’s Rasapura food court at Marina Bay Sands and high operating leverage. Revenue for the period was 6.2% higher y-o-y at $177.2 million. “Network expansion will translate into greater growth at the bottom line,” says Chow